Infosys' target has been cut by 27 per cent to Rs 950 from Rs 1,300 earlier. Wipro's target is down to Rs 156 from Rs 200 earlier, down 22 per cent.

Infosys' target has been cut by 27 per cent to Rs 950 from Rs 1,300 earlier. Wipro's target is down to Rs 156 from Rs 200 earlier, down 22 per cent. Infosys' target has been cut by 27 per cent to Rs 950 from Rs 1,300 earlier. Wipro's target is down to Rs 156 from Rs 200 earlier, down 22 per cent.

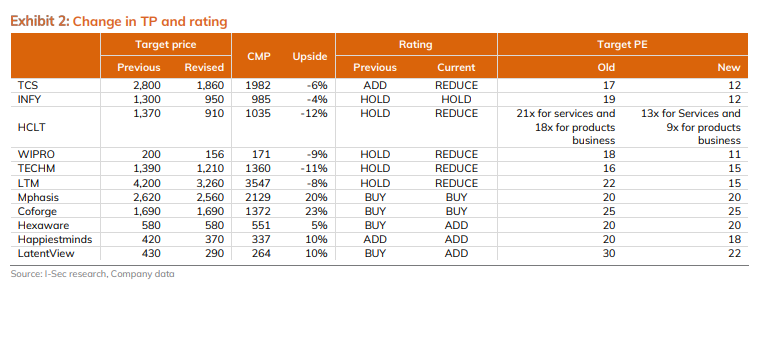

Infosys' target has been cut by 27 per cent to Rs 950 from Rs 1,300 earlier. Wipro's target is down to Rs 156 from Rs 200 earlier, down 22 per cent.ICICI Securities on Thursday said it has turned 'negative' on the IT sector from 'Neutral', particularly on large-cap IT stocks such as Tata Consultancy Services Ltd (TCS), Infosys Ltd, Wipro Ltd and HCL Technologies Ltd, given the protracted low-to-mid single-digit revenue growth expectation for the pack over FY24–28. The domestic brokerage suggested revised targets for stocks, which were up to 34 per cent lower than its previous targets.

Among the biggest target cuts, TCS' target has been slashed 33.57 per cent to Rs 1,860 from Rs 2,800. HCL Tech's target now stands at Rs 910, down 34 per cent from Rs 1,370 earlier. Infosys' target has been cut by 27 per cent to Rs 950 from Rs 1,300 earlier. Wipro's target is down to Rs 156 from Rs 200 earlier, down 22 per cent.

ICICI Securities said downside risks are now more pronounced as it leaned towards select mid-sized companies, namely Mphasis Ltd and Coforge Ltd, given their strong deal total contract value (TCV) growth, which provides near-term visibility of healthy organic revenue growth.

The domestic brokerage expects Q1FY27 revenue growth for the top-6 IT Services firms to be at minus 0.9 per cent to 1.1 per cent QoQ in constant currency (CC) terms, lower than what it was building in at the quarter’s start.

"Our view is premised on the delays in conversion of TCV to revenue, stemming from incremental macro weakness and potentially higher AI deflation. Margins pressure could mount too amid higher AI capability, S&M investments, and front-loading of AI-productivity benefits," it said.

The brokerage said there is a disconnect between growth in TCV and revenue for IT Services, implying higher AI-led deflation in existing book of business.

It said there is a weakening correlation between technology spend growth of US banks and IT Services’ BFSI revenue growth; and S&P 500 revenue growth and top-5 IT US revenue growth. This implied a shift of spends to in-house GCCs and AI infrastructure and frontier AI players, ICICI Securities said.

It gave an example of Indian IT Services exports, which grew 12 per cent YoY in FY26 against 3.6 per cent growth of top5 IT services companies in dollar terms – implying shift of spends to GCCs and other technology players in the AI value chain.

"We have re-aligned target multiples of large-cap IT to sector’s long-term average-2SD P/E to capture aforementioned downside risks to revenue. However, we note that there could be further downside risk to valuation multiples in scenarios if net new enterprise AI adoption use cases are slow to pick-up or do not meaningfully pick-up due to cost, security, accuracy and governance constraints while AI led cannibalization in IT Services delivery and competitive intensity continues to increase," ICICI Securities said.

This is what it said on the first quarter (June quarter) earnings preview of top IT majors.

TCS Q1 results preview

ICICI Securities expects 0.3 per cent QoQ CC (flat QoQ in dollar terms) revenue growth for TCS in Q1FY27, led by delays or deferrals in ramp-up of TCV to revenue due to weak macro from ongoing Middle East war. Slowdown in ramp-up of TCV to revenue is broad-based across verticals, it said.

"We expect the BFSI vertical to lead revenue growth led by ramp-up of two mega deal wins in FY27. We expect healthy deal bookings between USD 9-11bn for the quarter. We expect EBIT margin to contract by 150bps QoQ, led by a three-month impact from the annual wage hike, investments in AI and sales & marketing, which are likely to be offset by currency tailwinds," it said.

ICICI Securities said TCS has not yet announced finalisation of land purchase for the AI datacentre buildout in its hyper-vault business. Post land finalisation, the AI datacentre build-out would take 18 months.

Infosys Q1 results preview

ICICI Securities sees Infosys reporting organic revenue growth of 0.9 per cent QoQ CC in Q1FY27. This may include 0.9 per cent contribution for two months from Optimum Healthcare acquisition consolidation, taking overall growth to 1.8 per cent QoQ CC.

"We envisage softer organic growth (vs. 0.7–1.4 per cent CQGR required to achieve guidance of 1.5–3.5 per cent for FY27) due to delays in decision making, impacting volumes in April 2026 (also seen in March 2026). BFSI

and energy utility and resources will likely lead revenue growth. Hi-tech and retail are expected to be soft due to higher exposure to discretionary spends," ICICI Securities said.

The brokerage said the underlying demand in auto and communication remains soft for Infosys.

"We expect deal TCV to be in-line with its past four-quarter average, with quite a few deals announced during the quarter. EBIT margin may shrink by 20 bps QoQ led by headwinds from D&A charge from closure of Optimum Heathcare

acquisition; absence of 20bps benefit from reversals of provisions seen in Q4FY26; and AI investments – these would be partially offset by currency tailwinds," ICICI Securities said.

HCL Tech Q1 results preview

ICICI Securities said HCL Tech’s revenue to decline minus 0.9 per cent QoQ CC in Q1FY27 led by discretionary spending cuts by two US-based telecom clients, discontinuation of SAP programs by two other clients and seasonal weakness in Q1.

"We expect EBIT margin to contract by 25bps QoQ due to the absence of operating leverage on revenue growth, employee restructuring costs, and AI investments – partly offset by tailwinds from currency," it said.

Wipro Q1 results preview

ICICI Securities anticipated Wipro to report minus 0.4 per cent QoQ CC revenue growth in IT Services. It sees a healthy ramp-up of the Olam deal aiding growth in the retail vertical. The Q1 results would include 1.5-month contribution of 0.8 per cent from the consolidation of Mindsprint and Alpha Net Consulting; and healthy revenue growth in the Harman acquisition, helping accelerate the technology and communication vertical.

"That said, these tailwinds could be offset by client-specific issues and delays in rampup of large deals. We expect an EBIT margin contraction of 210bps QoQ," ICICI Securities said.

TechM Q1 results preview

ICICI Securities said it expects TechM to log Q1FY27 revenue growth of 1.1 per cent QoQ CC (0.7 per cent QoQ in dollar terms) due to a rampup of strong large deal wins in FY26, partly offset by seasonal weakness in the Comviva business.

The growth is seen led by communication, BFSI and retail. Softness in automotive may continue, the brokerage warned.

"The hi-tech vertical’s performance is expected to be volatile through FY27 due to lower IT spending by technology giants, in our view. We envisage EBIT margin expanding by 30bps QoQ to 14.1 per cent led by continued benefit from operating efficiencies from Project Fortius and currency movement benefit, partly offset by employee expenses restructuring and headwinds from large deal ramp-up," ICICI Securities said. Deal TCV is seen in the range of $900–1,000 million.

LTM Q1 results preview

ICICI Securities said LTM’s revenue may grow 0.3 per cent QoQ CC, lower than the 1.5 per cent QoQ CC that it was building in at the start of the quarter. This is likely due to 1 per cent impact from a slowdown in decision making in the Middle East; and softness in travel and hospitality.

"We note that its top BFSI client is on the path to recovery and the top technology clients are growing well. The consumer vertical’s growth is expected to be healthy led by a ramp-up of recent large deal wins. LTM also won a USD 100mn, 7-year deal from a Europe-based medical technology company," ICICI Securities said.

The broking firm sees LTM to log TCV at $1.5 billion, in-line with its past four quarter average run-rate.

Mphasis Q1 results preview

ICICI Securities estimated Mphasis to report 1.8 per cent QoQ CC growth in Q1FY27 led by continued strong growth momentum in BFS and insurance. IT sees some softness in Mphasis' logistics and transportation verticals due to a secondary impact from the West Asia war. It expects technology vertical's revenues to be stable. It noted that two-month contribution from TAP acquisition of $0.3 million is likely in Q1.

"With strong TTM deal bookings (2x YoY) and client-specific issues in the logistics vertical now in the base, we expect revenue growth momentum to continue, implying 8–12 per cent YoY CC growth for FY27E. Deal bookings in Q1FY27E should be $400–450 million. EBIT margins, excluding cashflow hedges, may see a 30bps QoQ dip to 16.3 per cent," it said.

WhatsApp Usernames faces India scrutiny: Govt halts roll out, gives Meta 3 days to explain

WhatsApp Usernames faces India scrutiny: Govt halts roll out, gives Meta 3 days to explain Adani Ports shares at record high: Firm issues Q1 and June operational updates

Adani Ports shares at record high: Firm issues Q1 and June operational updates  BTS' Suga reportedly turned one investment into a 40x jackpot; here's how

BTS' Suga reportedly turned one investment into a 40x jackpot; here's how PM Modi, Japan PM Takaichi to jointly inaugurate Maruti Suzuki’s ₹35,000 crore Kharkhoda plant

PM Modi, Japan PM Takaichi to jointly inaugurate Maruti Suzuki’s ₹35,000 crore Kharkhoda plant  Buffett delays annual donation to Gates Foundation amid questions over its Epstein links: Report

Buffett delays annual donation to Gates Foundation amid questions over its Epstein links: Report India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump

India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks

Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt!

TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt! Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities

Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed!

Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed! Vedanta Oil, Vedanta Iron, Vedanta Power shares hit fresh highs; key things to know

Vedanta Oil, Vedanta Iron, Vedanta Power shares hit fresh highs; key things to know APL Apollo Tubes shares: Q1 FY27 volumes hit by slow demand; check brokerages' views, targets

APL Apollo Tubes shares: Q1 FY27 volumes hit by slow demand; check brokerages' views, targets YES Bank, SBI, ICICI Bank, HDFC Bank, BoB, DCB: Check target prices for top banking stocksBTS' Suga reportedly turned one investment into a 40x jackpot; here's how

YES Bank, SBI, ICICI Bank, HDFC Bank, BoB, DCB: Check target prices for top banking stocksBTS' Suga reportedly turned one investment into a 40x jackpot; here's how ZEE Entertainment share price: Why ZEEL stock fell 5% today?

ZEE Entertainment share price: Why ZEEL stock fell 5% today?