Varun Beverages share price today

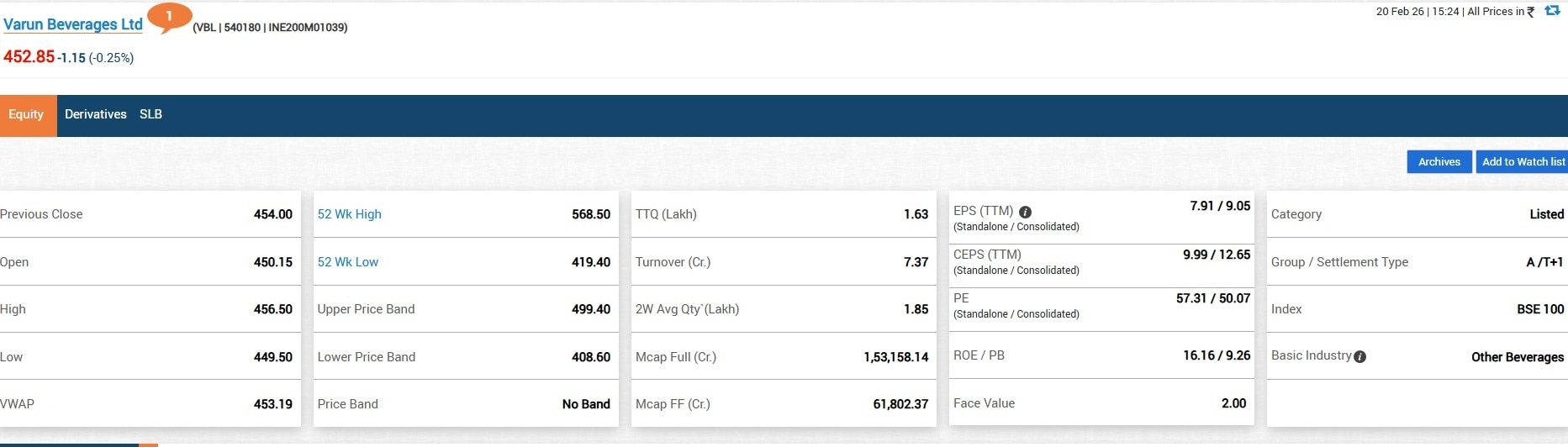

Varun Beverages share price today Shares of Varun Beverages have remained unaffected by the Q4 results announced in the beginning of this month. Instead, the PepsiCo bottler has carried forward losses in the stock market from 2025 to the current year. The FMCG sector stock slipped 23.14% last year. This year too, the stock is down over 8% as investors await recovery in their beverages stock bet.

Motilal Oswal has a price target of Rs 550 on the Varun Beverages stock.

It expects the company to deliver double-digit domestic volume growth in CY26. The brokerage's optimism emanates from strategic innovation, capacity investments, and premiumisation initiatives, which position the firm to deliver double-digit domestic volume growth in CY26. The brokerage expects margins to stabilise near current levels despite near-term realisation pressures.

"We expect a CAGR of 13%/13%/16% in revenue/EBITDA/PAT over CY25-27. We value the stock at 45x CY27E EPS to arrive at a TP of Rs 550. We reiterate our BUY rating on the stock," said Motilal Oswal.

The stock is under bear attack with shares of the Pepsico bottler trading lower than the 5 day, 10 day, 20 day, 30 day, 50 day, 150 day and 200 day simple moving averages.

In the current session, Varun Beverages stock was trading 0.33% higher at Rs 456.50 against the previous close of Rs 454. A total of 1.27 lakh shares of the firm changed hands, amounting to a turnover of Rs 5.74 crore. Market cap of the firm stood at Rs 1.54 lakh crore.

Brokerage JM Financial stated that management is optimistic about India volumes/profitability and Africa opportunity. It said the upcoming summer season will be key.

"Going forward, assuming summer season turns out to be normal, then management remains confident about delivering double-digit volume growth and reduction in the volume-value gap in India business. Going ahead, likely uptick in volumes should lead to better mix, fixed cost absorption and support overall margins," said the brokerage.

JM Financial has a buy call on the stock with a price target of Rs 550.

The brokerage expects a CAGR of 13%/13%/16% in revenue/EBITDA/PAT over CY25-27.

"We value the stock at 45x CY27E EPS to arrive at a target price of Rs 550. We reiterate our BUY rating on the stock," said the brokerage.

Can China really take down 'Sudarshan Chakra'? PLA's latest bold claim against India's S-400

Can China really take down 'Sudarshan Chakra'? PLA's latest bold claim against India's S-400 Cancer is leaving more children without mothers; India among six hardest-hit countries, says WHO

Cancer is leaving more children without mothers; India among six hardest-hit countries, says WHO RAM shortage declines global PC shipments down to 4.9%, Apple gains market share

RAM shortage declines global PC shipments down to 4.9%, Apple gains market share India renews lobbying deal with Trump ally Jason Miller for Rs 17 crore

India renews lobbying deal with Trump ally Jason Miller for Rs 17 crore, which it describes as the first integrated cyber platform developed by a professional services firm.") As AI reshapes cyber threats, EY bets on IP-led cyber platforms over traditional consulting

As AI reshapes cyber threats, EY bets on IP-led cyber platforms over traditional consulting Dubai Real Estate Outlook 2026: Why Rizwan Sajan Says Prices Could Surge After September

Dubai Real Estate Outlook 2026: Why Rizwan Sajan Says Prices Could Surge After September Delhi-NCR Monsoon Misery Returns: Why Does Every Spell Of Rain Bring The Same Crisis?

Delhi-NCR Monsoon Misery Returns: Why Does Every Spell Of Rain Bring The Same Crisis? Why SBI Mutual Fund Is Going Public: Top Executives Answer Key Investor Questions

Why SBI Mutual Fund Is Going Public: Top Executives Answer Key Investor Questions Sony INZONE H6 Air Gaming Headphones Unboxing

Sony INZONE H6 Air Gaming Headphones Unboxing ISOIN Wealth Discusses ICICI Prudential Multi-Asset Active FoF

ISOIN Wealth Discusses ICICI Prudential Multi-Asset Active FoF Sensex, Nifty trim gains but settle higher; what's next for the market?

Sensex, Nifty trim gains but settle higher; what's next for the market? Adani Enterprises shares gain as group forays into low-carbon chemical production

Adani Enterprises shares gain as group forays into low-carbon chemical production  Kalyan Jewellers shares zoom 25% in two days; is more steam left?

Kalyan Jewellers shares zoom 25% in two days; is more steam left? TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details

TCS Q1 results: Net profit rises to ₹13,349 crore, revenue up 14% | Quarterly earnings details TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date

TCS Q1 FY27 results: Rs 12 per share interim dividend announced; check record date