The recent data shows that the country's GDP shrank by nearly 24 per cent in the June quarter

The recent data shows that the country's GDP shrank by nearly 24 per cent in the June quarterBorrowers are facing the maximum brunt of the pandemic COVID-19. The recent data shows that the country's GDP shrank by nearly 24 per cent in the June quarter compared to the same period last year. This shows the loss of income is a reality for a large number of people looking for respite from debt burden amid financial stress. The universal moratorium of loans, which was offered by the RBI in April, ended on August 31. To give relief to the borrowers still facing difficulties in repaying their loans, the central bank has now come up with loan restructuring facility. It will allow borrowers to contact their lenders and discuss a new repayment plan that may include EMI holiday or increase of tenure and reduction of EMIs, among other options. However, each choice will have its consequences in terms of increased burden of interest payment. We tell you how these options will impact your finances and how you should go about selecting a right option.

Who can use retail loan restructuring?

The restructuring offer is meant to allow a breathing space to people significantly affected by the coronavirus-induced economic slowdown. "With this facility, banks can reschedule payments, convert interest into some other credit facility, and even provide a moratorium of up to two years. Not only that, the lender can also change the tenure based on the resolution if that can help the borrower repay the loan comfortably. Banks can reduce the equated monthly instalment (EMI) if you are facing salary cuts," says Rishi Mehra, CEO, Wishfin.com.

Multiple kinds of loans are extended by the banks. So, you must know what all loans are eligible for the restructuring. "The one-time restructuring of loans has been allowed for retail, corporate and MSME loans across all public, private, rural and co-operative banks, NBFCs, and Housing finances etc," says Aarti Khanna, Founder and CEO, AskCred.

"The intent of this scheme provided by the RBI is to help those borrowers who were regularly repaying their loans (standard on repayment as of March 31, 2020), but today are unable to repay because of the unquantified impact of the sudden lockdown due to the COVID-19 pandemic whereby they could not conduct their business as usual. Such customers have been given room for restructuring their loans, which will not be classified as a non performing asset," she adds.

How this restructuring is different?

Loan restructuring has always been a tool but this time it will work differently. Earlier this facility was allowed mostly when the borrower defaulted on repayment and hence the credit history of the borrower was negatively impacted. However, the current restriction is offered only to the ones who did not miss any repayment till March 31, 2020.

Very soon the RBI is expected to come up with standard guidelines as to how exactly this facility will be implemented. "Earlier the terms were customised and dictated by the bank whereas in the new scheme, specific two-year cap has to be followed and a special committee is also being formed that would be validated by Mr K V Kamath to ensure and approve seamless process and plans. This would bring in a standardised approach," says Khanna of AskCred.

How to get the restructuring done

Borrowers who are facing challenges in repayment will have to approach their lenders. "To get the benefits of loan restructuring, borrowers must get a resolution plan sanctioned before December 31, 2020. The lender will then need to implement it within 90 days. The restructured loan will continue to remain standard till the time the borrower conforms to the resolution plan. This means the lender won't report to the credit bureau that the borrower has defaulted, thereby preventing the credit score of the concerned individual from going down which could happen otherwise," says Mehra of Wishfin.com

However, this facility may not be entirely based on the request of the borrowers as lenders will also do their due diligence. "The lender would like to be convinced that you are genuinely struggling to pay your loans. For that, it might ask borrowers to submit the latest income statements such as salary slip (salaried), profit & loss account statement (self-employed). The lender will check these statements thoroughly before deciding whether to benefit you with loan restructuring or not," says Mehra.

Problems a borrower may face

Though the restructuring offer is a welcome relief at this point of time, but borrowers need to be completely sure of their future repayment plan and negotiate accordingly with the lending institution.

It may bring a great relief now, but any default in future could prove costly. "If thereafter the borrower misses a single payment, the lending institution will follow up from the first month inself and recurrent non-payment will land the borrower in deeper debt trap and also severely impact the overall credit profile of the borrower. Apart from that the borrower may even lose the collateral pledged in case of a secured loan. Co-applicants and guarantors credit profile can also be severely impacted at the same time," says Khanna of AskCred.

What works better - EMI holiday or reduced EMI?

If you can continue your loan repayment with little hardship and expense reduction then it would be the best course of action. However, if it does not help, you can go for loan restructuring. "If you are finding it hard to make your loan payments due to salary cuts and other financial problems, you can opt for the scheme and benefit from it," says Mehra of Wishfin.com

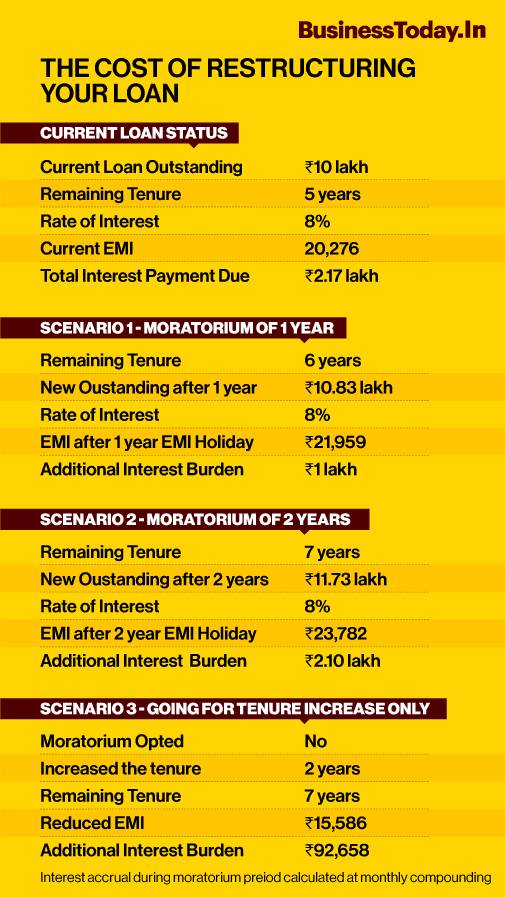

When going for a restructuring you have to be mindful of the cost in terms of higher interest outflow. Easier the repayment higher would be the total interest that you would end up paying. For the same amount of Rs 10 lakh loan outstanding with five-year remaining tenure you will end up paying an additional interest amount of Rs 2.10 lakh if you opt for the easiest option of two-year EMI holiday. If you go for the one-year EMI holiday you will be paying Rs 1 lakh of additional interest. However, if you just go for the tenure increase of two years and keep paying the reduced EMI you will only pay Rs 92,658 as additional interest.

So, in terms of interest cost the EMI holiday is the costliest option. Therefore, your preferred order should be increase of tenure, lowest period EMI holiday and as a last resort should you go for two-year EMI holiday which is the longest relief you can get under the current scheme.

Also Read: India's GDP contracts 23.9% in Q1; construction, manufacturing, trade bear the brunt

Also Read: Drop in Q1 GDP on expected lines; India on a V-shape recovery path: CEA K Subramanian

'US will bomb Iranian bridges, power plants if ships attacked in Hormuz': Trump warns Tehran again

'US will bomb Iranian bridges, power plants if ships attacked in Hormuz': Trump warns Tehran again 'Will respond to Wangchuk's letter': JP Nadda reads out list of paper leaks in Opposition-ruled states

'Will respond to Wangchuk's letter': JP Nadda reads out list of paper leaks in Opposition-ruled states China's global economic rise is 'remarkable'; India overtakes US in world savings: EAC-PM report

China's global economic rise is 'remarkable'; India overtakes US in world savings: EAC-PM report Don't fear the market fall. Buy the volatility, says this fund manager — and here's why

Don't fear the market fall. Buy the volatility, says this fund manager — and here's why IndusInd Bank: Q1 a clear inflection point; bank well positioned to improve growth in coming quarters, says MD & CEO Rajiv Anand

IndusInd Bank: Q1 a clear inflection point; bank well positioned to improve growth in coming quarters, says MD & CEO Rajiv Anand After Vikram-1's Orbital Launch, What's Next For Skyroot?

After Vikram-1's Orbital Launch, What's Next For Skyroot? Can Andy Burnham Redefine India-UK Relations? New UK PM's Big India Vision Explained

Can Andy Burnham Redefine India-UK Relations? New UK PM's Big India Vision Explained Delhi Protests Surge: PM Modi Breaks Silence In NEET Paper Leak As Opposition Rallies!

Delhi Protests Surge: PM Modi Breaks Silence In NEET Paper Leak As Opposition Rallies! Trump's 100% Pharma Tariff Plan: How Will Indian Drugmakers Respond To The U.S. Move?

Trump's 100% Pharma Tariff Plan: How Will Indian Drugmakers Respond To The U.S. Move? Sagility Q1 Results: CFO Srinivas Mattapalli On 27.6% Revenue Growth, Margins & Outlook

Sagility Q1 Results: CFO Srinivas Mattapalli On 27.6% Revenue Growth, Margins & Outlook Sensex, Nifty extend losses for third day; investors lose Rs 4.24 lakh crore as market sentiment weakens

Sensex, Nifty extend losses for third day; investors lose Rs 4.24 lakh crore as market sentiment weakens IndusInd Bank Q1 FY27 profit jumps 72% YoY to Rs 1,037 crore; NII at Rs 4,685 crore

IndusInd Bank Q1 FY27 profit jumps 72% YoY to Rs 1,037 crore; NII at Rs 4,685 crore Adani Green Energy Q1 earnings: Net profit rises 19%, revenue at Rs 4,280 crore

Adani Green Energy Q1 earnings: Net profit rises 19%, revenue at Rs 4,280 crore  Tata Elxsi shares hit five-year low; time to buy, sell or hold?

Tata Elxsi shares hit five-year low; time to buy, sell or hold?  Autoline Industries shares: Is it time to buy this stock? What technical chart signals

Autoline Industries shares: Is it time to buy this stock? What technical chart signals