While the gap between Direct and Regular plans may appear modest over five years, it widens sharply over longer holding periods.

While the gap between Direct and Regular plans may appear modest over five years, it widens sharply over longer holding periods. While the gap between Direct and Regular plans may appear modest over five years, it widens sharply over longer holding periods.

While the gap between Direct and Regular plans may appear modest over five years, it widens sharply over longer holding periods.Hidden commissions in regular mutual fund plans can significantly erode long-term investor wealth, with most investors losing more than a quarter of their potential gains over a decade, according to a new study by 1 Finance Research.

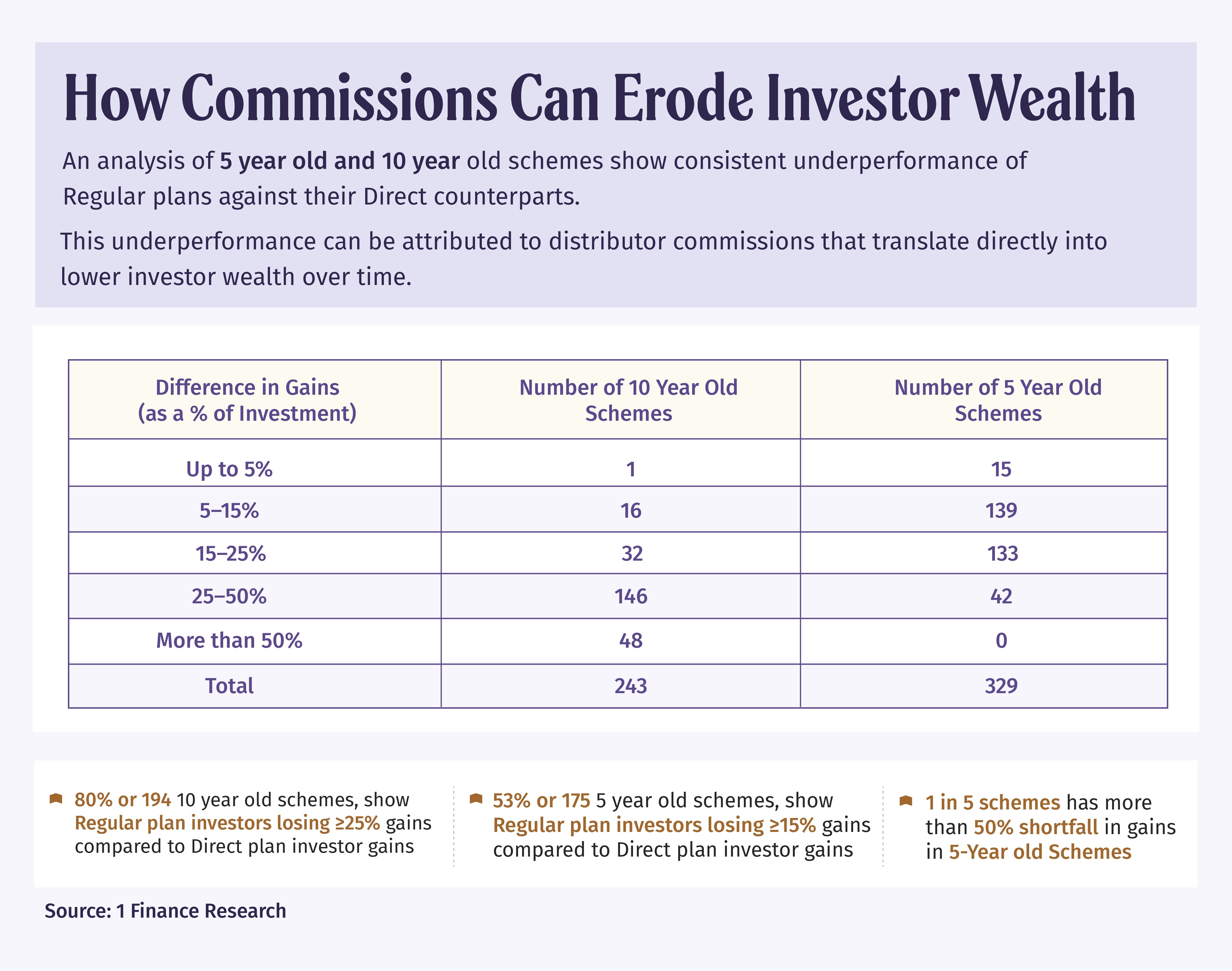

The report found that over a 10-year holding period, more than 80% of equity mutual fund schemes delivered at least 25% lower wealth to investors in Regular plans compared with Direct plans of the same fund. Nearly one in five schemes showed a wealth gap of over 50%, driven purely by the compounding impact of higher expense ratios embedded in Regular plans.

The study underscores how distributor commissions, though often overlooked, remain one of the most persistent drags on investor returns. These commissions are built into the total expense ratio (TER) of Regular plans, reducing annual returns year after year, even though the underlying portfolio is identical to that of Direct plans.

Data highlights the scale of this erosion. Among 10-year-old schemes, 80%, or 194 out of 243, delivered at least 25% lower gains to Regular-plan investors, while nearly one in five schemes showed a shortfall of over 50%. The trend is visible even over shorter periods: in five-year-old schemes, 53% posted at least a 15% gap in gains, entirely due to higher expenses.

The report presents a comparative analysis of actively managed equity mutual funds across four major categories — flexi-cap, large-cap, mid-cap and small-cap — compared with their respective AMFI-recognised benchmarks.

The analysis is based on whether a fund outperformed or underperformed its benchmark over four durations: one year, three years, five years and ten years.

The message is clear - small annual cost differences compound over time, turning commissions into one of the biggest drags on long-term investor returns.

“Cost differences may look small in a single year, but when they persist across market cycles, they meaningfully reshape investor outcomes,” said Rajani Tandale, Senior Vice President, Mutual Fund at 1 Finance. “The erosion in Regular plans is structural, not episodic.”

Using AMFI NAV data, the study compared Direct-Growth and Regular-Growth options across major equity fund categories. To isolate the impact of costs, researchers assumed a uniform ₹100 investment from the same starting date. Schemes with at least five years of history were used for medium-term analysis, while those with 10 years were examined for long-term impact.

The findings show that wealth erosion from commissions accelerates over time rather than progressing linearly. While the gap between Direct and Regular plans may appear modest over five years, it widens sharply over longer holding periods. Over a five-year horizon alone, more than half of the schemes delivered at least 15% lower wealth to Regular-plan investors.

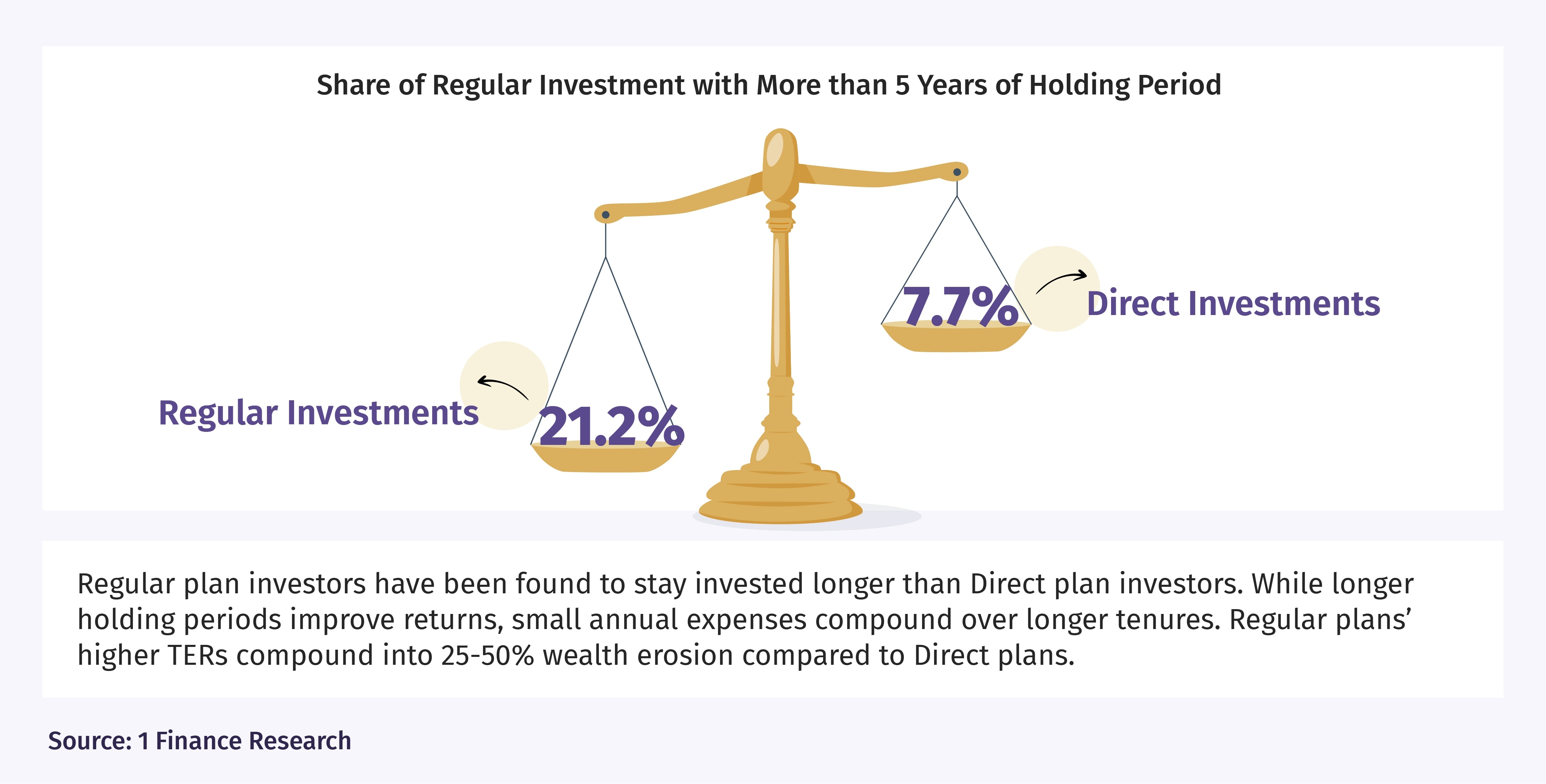

The data also reveals a striking paradox in mutual fund investing: Regular-plan investors tend to stay invested longer, yet end up with significantly lower wealth than Direct-plan investors. According to the findings, 21.2% of Regular investments are held for more than five years, compared with just 7.7% of Direct investments. While longer holding periods usually enhance returns through compounding, the higher TERs embedded in Regular plans work in the opposite direction.

These seemingly small annual costs compound relentlessly over time, translating into a 25–50% erosion of investor wealth compared with Direct plans holding the same portfolio. In effect, investor discipline in staying invested is undermined by the drag of commissions paid to distributors.

Notably, the gap is not a function of poor fund selection. “The underperformance is driven by costs, not capability,” the report said, pointing out that the same fund house and portfolio can generate sharply different outcomes purely based on the plan chosen.

Despite this, Regular plans continue to dominate assets. As of March 2024, about 21.2% of Regular-plan investments were held for over five years, compared with just 7.7% for Direct plans. This persistence reflects the strength of commission-led distribution, even as evidence mounts of its long-term cost to investors.

The study concludes that choosing between Direct and Regular plans is as important as choosing the fund itself. Small annual cost differences, it warns, can compound into substantial wealth gaps—making expense awareness a critical part of long-term investing discipline.

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's

Same 43°C temperature, different reality: Why Europe's heatwave is more deadly than India's 'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means

'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore

From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure