SIP and SWP are like two sides of a coin, each representing distinct concepts. SIP is a method for investing, whereas SWP is a strategy for withdrawing funds.SIP and SWP are like two sides of a coin, each representing distinct concepts. SIP is a method for investing, whereas SWP is a strategy for withdrawing funds.

SIP and SWP are like two sides of a coin, each representing distinct concepts. SIP is a method for investing, whereas SWP is a strategy for withdrawing funds.SIP and SWP are like two sides of a coin, each representing distinct concepts. SIP is a method for investing, whereas SWP is a strategy for withdrawing funds.Retirement in India is evolving from a time of slowing down to an era of pursuing passions, travel, and financial independence. For many, it’s no longer about simply stopping work but about living life on their own terms — and smart financial tools are making this possible.

Arsh Khanna, Financial Counsellor, shares the story of a retired couple in Gurgaon who perfectly capture this sentiment. “They told me over chai, ‘Humne poori zindagi paisa kamaaya… ab paisa humein sukoon de raha hai.’ They weren’t talking about some big jackpot win, but about a simple yet powerful combination of investments: SIPs and SWPs,” Khanna says.

The couple had diligently invested through SIPs — Systematic Investment Plans — during their working years. “SIPs quietly built their wealth month after month,” explains Khanna. “It’s a disciplined way of investing small amounts regularly into mutual funds, which over the years, compounds into a significant corpus.”

But the real magic begins after retirement with SWPs — Systematic Withdrawal Plans. Khanna elaborates, “SWPs help retirees convert their accumulated corpus into a steady monthly income. It’s like getting a ‘retired salary,’ funding travel, hobbies, or simply a stress-free lifestyle without worrying about cash flows.”

For the Gurgaon couple, SWPs mean there’s no awkward silence when the restaurant bill arrives or guilt over treating themselves to small luxuries. “It’s about peace of mind and knowing you’ve earned the life you’re living,” Khanna says.

What surprises many is that retirement doesn’t have to wait until 60. “We’ve helped professionals retire by 50 — and some even by 45 — not because they struck it rich, but because they planned well,” Khanna notes. “The key is aligning investments with your lifestyle goals, not just numbers on a spreadsheet.”

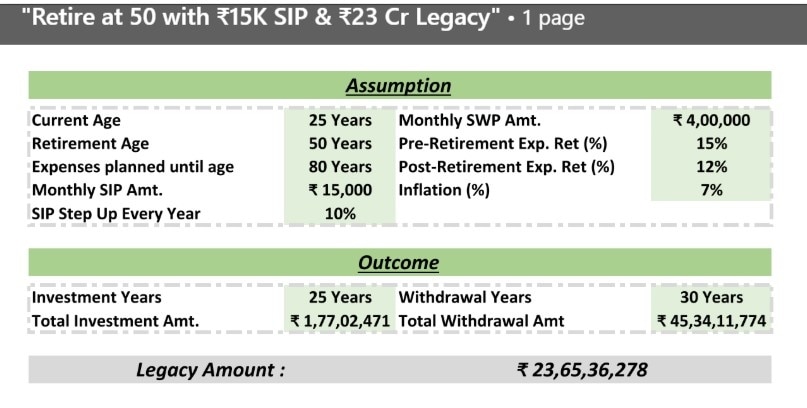

Khanna shares a practical example to illustrate the power of disciplined investing. “Imagine you start a SIP of Rs 15,000 every month,” he says. “Over a few decades, this can grow into a sizable corpus. Post-retirement, you could potentially withdraw Rs 4,00,000 monthly for 30 years through an SWP and still leave behind a legacy exceeding Rs 23 crore for your next generation.”

Of course, these figures depend on factors like investment returns, inflation, and market volatility, but the principle remains robust: discipline and planning can turn modest savings into financial freedom.

He advises young earners and mid-career professionals alike to start early. “Every year you delay could mean significantly lower wealth at retirement,” he warns. “SIPs instill discipline, while SWPs ensure that your retirement corpus lasts as long as you do — and often longer.”

For those wondering how soon they could realistically retire in India, Khanna recommends seeking guidance. “A financial advisor can help map out a plan tailored to your aspirations — whether your dream is to retire early in Goa or simply enjoy a stress-free life in your hometown,” he says.

Retirement, as Khanna sums it up, “shouldn’t be about worrying if you’ll have enough. It should be about knowing you do — and finally living the life you deserve.”

— the coaching institute acquired by Think & Learn in 2021.") Can Byju Raveendran still shape Byju's insolvency outcome?

Can Byju Raveendran still shape Byju's insolvency outcome? Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022

Did you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022 Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next?

Tomatoes push up Thali costs in May by 7% -- will onions and potatoes be next? Annamalai set to quit BJP? Here's a look at the party's most high-profile exits

Annamalai set to quit BJP? Here's a look at the party's most high-profile exits") Which company has been called the next trillion-dollar company?

Which company has been called the next trillion-dollar company? SEBI’s Big Crackdown! Rajesh Exports Faces Massive Revenue Inflation Allegations

SEBI’s Big Crackdown! Rajesh Exports Faces Massive Revenue Inflation Allegations Maruti Suzuki Unveils Flex Fuel WagonR | India's Ethanol Revolution Gets Real

Maruti Suzuki Unveils Flex Fuel WagonR | India's Ethanol Revolution Gets Real Market Rebound After Early Fall! Is It Time To Buy The Dip Again? | Siddharth Khemka

Market Rebound After Early Fall! Is It Time To Buy The Dip Again? | Siddharth Khemka Sanctions Are an Opportunity | St Petersburg Tourism Chairman Exclusive

Sanctions Are an Opportunity | St Petersburg Tourism Chairman Exclusive ‘Nurture Your Roots, Spread Your Wings’: Sri Sri Ravi Shankar’s Message At SPIEF

‘Nurture Your Roots, Spread Your Wings’: Sri Sri Ravi Shankar’s Message At SPIEF 'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha

'Is this the biggest stock market scam ever? Move over, Harshad Mehta ...' — asks Sanjay Jha Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know

Thangamayil Jewellery shares zoom 18% to hit record high; here's what investors should know CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why

CG Power, Hitachi Energy India, GE Vernova shares rise up to 4% today; here's why  Bharat Forge sets record date for FY26 dividend payment; check detailsDid you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022

Bharat Forge sets record date for FY26 dividend payment; check detailsDid you know? Rajesh Exports was one of the awardees of Rs 18,100 cr PLI scheme in 2022