Urban mobility in India is on the cusp of transformative change in the wake of COVID-19, driven by the need for social distancing and optimised expensesUrban mobility in India is on the cusp of transformative change in the wake of COVID-19, driven by the need for social distancing and optimised expenses

Urban mobility in India is on the cusp of transformative change in the wake of COVID-19, driven by the need for social distancing and optimised expensesUrban mobility in India is on the cusp of transformative change in the wake of COVID-19, driven by the need for social distancing and optimised expensesAs people learn to co-exist with the coronavirus, a tantalising question emerges for the struggling transport industry-will people change the way they commute?

Boston Consulting Group (BCG) conducted five waves of surveys with over 12,000 respondents since March 2020 to understand people's travel concerns and priorities during and after the lockdowns.

The same (survey) found that even though respondents are becoming more assured about their future income and less worried about venturing out (by Wave 5 survey, 53 percent respondents had resumed travel for work), there is a significant shift in preferences that will require innovative approaches to serve them.

Also Read: Coronavirus impact: Transport, construction sectors likely to be worst-hit

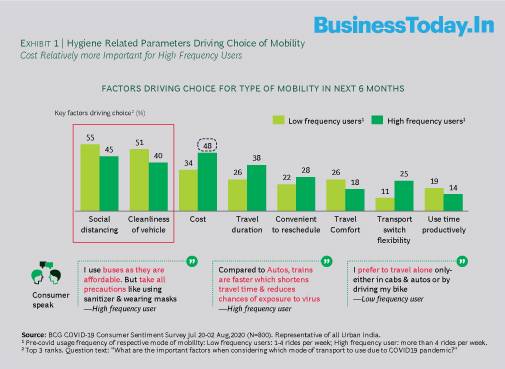

Consumers balance social distancing and costs

As expected, social distancing and hygiene are the two most important criteria, more than cost itself. While public transport was the dominant way India commuted pre-COVID, 71 per cent respondents now find public transport like buses and metros risky while this number dropped to 27-28 per cent with private cars and two-wheelers.

However, for high frequency commuters, who travel four or more times a week, costs continue to have a (slightly) higher importance in addition to social distancing and cleanliness (Exhibit 1). Consequently, they are more likely to continue using hired mobility/public transport as long as safety is addressed.

Preference for lower-cost personal vehicles

The stress on social distancing and hygiene is likely to increase preference for personal vehicles. 57 per cent of respondents expect to spend similar or more on cars and 64 per cent on two-wheelers in the coming months (Exhibit 2). However, consumers may optimise their spending and buy a less expensive model or consider purchasing a used vehicle.

Post-COVID, recovery is expected across both public and personal options. 80 per cent of polled respondents are expecting to spend similar or more compared to pre-COVID times across different modes of transport (Exhibit 3).

However, this will need to be watched closely given the possibilities of fundamental changes in underlying transportation demand with employers exploring long-term work-from-home models.

Re-imagining urban mobility

The evolving customer mindset points out to two key drivers in the short-to-medium term:

The interplay of these drivers has several implications for industry players; a few are outlined here.

New vehicle sales: OEMs can enhance focus on entry level variants and provide flexible, innovative financing (for example, EMI moratoriums, back-ended EMIs, etc.) to even induce fence-sitters, who may otherwise defer their purchases.

Subscription model: Many consumers may eventually want to return to shared mobility, but in the short-term, a subscription model with shorter tenures and all-inclusive monthly payouts could provide a good tradeoff to access a private vehicle without capital outlay. Once tested, this model can become a prominent part of the

landscape even in the post-pandemic world.

Digitisation of sales/service: OEMs need to really leverage digital extensively across discovery, testing, selection, purchase, financing and after-sales. This requires innovation in the operating model for e.g., service being delivered in a hub-spoke model with pick-up and drop, and AR delivering dealership experience at home.

Used vehicles: More consumers are likely to purchase used vehicles to optimise costs. This market is not so well organised in India and presents an opportunity for larger OEMs and third-party aggregators. If operators can focus on demand aggregation and upgrade their consumer propositions, such as providing refurbishment and certification of vehicles, financing packages and after-sales experiences, it will help drive loyalty and pride in ownership and help grow the used vehicle market.

Also Read: COVID-19 ushering in change for mobility segment, consumer behaviour will transform: Chandrasekaran

Shared mobility: The basics will continue to matter. Health of passengers (and staff) will remain a top priority. Practices such as partition between driver and passengers and frequent vehicle sanitisation will become the norm.

However, this is also a good time for providers to experiment with new mobility models addressing new customer demand spaces, such as essential workers, cargo and food delivery, weekend rentals for consumers, day long rentals for travelling salespersons etc.

Some experiments have already begun, such as two-wheeler fleets for the delivery economy. Innovations such as mixed-model mobility solutions where the same assets are used for multiple services over the week can help fleet operators drive up asset utilisation, drive down unit prices for consumers and deliver better economics.

Urban mobility in India is on the cusp of transformative change in the wake of COVID-19, driven by the need for social distancing and optimised expenses. Key constituents of the urban transport industry- OEMs, used vehicle aggregators and mobility players-will have to mount a differentiated response and embrace key changes to not only return to health but also propel urban mobility into a new, exciting and future-ready trajectory.

(Vikram Janakiraman is a Managing Director and Partner at BCG, Natarajan Sankar is a Managing Director and Partner at BCG, Aditya Khandelia is a Principal at BCG.)

Iranian crude re-enters global markets as US grants 60-day waiver; WTI slips below $74

Iranian crude re-enters global markets as US grants 60-day waiver; WTI slips below $74 WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED

WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED India wants to make more at home. So why are imports still surging?

India wants to make more at home. So why are imports still surging? From BrahMos to Akashteer: UAE explores buying India's frontline defence systems

From BrahMos to Akashteer: UAE explores buying India's frontline defence systems No rank on CV? IITs' new placement rule asks students to drop JEE, GATE scores. Here's why

No rank on CV? IITs' new placement rule asks students to drop JEE, GATE scores. Here's why Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today

Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students

US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors?

Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors? UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports

UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era!

CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era! Sensex, Nifty trim gains but settle higher; what's ahead for investors?

Sensex, Nifty trim gains but settle higher; what's ahead for investors? Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding

Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding Explained: Open market share buybacks are back, what this means for Indian investors

Explained: Open market share buybacks are back, what this means for Indian investors Kirloskar Brothers shares jump 7%; key technical levels to watch out for

Kirloskar Brothers shares jump 7%; key technical levels to watch out for CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies

CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies