A lot of skeptics announced this as the doomsday for the Indian e-tailing market (and consumer internet in general) - with their views being further fuelled by the devaluation of Flipkart, the bellwether of the industry, by various funding agencies.

At this point, it would be prudent to take a step back and answer certain pressing questions: How bad was the year 2016 in reality? What were the reasons for the challenges faced by the industry during the year? How would the market evolve going forward?

Considering that the e-tailing industry grew at 100+ per cent for two consecutive years before 2016, most analysts have forecasted the 2020 numbers to be $65-120 Billion, with RedSeer estimates putting the figure at $80 Billion. For these numbers to be achieved, the industry would need to grow at 45 per cent CAGR over the next four years, from the exit GMV run rate of 2016. The billion-dollar question: Is such a strong, sustained growth achievable for the industry?

This question can be split into two parts: One, what pulled the growth down in 2016 and were these levers fundamental in nature or one-off events?

Two, how do the fundamental drivers, which will determine the growth for the next few years, look like for the industry?

Let's attempt to answer the first part of the question in detail, as a year-end review.

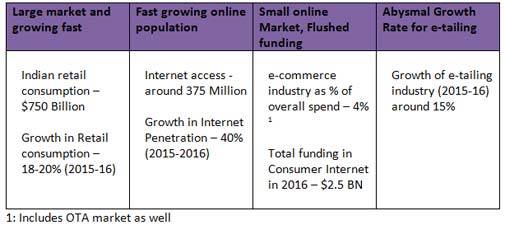

1: Includes OTA market as well

It's not every day you see such figures (as in Table 1) in context of fast growing industry.

Despite fast growing consumer spending, globally fastest growing internet penetration and a funding splurge by investors, why did the Indian e-tailing industry fail to deliver on the expected growth metrics in 2016?

The answer to this question takes us to a combination of events which happened in 2016, a rare happening in an industry and more so in such a short interval of time.

'Speed-Breakers' of 2016

A. Circular trading Correction: Due to heavy discounting by e-tailers throughout 2015, there was a significant percentage of GMV (varying estimate puts this numbers to be 20- 30 per cent), which was being driven by retailers and wholesalers buying goods and in-turn selling it to the end customers; with some e-tailers facing this issue more than others. However, post the completion of the festive season 2015, e-tailers started to clean this mess, resulting in an immediate fall in retailer orders and bringing in a much-needed correction for the market

B. Market leader restructures: The first quarter of the year saw the mass exodus of senior leadership from Flipkart, followed by a quest on how to fill the gap and what the new leadership structure should be like. It took 3-4 months for Flipkart to fix the internal organization and associated strategies and they practically lost this time to do anything significant around growth. A flat growth for the leader in first two quarters contributed to pulling the market down.

C. The next one also slows down: Snapdeal, which was the second largest e-tailer by GMV share at the end of 2015, and was growing with the fastest rate, reversed its trajectory. It not only stopped growing but shrank significantly, to give up the second position to Amazon. While, there are various theories on what led to this drop, we believe it was caused by a combination of- a) industry wide circular trading correction, and b) new found discipline around cash burn, C) Focus on revenue vs. the GMV

D. Govt. Regulations on Discounting and marketplace: The first quarter of 2015 also saw another blow for the industry, in the form of the DIPP regulations on the extent of discounting and the per cent GMV contribution by captive selling arms of e-tailers. While, the first regulation put all the e-tailers in a fix for first few months on how to realign their strategy (which earlier was so heavily dependent on discounting), there was also heavy operation jugglery to be done to "manage" the 25 per cent limit on captive sellers- which again shifted the focus of the e-tailers from driving growth

E. Demonetization: Demonetization was the final big blow of 2016 for the e-tailing industry. In an industry, which relies so much on cash (65-70 per cent orders are CoD), demonetization put brakes on the momentum achieved post a successful October festive period. The industry lost around 20 per cent of the GMV in Nov and early December, and the growth from there-on was not so great.

With the above five levers pulling the growth down, it had a domino effect on a fragile and young industry, leading to further two more impacts:

1. Slow new customer acquisition: The leading players were focused on the market share fight, rather than going aggressive and creating new markets. This did lead to a change in the pecking order of e-tailers, but the new players didn't drive growth in the overall market- with the proof coming from the slowing growth in addition of first time customers

2. Funding Cease: The slowing macro of Indian e-tailing industry didn't please the global investors, particularly the mutual funds. This led to an uneasy calm in the funding cycle of big e-tailers, driving them to focus a lot more on controlling the cash burn, which in turn led to challenges in adding infrastructure, sellers and customers to the ecosystem

Now for the big questions: how do the fundamental drivers, which will determine the growth for the next few years, look for the industry? How do the year coming ahead and the much talked about 2020 look like? What will ensure that we do not see a repeat of 2016's timid growth rate?

Looking back at the major speed breakers of 2016, we see none of them are fundamental to the e-tailing industry. They are all external or organization-centric rather than "consumer's vote" on not going online to buy.

Therefore, we do not expect the repeat of DIPP regulation, demonetization, heavy correction due to circular trading and we might see the leadership order changing in the industry due to winning or losing strategies.

But the key message here is that the overall growth platform is fundamentally robust. Technology and internet will play a key role in Indian retail market going forward, especially considering that retail space is expensive and the customer offline shopping experience is not world class due to lagging infrastructure and poor selection.

E-tailing is here to stay and will surely transform the way we shop. How much and by when is the question.

(Author is the founder and CEO of RedSeer Management Consulting, a leading advisory firm working in the consumer internet sector.)

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market.") Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma

Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma From ‘embarrassing’ to impressive: Top Silicon Valley VC calls Sarvam praises Indic AI breakthroughs

From ‘embarrassing’ to impressive: Top Silicon Valley VC calls Sarvam praises Indic AI breakthroughs India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs

India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook

RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.”

Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.” Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation

Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact

RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’ BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates

Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates 'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag

'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag Bitcoin avoids $60,000 breakdown, still down over 50% from record high

Bitcoin avoids $60,000 breakdown, still down over 50% from record high