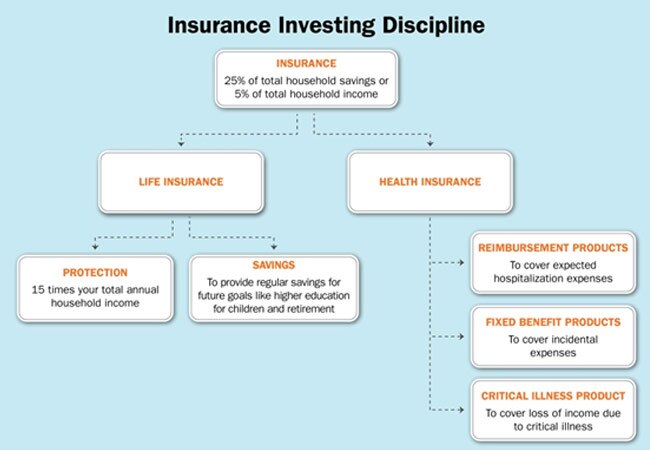

The earning members in an Indian middle-class household often do not have sufficient wealth in the early stages of their careers to enable them to achieve certain defined life goals such as buying a house, paying for higher education or saving for one's retirement. They aspire to accumulate this wealth through the course of their active working lives. Since meeting such defined goals is dependent on one's future earnings, it is imperative to safeguard those earnings against any eventuality; hence the emphasis on the importance of protection tools and their inter-relation with investment products.

While building one's insurance portfolio, one must also consider the risks of illnesses that may occur and hamper future earnings. It is important that the appropriate insurance products are chosen to offset this threat.

While the ideal situation would be to protect oneself from all uncertainties, one must also take into consideration the financial impact that ensues. Prioritization is the keyword while choosing life insurance solutions and one should always cover the most imminent risks first. A well-structured insurance portfolio not can only providefor one's needs at key life stages, but also help plan for a brighter tomorrow, today.

The author is CEO, Bharti AXA Life Insurance

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market

'Strengthens supply chains against China, support Rupee stability': Amitabh Kant says tariff cut to 18% gives India edge in US market.") Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma

Inside the India-US interim trade agreement: Reciprocal tariffs on India to come down to 18%, 0% duty on generic pharma India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs

India-US interim trade pact: From diamonds to silk — Full list of products under 18% tariffs IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’

IDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’, MRF, Hero MotoCorp, Mazagon Dock Shipbuilders and Power Grid Corporation of India, among others.") BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook

RBI Says Trade Deals With EU, US & Others Strengthen India’s External Sector Outlook Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.”

Jeffrey Sachs Praises Modi On India-US Trade Deal: “Trump Blinked, India Must Not Depend On U.S.” Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation

Agra’s ₹127 Cr Housing Project In Ruins: Flats For Poor Rot Before Occupation RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact

RBI Credit Policy LIVE Analysis | Aditya Pagaria Explains Rate Pause Impact TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week

TeamLease Q3 Results: Profit Jumps 47% As Margins Improve Despite Headcount LossIDBI Bank stake sale: Kotak Mahindra Bank says ‘has not submitted a financial bid’BDL, Mazagon Dock, MRF, Hindustan Copper, RVNL, others to turn ex-dividend next week Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates

Q3 results: HAL, Titan, M&M, HUL, ONGC, Lenskart to post earnings next week; check dates 'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag

'Think about it': Deepak Shenoy warns indices mask stress as majority of Nifty 500 stocks lag Bitcoin avoids $60,000 breakdown, still down over 50% from record high

Bitcoin avoids $60,000 breakdown, still down over 50% from record high