If you want safety but also want better efficiency from your money, Post Office and small savings schemes can be strong alternatives.If you want safety but also want better efficiency from your money, Post Office and small savings schemes can be strong alternatives.

If you want safety but also want better efficiency from your money, Post Office and small savings schemes can be strong alternatives.If you want safety but also want better efficiency from your money, Post Office and small savings schemes can be strong alternatives.For decades, fixed deposits (FDs) have been the default savings option for most Indian investors. If you wanted safety, guaranteed returns, and peace of mind, you simply opened an FD with your bank and left the money there. But today, many investors like you are beginning to realise that keeping all your savings in FDs may not be the smartest move anymore.

With interest rates on bank deposits largely in the 7%–8% range, several government-backed savings schemes are offering similar safety but with better returns, tax benefits, and stronger long-term compounding. Because these schemes are backed by the Government of India, they provide the same sense of security that attracts investors to FDs in the first place.

Why you may want to look beyond FDs

If most of your savings are in bank deposits, you are not alone. Many investors prefer FDs because they are simple and predictable. However, experts say relying only on FDs can limit your returns, especially when other guaranteed schemes are offering higher interest or tax advantages.

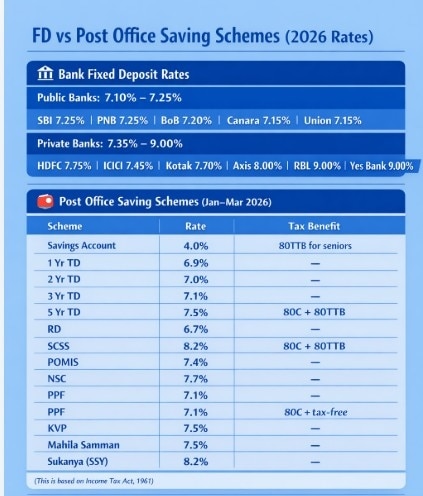

Recent FD rate data shows most public sector banks offering around 7.10%–7.25%, while private banks may offer slightly higher rates to attract deposits. But higher rates do not always mean better value, especially if the returns are fully taxable or if the bank is not considered as safe as a sovereign-backed scheme.

That is why financial planners now suggest that you should diversify your safe investments instead of putting everything into fixed deposits.

PPF, NSC, Time Deposits

If you want safety but also want better efficiency from your money, Post Office and small savings schemes can be strong alternatives.

The Public Provident Fund (PPF) is one of the most powerful long-term options available to you. It currently offers about 7.1% interest and comes with full tax benefits, meaning your investment, interest, and maturity amount are all tax-free. Over time, this tax advantage alone can make a big difference.

The National Savings Certificate (NSC) is another option if you want guaranteed returns along with tax deduction under Section 80C. It offers around 7.7% interest and is often used by investors who want stability but also want to reduce their tax liability.

If you prefer something similar to a bank FD, the Post Office Time Deposit works in the same way but comes with government backing and interest rates up to around 7.5%.

SCSS, Sukanya Samriddhi Yojana

Depending on your age and financial goals, some government schemes can give you even better returns.

If you are planning for retirement income, the Senior Citizen Savings Scheme (SCSS) offers around 8.2% interest, one of the highest among fixed-income options, and pays income regularly.

If you are saving for your daughter’s future, Sukanya Samriddhi Yojana (SSY) offers one of the highest interest rates among all government schemes along with tax-free maturity, making it a strong long-term choice.

For guaranteed growth without market risk, Kisan Vikas Patra (KVP) remains a simple option where your money doubles in a fixed period at current interest rates.

If you need regular income, there are options

Not every investor wants long lock-in periods. If you need steady cash flow, the Post Office Monthly Income Scheme (POMIS) pays interest every month, which many investors use as a substitute for FD interest income.

You can also look at RBI Floating Rate Bonds, where the interest changes with market rates, helping your returns stay relevant even when inflation rises.

Bank FD rates in March 2026

Experts say FDs remain safe, but the smarter approach is diversification across secure schemes that provide better returns, tax efficiency, and the power of compounding over time.

Latest fixed deposit (FD) rate data for March 2026 shows a clear gap between public sector and private sector banks, with private lenders offering significantly higher returns to attract deposits. Among public sector banks, FD rates are largely in the range of 7.10% to 7.25%, with State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank, Union Bank of India, Indian Bank, and Bank of India offering similar returns.

Private sector banks, however, are offering higher rates, ranging from 7.35% to 9%, depending on tenure and category. Banks such as HDFC Bank, ICICI Bank, Kotak Mahindra Bank, and Axis Bank are offering rates close to 7.5–8%, while smaller private lenders like RBL Bank and Yes Bank are offering up to 9%, making them the highest in the list.

The higher rates reflect strong competition for deposits as banks try to maintain liquidity. However, experts advise investors to balance returns with safety, as public sector banks are generally considered more secure despite slightly lower FD rates.

Smarter approach for investors today

Instead of choosing between FDs and other schemes, experts say you should think in terms of balance. Keeping some money in FDs for liquidity, some in PPF for long-term growth, and some in high-interest government schemes can give you better returns without taking extra risk.

In today’s interest-rate environment, the question for investors is no longer whether FDs are safe — it is whether relying only on FDs is enough.

Kotak Bank shares: MD and CEO Ashok Vaswani to step down; Saha looks best placed, says Nomura; target price

Kotak Bank shares: MD and CEO Ashok Vaswani to step down; Saha looks best placed, says Nomura; target price Aastha Spintex IPO opens today: Should you apply? Check price band, GMP, reviews & more

Aastha Spintex IPO opens today: Should you apply? Check price band, GMP, reviews & more 'Come forward and help us': Ketan's father appeals to witnesses present at Lohagad on day of murder

'Come forward and help us': Ketan's father appeals to witnesses present at Lohagad on day of murder YRF's next big drama could be mobile-only: Why the film company is betting on a new format

YRF's next big drama could be mobile-only: Why the film company is betting on a new format HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report

HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Netweb Technologies shares crash 8% despite fundraising plan

Netweb Technologies shares crash 8% despite fundraising plan  Hexaware Technologies shares gain 8% in early deals; here's why

Hexaware Technologies shares gain 8% in early deals; here's why  Persistent Systems–Nagarro deal: Key questions answered

Persistent Systems–Nagarro deal: Key questions answered Turtlemint Fintech Solutions make a weak stock market debut; shares lists at 11% discount

Turtlemint Fintech Solutions make a weak stock market debut; shares lists at 11% discount Persistent Systems shares dive 9% to hit 52-week low; here's why

Persistent Systems shares dive 9% to hit 52-week low; here's why