According to experts, employers will need to rebalance salary break-ups, especially for employees who currently draw large allowances or flexible components.

According to experts, employers will need to rebalance salary break-ups, especially for employees who currently draw large allowances or flexible components. According to experts, employers will need to rebalance salary break-ups, especially for employees who currently draw large allowances or flexible components.

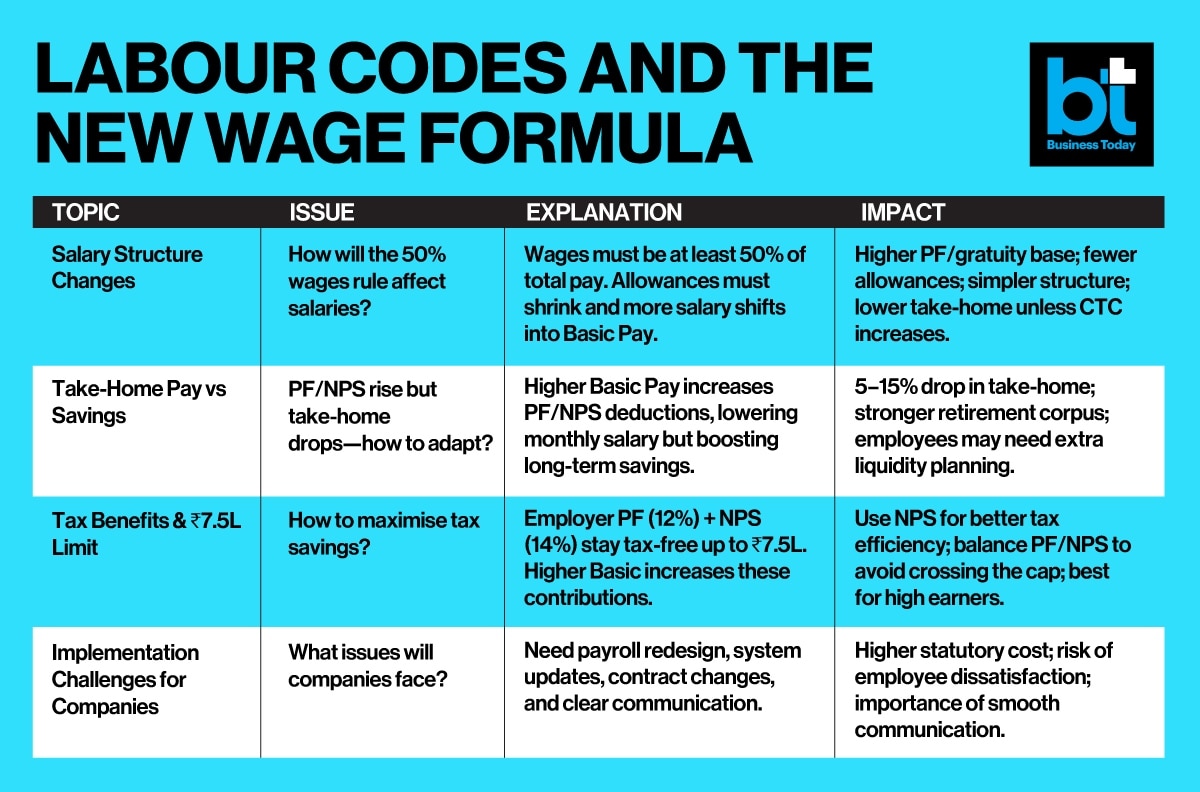

According to experts, employers will need to rebalance salary break-ups, especially for employees who currently draw large allowances or flexible components.If you’re a salaried employee, the new labour codes that kicked in on November 21 are likely to reshape the way your salary looks — and even how much you take home each month. While these codes don’t introduce brand-new tax deductions, they do change how your salary is defined, and that alone will have a big impact on PF, gratuity, pensions and your overall tax planning.

At the heart of the change is the Code on Wages, 2019. It introduces a single, uniform definition of “wages” — something experts say will completely reset how statutory benefits are calculated.

Ramachandran Krishnamoorthy, Director – Payroll Services at Nexdigm, explained that wages — consisting of basic pay, dearness allowance (DA) and retaining allowance — will now need to make up at least 50% of your total salary. “This will simplify salary structures and expand the scope of social security,” he said, adding that many allowances employees currently use for tax saving may no longer serve the same purpose under the new system.

What this means for you

The most immediate impact will be on compulsory savings. Because contributions to PF, gratuity and pension are linked to the wage component, these amounts will automatically rise. This could lead to a dip in monthly take-home pay, but experts believe the trade-off is worth it.

According to Pankaj Savla, Director at NPV Labour Law Solution, mid-career employees might end up with 20–30% higher retirement benefits over their lifetime. “Employees should treat the reduction in take-home salary as forced savings,” he said. He added that with its equity exposure and tax efficiency, NPS could become even more popular among those aiming for better long-term returns.

Choosing between new and old tax regimes

Here’s where things get interesting. With a higher basic salary, employer contributions to PF and NPS also increase — and these are exempt under the new tax regime. Krishnamoorthy pointed out that this makes the new regime more appealing for people who don’t claim many deductions.

But the old tax regime isn’t out of the game. A higher basic salary also increases HRA exemption, which is especially helpful for those paying high rents in big cities. Savla added a note of caution: allowance-heavy salary structures will need to be reworked because non-wage components cannot exceed 50% of total pay.

PF–NPS balancing act

There’s also a tax cap you need to keep in mind. Employer contributions to PF and NPS together cannot exceed Rs 7.5 lakh a year.

Krishnamoorthy explained this simply:

You hit the limit for PF-only contributions at a basic salary of Rs 62.5 lakh,

And for NPS-only contributions at Rs 53.57 lakh.

He suggests balancing contributions between PF and NPS based on your tax-saving needs and return expectations.

What employees should prepare for

The transition won’t be just theoretical — companies need to overhaul payroll software, restructure salary packages and communicate clearly with employeesm experts said. Krishnamoorthy said this overhaul will lead to cleaner, more predictable salary structures. Savla, however, warned that a lack of clear communication might leave employees frustrated, especially if their take-home pay falls suddenly.

The changes extend beyond full-time staff — contract and gig workers will also see revisions as 29 existing labour laws merge into four broad codes covering wages, industrial relations, social security and workplace safety.

As the 2025 rollout gathers pace, both experts say the reforms should be viewed as a long-term investment in employee well-being. Yes, the short-term adjustment may feel uncomfortable, but the outcome is expected to be a stronger retirement foundation and more transparent, future-ready payroll systems.

Here’s what the new IIP series shows about FY27 factory output

Here’s what the new IIP series shows about FY27 factory output Here’s how vaccine alliance Gavi committed to speed Ebola vaccine

Here’s how vaccine alliance Gavi committed to speed Ebola vaccine Vodafone Idea: After 32% in a month, is the stock headed for more upside in June?

Vodafone Idea: After 32% in a month, is the stock headed for more upside in June? Annamalai was offered Rajya Sabha seat, declined; likely to quit BJP: Report

Annamalai was offered Rajya Sabha seat, declined; likely to quit BJP: Report Zee secures FIFA World Cup rights for India, just 10 days before the tournament kicks off

Zee secures FIFA World Cup rights for India, just 10 days before the tournament kicks off Piyush Goyal: Most India-U.S. Trade Issues Already Resolved

Piyush Goyal: Most India-U.S. Trade Issues Already Resolved India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review

India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review "Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs

"Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices?

Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices? India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest Pace

India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest Pace NHPC OFS opens June 2 as govt sets ₹71 floor price for up to 6% stake sale

NHPC OFS opens June 2 as govt sets ₹71 floor price for up to 6% stake sale  NMDC Steel shares jump 14% on Q4 profit revival; more steam left in the stock?

NMDC Steel shares jump 14% on Q4 profit revival; more steam left in the stock? Zee Entertainment shares jump 16% in five sessions; key triggers, target price

Zee Entertainment shares jump 16% in five sessions; key triggers, target price Prestige Estates: Multibagger realty stock rises 24% from 52-week low; buy, sell or hold?

Prestige Estates: Multibagger realty stock rises 24% from 52-week low; buy, sell or hold? Why Sensex, Nifty plunged for fourth straight session today; what investors should watch next

Why Sensex, Nifty plunged for fourth straight session today; what investors should watch next