Budget 2025 further widened the appeal of the new tax regime by making income up to Rs 12 lakh tax-free from FY 2025–26, which was applicable on senior citizens too.

Budget 2025 further widened the appeal of the new tax regime by making income up to Rs 12 lakh tax-free from FY 2025–26, which was applicable on senior citizens too.The Senior Citizens Savings Scheme (SCSS) continues to be one of the most popular fixed-income options for elderly investors in India, offering a combination of assured returns, sovereign backing and tax benefits. However, after the tax changes announced in recent Budgets, especially the expansion of the new tax regime in 2025, the actual tax outgo on SCSS investments now depends heavily on which regime a senior citizen chooses.

The Union Budget 2025, presented by Finance Minister Nirmala Sitharaman, introduced a revamped new tax regime for FY 2025-26 (AY 2026-27), effective April 1, 2025. Key changes include making income up to Rs 12 lakh completely tax-free via rebates, extending to Rs 12.75 lakh for salaried individuals (including a Rs 75,000 standard deduction).

New Tax Regime Slabs (FY 2025-26 / AY 2026-27)

Up to Rs 4 lakh: Nil

Rs 4 lakh - Rs 8 lakh: 5%

Rs 8 lakh - Rs 12 lakh: 10%

Rs 12 lakh - Rs 16 lakh: 15%

Rs 16 lakh - Rs 20 lakh: 20%

Rs 20 lakh - Rs 24 lakh: 25%

Above Rs 24 lakh: 30%

SCSS is a government-backed savings scheme available through post offices and authorised banks. Resident individuals aged 60 years and above can invest a lump sum—either singly or jointly with a spouse—for a five-year tenure, extendable by three years. Retired civilians aged 55–60 years and retired defence personnel aged 50–60 years can also open an account within one month of receiving retirement benefits. Non-resident Indians and Hindu Undivided Families are not eligible.

For Q4 FY 2025–26, the SCSS interest rate stands at 8.2% per annum. The rate is reviewed quarterly, and interest is paid every quarter on the first working day. While the scheme allows investments from as little as Rs 1,000, the maximum permissible investment is Rs 30 lakh, in multiples of Rs 1,000.

Old vs new tax regime

Tax treatment of SCSS differs sharply between the old and new tax regimes. Under the old tax regime, the principal amount invested in SCSS qualifies for deduction under Section 80C of the Income-tax Act, subject to the overall ceiling of Rs 1.5 lakh per financial year. This means that even if a senior citizen invests several lakhs—or the full Rs 30 lakh—the maximum deduction that can be claimed in a year remains capped at Rs 1.5 lakh, provided the limit has not already been exhausted through other 80C instruments such as PPF or life insurance.

Under the new tax regime, however, SCSS investments do not qualify for any deductions under Section 80C. Senior citizens opting for the new regime therefore lose this upfront tax benefit.

Budget 2025 further widened the appeal of the new tax regime by making income up to Rs 12 lakh tax-free from FY 2025–26. As a result, many senior citizens with modest incomes, including interest income from SCSS, are paying zero tax if their total income is within this threshold. At the same time, the new regime does not allow the Section 80TTB deduction of up to Rs 50,000 on interest income for senior citizens.

Tax on interest income

Interest earned from SCSS is fully taxable at the applicable slab rate in the hands of the investor. Under the old regime, senior citizens can claim a deduction of up to Rs 50,000 per year under Section 80TTB on interest income from bank deposits and post office schemes, including SCSS. Any interest above this limit becomes taxable.

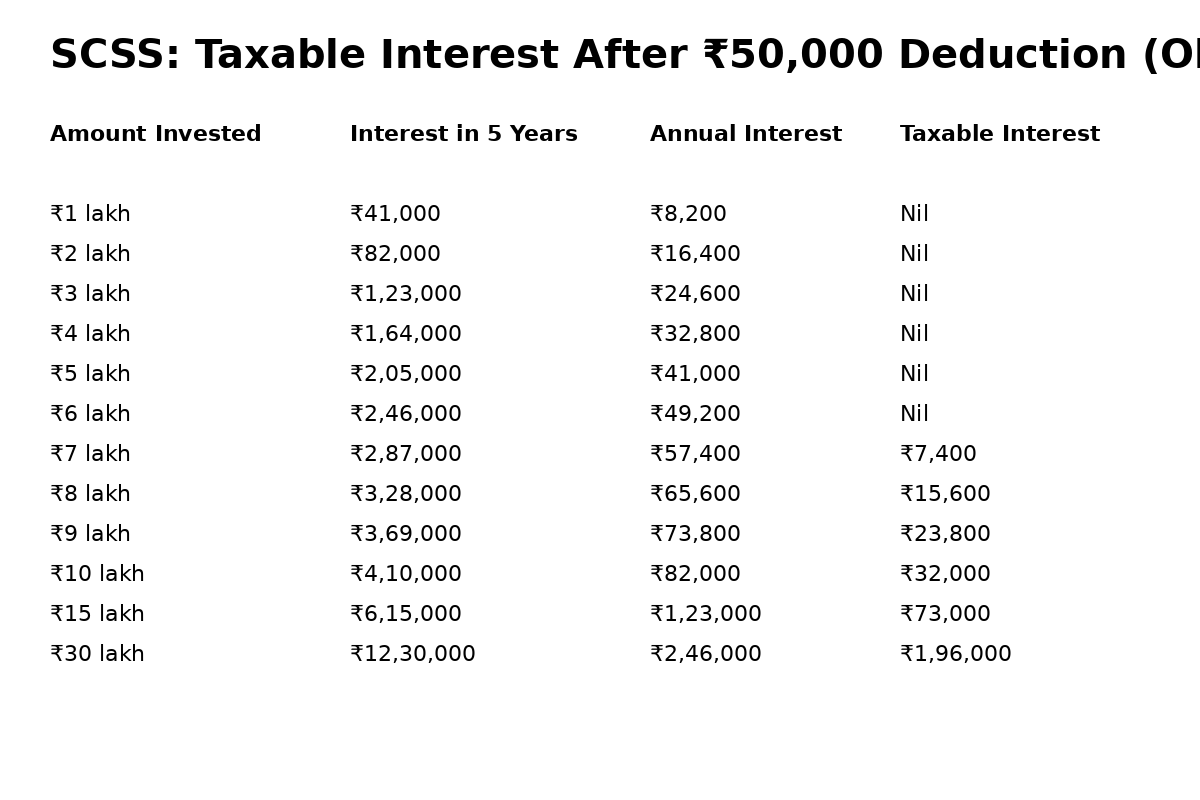

For example, a senior citizen investing Rs 10 lakh in SCSS at 8.2% earns Rs 82,000 annually. Under the old regime, ₹50,000 can be claimed as a deduction under Section 80TTB, leaving Rs 32,000 as taxable interest income. Over the five-year tenure, the total interest earned would amount to about Rs 4.1 lakh.

The tax impact becomes more visible at higher investment levels. At an investment of Rs 7 lakh, annual interest of Rs 57,400 exceeds the RS 50,000 deduction limit, making Rs 7,400 taxable. At Rs 30 lakh, annual interest works out to about Rs 2.46 lakh, of which Rs 1.96 lakh becomes taxable even after claiming the Section 80TTB deduction under the old regime.

Tax deducted at source (TDS) also applies. For senior citizens, banks and post offices deduct TDS if total interest from SCSS exceeds Rs 1 lakh in a financial year. Investors can submit Form 15H to avoid TDS if their total tax liability is nil.

For senior citizens in India (60-79 years) under the old tax regime, the basic income exemption limit is Rs 3 Lakhs, while super senior citizens (80+ years) have a Rs 5 Lakh limit, offering higher basic thresholds than the standard Rs 2.5 Lakh for younger individuals, with additional benefits like higher deductions (e.g., Section 80D for health) and the option to opt-out of advance tax if they have no business income.

The bottom line

After Budget 2025, SCSS remained attractive for safety and steady income, but its tax efficiency is dependent on individual income levels and the choice of tax regime. For seniors with income below Rs 12 lakh, the new tax regime may eliminate tax altogether, even without deductions. For others, especially those relying heavily on interest income, the old regime -- with Section 80C and 80TTB benefits -- may still result in a lower tax bill.

Did Cockroach Janta Party's 'Chalo Sansad' 2.0 threat trigger Dharmendra Pradhan's resignation? What we know so far

Did Cockroach Janta Party's 'Chalo Sansad' 2.0 threat trigger Dharmendra Pradhan's resignation? What we know so far 'Will discharge my responsibilities with complete humility': Pralhad Joshi after being appointed Education Minister

'Will discharge my responsibilities with complete humility': Pralhad Joshi after being appointed Education Minister From NEET protests to politics? What CJP's Saurav Das and Ashutosh Ranka have now revealed

From NEET protests to politics? What CJP's Saurav Das and Ashutosh Ranka have now revealed From a BA graduate to a five-time MP and Cabinet veteran: What did new Education Minister Pralhad Joshi study?

From a BA graduate to a five-time MP and Cabinet veteran: What did new Education Minister Pralhad Joshi study? From Friday pubbing to running clubs: Why Gen Z is making a surprising lifestyle switch in this country?

From Friday pubbing to running clubs: Why Gen Z is making a surprising lifestyle switch in this country? Is Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth Ahead

Is Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth Ahead Treasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment Options

Treasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment Options FDs vs Markets: Where Should You Keep Your Short-Term Money?

FDs vs Markets: Where Should You Keep Your Short-Term Money? Why Term Insurance Is Essential for Every Earning Member | Sum Assured & Coverage Explained

Why Term Insurance Is Essential for Every Earning Member | Sum Assured & Coverage Explained Pakistan's Alleged Terror-Politics Nexus: Lashkar Links Spark Questions Over Fazlur Rehman

Pakistan's Alleged Terror-Politics Nexus: Lashkar Links Spark Questions Over Fazlur Rehman Metal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picks

Metal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picks TRIL shares: Should you average the falling stock? Here's 'fixed and final' stop loss

TRIL shares: Should you average the falling stock? Here's 'fixed and final' stop loss Adani Power: 45 GW target, Rs 2 lakh crore capex plan among conference call highlights

Adani Power: 45 GW target, Rs 2 lakh crore capex plan among conference call highlights  ITC Hotels, Chalet, Ventive, IHCL, SAMHI: Hotel stocks to buy despite travel disruptions

ITC Hotels, Chalet, Ventive, IHCL, SAMHI: Hotel stocks to buy despite travel disruptions ITC shares: Rs 307 a key short-term level to watch; here's target priceMetal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picksIs Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth AheadTreasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment OptionsFrom Friday pubbing to running clubs: Why Gen Z is making a surprising lifestyle switch in this country?

ITC shares: Rs 307 a key short-term level to watch; here's target priceMetal recycling stocks to buy: Gravita, Pondy Oxides, Jain Resource among top picksIs Indo-MIM's IPO Valuation Justified? Here's Why The Company Sees Strong Growth AheadTreasury Bills Explained: Why T-Bills Are One Of The Safest Short-Term Investment OptionsFrom Friday pubbing to running clubs: Why Gen Z is making a surprising lifestyle switch in this country? Vaishno Devi pilgrims get 4 new train services including 3 Vande Bharat Express — New Delhi, Jammu, Amritsar routes covered

Vaishno Devi pilgrims get 4 new train services including 3 Vande Bharat Express — New Delhi, Jammu, Amritsar routes covered