The ₹25 lakh exemption cap significantly reduces tax burden at retirement, especially for long-tenured employees.The ₹25 lakh exemption cap significantly reduces tax burden at retirement, especially for long-tenured employees.

The ₹25 lakh exemption cap significantly reduces tax burden at retirement, especially for long-tenured employees.The ₹25 lakh exemption cap significantly reduces tax burden at retirement, especially for long-tenured employees.Tax rules 2026: Leave encashment is the amount paid by an employer for unused earned leave accumulated by an employee. Under Section 10(10AA) of the Income Tax Act, this benefit can be partially or fully tax-exempt, depending on the type of employment and timing of receipt. A key update is that for non-government employees, the maximum exemption limit is ₹25 lakh, significantly enhancing tax relief at retirement or resignation.

Who gets full exemption?

Government employees (central/state): Leave encashment received at the time of retirement or resignation is fully tax-free, with no upper limit.

On death of an employee: Any leave encashment received by legal heirs is completely exempt from tax.

What about private sector employees

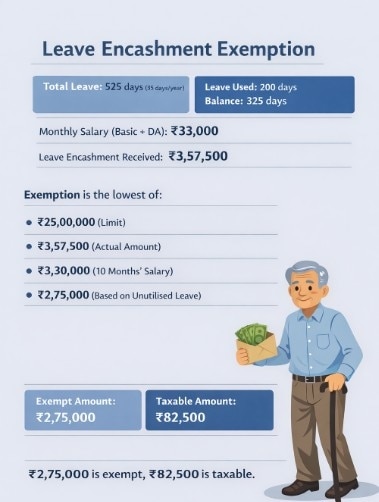

For non-government employees, the exemption is not fully automatic. The tax-free portion is the least of the following four amounts:

Actual leave encashment received

Any amount exceeding the lowest of these four components is treated as taxable income under “Salary.”

ALSO READ: Income tax 2026: Rule 9 puts NRI India-linked income under sharper lens

What counts as ‘salary’?

For calculation purposes, salary includes:

Other components like HRA, bonuses, or allowances are typically excluded.

Taxability based on timing

The taxation of leave encashment depends on when it is received:

During employment

Any leave encashment received while in service is fully taxable as “Income from Salary.” However, employees can claim relief under Section 89 to reduce the tax burden arising from lump-sum receipts. To avail this, filing Form 10E on the income tax portal is mandatory.

At retirement or resignation:

Tax treatment varies by employee category:

Government employees: Fully tax-exempt

Private sector employees: Partly exempt, partly taxable

Legal heirs (in case of death): Fully tax-exempt

ALSO READ: Can't have HRA in salary? No problem: Top tax hacks under New Tax Regime for FY27 explained

How exemption is calculated (Private employees)

For non-government employees, the exemption is the least of the following four amounts:

Actual leave encashment received

₹25,00,000 (lifetime limit notified by the government)

Average salary of last 10 months (basic + DA + eligible commission)

Cash equivalent of unutilised leave (max 30 days per year of service)

The taxable portion is calculated as:

Leave encashment received – Exempt amount

Importantly, the ₹25 lakh limit is a lifetime cap across all employers. For example, if ₹5 lakh exemption has already been claimed earlier, only the remaining ₹20 lakh can be used in future claims. Even if leave encashment is received from multiple employers in the same year, the overall exemption cannot exceed ₹25 lakh.

When is leave encashment taxable?

During employment: Fully taxable as salary. However, relief under Section 89 can be claimed to reduce the tax burden. Filing Form 10E is mandatory for this relief.

At retirement or resignation: Eligible for exemption under Section 10(10AA), subject to limits.

Types of leave considered for tax benefit

Not all leave types qualify for encashment benefits. Typically included:

Earned leave/privilege leave (if employer allows carry-forward)

Excluded from calculation:

Casual leave

Sick leave (in most cases)

Maternity, paternity, sabbatical, and quarantine leave

Employer policies also play a role in determining what can be encashed.

Cognizant to reduce 15,000 jobs; India to face maximum impact

Cognizant to reduce 15,000 jobs; India to face maximum impact") M&M share price target post robust Q4; upcoming SUV, EV models in focus

M&M share price target post robust Q4; upcoming SUV, EV models in focus") Samsung Electronics hits $1 trillion market valuation on AI-driven chip demand

Samsung Electronics hits $1 trillion market valuation on AI-driven chip demand Congress backs Vijay's TVK in Tamil Nadu, will AIADMK join course?

Congress backs Vijay's TVK in Tamil Nadu, will AIADMK join course?  Microsoft, Google, and xAI to give early access of next-gen AI models to US Govt

Microsoft, Google, and xAI to give early access of next-gen AI models to US Govt Bulldozer At Hogg Market: TMC Office Demolished In Kolkata Amid Post-Poll Violence Tension!

Bulldozer At Hogg Market: TMC Office Demolished In Kolkata Amid Post-Poll Violence Tension! Thalapathy Vijay’s Historic Win: The Fall Of DMK & AIADMK After 50 Years Of Dravidian Rule!

Thalapathy Vijay’s Historic Win: The Fall Of DMK & AIADMK After 50 Years Of Dravidian Rule! Amit Shah’s Bengal Blueprint: How The ‘Modern Chanakya’ Cracked India’s Toughest Political Code!

Amit Shah’s Bengal Blueprint: How The ‘Modern Chanakya’ Cracked India’s Toughest Political Code! Mutual Fund Strategy: Why You Shouldn’t Exit Underperforming Funds Too Soon

Mutual Fund Strategy: Why You Shouldn’t Exit Underperforming Funds Too Soon "Badla Nahi, Badlav!": PM Modi Hails Violence-Free Election As Bengal Enters A New Era Of Peace

"Badla Nahi, Badlav!": PM Modi Hails Violence-Free Election As Bengal Enters A New Era Of Peace Buy ITC Hotels, IHCL, Leela, Chalet, Lemon Tree, Brigade Hotel, says ICICI Sec

Buy ITC Hotels, IHCL, Leela, Chalet, Lemon Tree, Brigade Hotel, says ICICI Sec ITC shares stuck in bear grip; should you 'buy on dips'?

ITC shares stuck in bear grip; should you 'buy on dips'?  Why Quess Corp shares still a 'Buy' despite stock down 37% in a year — Target price

Why Quess Corp shares still a 'Buy' despite stock down 37% in a year — Target price Cochin Shipyard: PSU defence stock jumps 3% after Gujarat development

Cochin Shipyard: PSU defence stock jumps 3% after Gujarat development InterGlobe Aviation: Why IndiGo shares are rising today

InterGlobe Aviation: Why IndiGo shares are rising today