Taxpayers holding foreign assets or income must pick an ITR form featuring Schedule FA (Foreign Assets). ITR-1 and ITR-4 lack this essential section. Suitable forms are ITR-2 and ITR-3.Taxpayers holding foreign assets or income must pick an ITR form featuring Schedule FA (Foreign Assets). ITR-1 and ITR-4 lack this essential section. Suitable forms are ITR-2 and ITR-3.

Taxpayers holding foreign assets or income must pick an ITR form featuring Schedule FA (Foreign Assets). ITR-1 and ITR-4 lack this essential section. Suitable forms are ITR-2 and ITR-3.Taxpayers holding foreign assets or income must pick an ITR form featuring Schedule FA (Foreign Assets). ITR-1 and ITR-4 lack this essential section. Suitable forms are ITR-2 and ITR-3.The Income Tax Department urges taxpayers who omitted foreign assets (FA) or foreign income from their original ITR to file a revised return before December 31. This corrects any omissions or inaccuracies, ensuring compliance.

"If a taxpayer failed to report foreign assets or income in their original ITR, they can rectify this by filing a revised return up to December 31," the department stated.

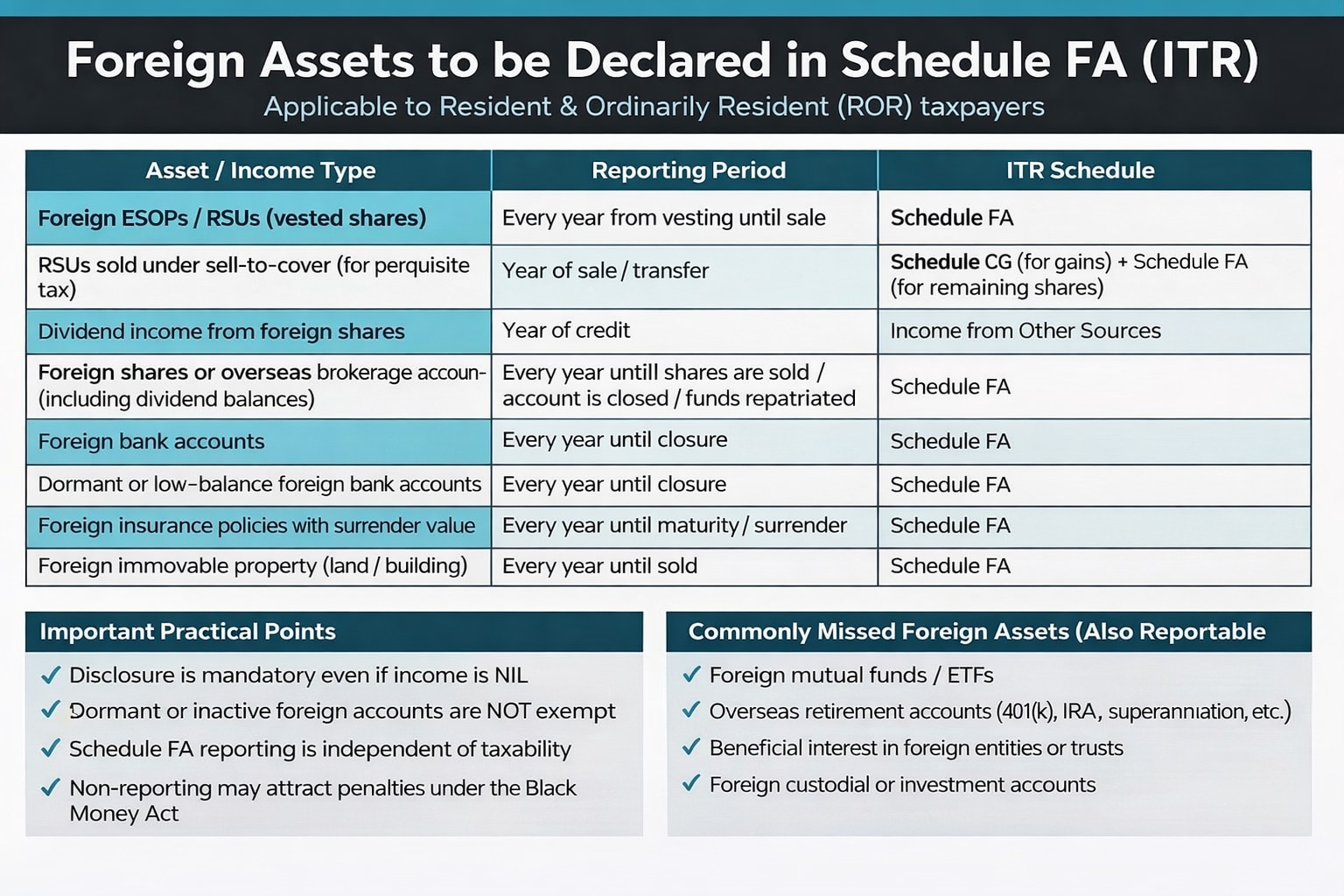

The department has reiterated the scope and importance of Schedule FA in income tax returns, outlining the foreign assets and income that Resident and Ordinarily Resident (ROR) taxpayers must mandatorily disclose. The guidance serves as a reminder that Schedule FA reporting is independent of tax liability and applies even when no income is earned from overseas assets.

In a recent tweet, CA Himank Singla shared that foreign equity holdings, such as ESOPs and RSUs must be reported in Schedule FA every year from the year of vesting until the year of sale. Where employers sell RSUs under a sell-to-cover mechanism to meet perquisite tax obligations, the transaction must be disclosed in Schedule CG for capital gains, while any remaining shares continue to be reported in Schedule FA.

Dividend income from foreign shares must be disclosed in the year of credit under “Income from Other Sources.” Foreign shares and overseas brokerage accounts, including dividend balances lying abroad, must be reported annually until the shares are sold, the account is closed, or funds are repatriated.

Foreign bank accounts, including dormant or low-balance accounts, are also required to be disclosed every year until closure. Similarly, foreign insurance policies with a surrender value and overseas immovable property such as land or buildings must be reported annually until maturity, surrender, or sale.

The tax authority has stressed several practical points. Disclosure is mandatory even if income from the asset is nil, and low-balance or inactive accounts do not qualify for exemption. Importantly, failure to report foreign assets may attract penalties under the Black Money (Undisclosed Foreign Income and Assets) Act, irrespective of whether tax is payable.

The guidance also flags commonly missed assets that remain reportable, including foreign mutual funds and ETFs, overseas retirement accounts such as 401(k), IRA or superannuation funds, beneficial interests in foreign trusts or entities, and foreign custodial or investment accounts.

Tax experts advise that taxpayers with overseas financial exposure carefully review their filings before submission, as Schedule FA compliance depends on residential status and asset ownership rather than income generation. With increased data sharing and global financial transparency, accurate disclosure has become a critical part of tax compliance for Indian residents.

Selecting ITR forms

Taxpayers holding foreign assets or income must pick an ITR form featuring Schedule FA (Foreign Assets). ITR-1 and ITR-4 lack this essential section.

The tax department said: “The two simplest Income Tax return forms—ITR-1 and ITR-4—do not contain the required Schedule FA section. Important: Taxpayers with any foreign assets or income should not file using ITR-1 or ITR-4, as these forms lack the necessary reporting schedules for foreign disclosures.”

Under the Income Tax Act, residents are obligated to report:

Foreign Assets: Via Schedule FA.

Foreign Income: Via Schedule FSI.

Tax Relief: Claim credits for overseas taxes paid using Schedule TR + online Form 67.

Select a suitable form like ITR-2, ITR-3, or others to stay fully compliant.

What counts as foreign assets or income?

Foreign assets include any holdings outside India, such as:

Immovable property

Bank accounts

Investments

Other financial assets

Foreign income covers earnings from sources abroad. Salaried individuals receiving shares, restricted stock units (RSUs), bonus shares, or ESOPs from multinational employers must report these, as they are taxable in India.

EPFO new rules 2026: Mandatory PF capped at ₹1,800; extra savings now voluntary

EPFO new rules 2026: Mandatory PF capped at ₹1,800; extra savings now voluntary WhatsApp Usernames faces India scrutiny: Govt halts roll out, gives Meta 3 days to explain

WhatsApp Usernames faces India scrutiny: Govt halts roll out, gives Meta 3 days to explain Elon Musk's next big bet? SpaceX may have a prototype for phone-like AI device

Elon Musk's next big bet? SpaceX may have a prototype for phone-like AI device Bengaluru daycare horror: Capgemini shuts facility, says employees' welfare 'foremost priority'

Bengaluru daycare horror: Capgemini shuts facility, says employees' welfare 'foremost priority' 'Stock market's going up, everybody's profiting': Donald Trump defends $1.2 billion crypto earnings

'Stock market's going up, everybody's profiting': Donald Trump defends $1.2 billion crypto earnings India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump

India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks

Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt!

TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt! Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities

Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed!

Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed! Rhi Magnesita India shares zoom over 14%; company undergoes leadership rejig

Rhi Magnesita India shares zoom over 14%; company undergoes leadership rejig Suzlon Energy: Technicals signal bullish momentum, analysts share price targets

Suzlon Energy: Technicals signal bullish momentum, analysts share price targets BPCL, HPCL, IOC shares gain up to 4% amid oil price fall, Nayara petrol, diesel rate cuts

BPCL, HPCL, IOC shares gain up to 4% amid oil price fall, Nayara petrol, diesel rate cuts Tata Technologies shares snap five-session fall, climb nearly 8% today; here's why

Tata Technologies shares snap five-session fall, climb nearly 8% today; here's why Adani Total Gas, Auro Pharma, Delhivery: stocks to trade - Target price, stop loss & more

Adani Total Gas, Auro Pharma, Delhivery: stocks to trade - Target price, stop loss & more