Omitting F&O gains or losses in your ITR could lead to a notice from the Income Tax Department.Omitting F&O gains or losses in your ITR could lead to a notice from the Income Tax Department.

Omitting F&O gains or losses in your ITR could lead to a notice from the Income Tax Department.Omitting F&O gains or losses in your ITR could lead to a notice from the Income Tax Department.Futures and Options (F&O) trading in India offers immense opportunities for traders. The Income Tax Act classifies F&O income as Non-Speculative Business Income and requires it to be mandatorily reported in the Income Tax Returns (ITR).

As per Section 43(5) of the Income Tax Act, 1961, F&O income or loss is treated as non-speculative business income and must be declared under the head "Profits and Gains of Business or Profession" (PGBP). This income is taxed at the slab rates applicable to the individual. This differs significantly from capital gains tax rules that apply to equity investments or speculative business rules that apply to intraday equity trades.

The distinction matters because non-speculative business income allows for broader and more flexible loss set-off and carry-forward provisions under Sections 70, 71, and 72 of the Act. Speculative losses, on the other hand, can only be set off against speculative gains and have more restrictive carry-forward rules.

A total of 95.75 lakh individuals traded in futures and options (F&O) derivatives in FY24, according to a report by market regulator SEBI. However, 91.1% of them incurred losses on a net basis — highlighting the importance of understanding tax treatment not just on profits, but also on losses.

A real-life case highlighted by Sujit Bangar, founder of TaxBuddy.com and a former IRS officer, sheds light on the significance of proper tax strategy in such cases.

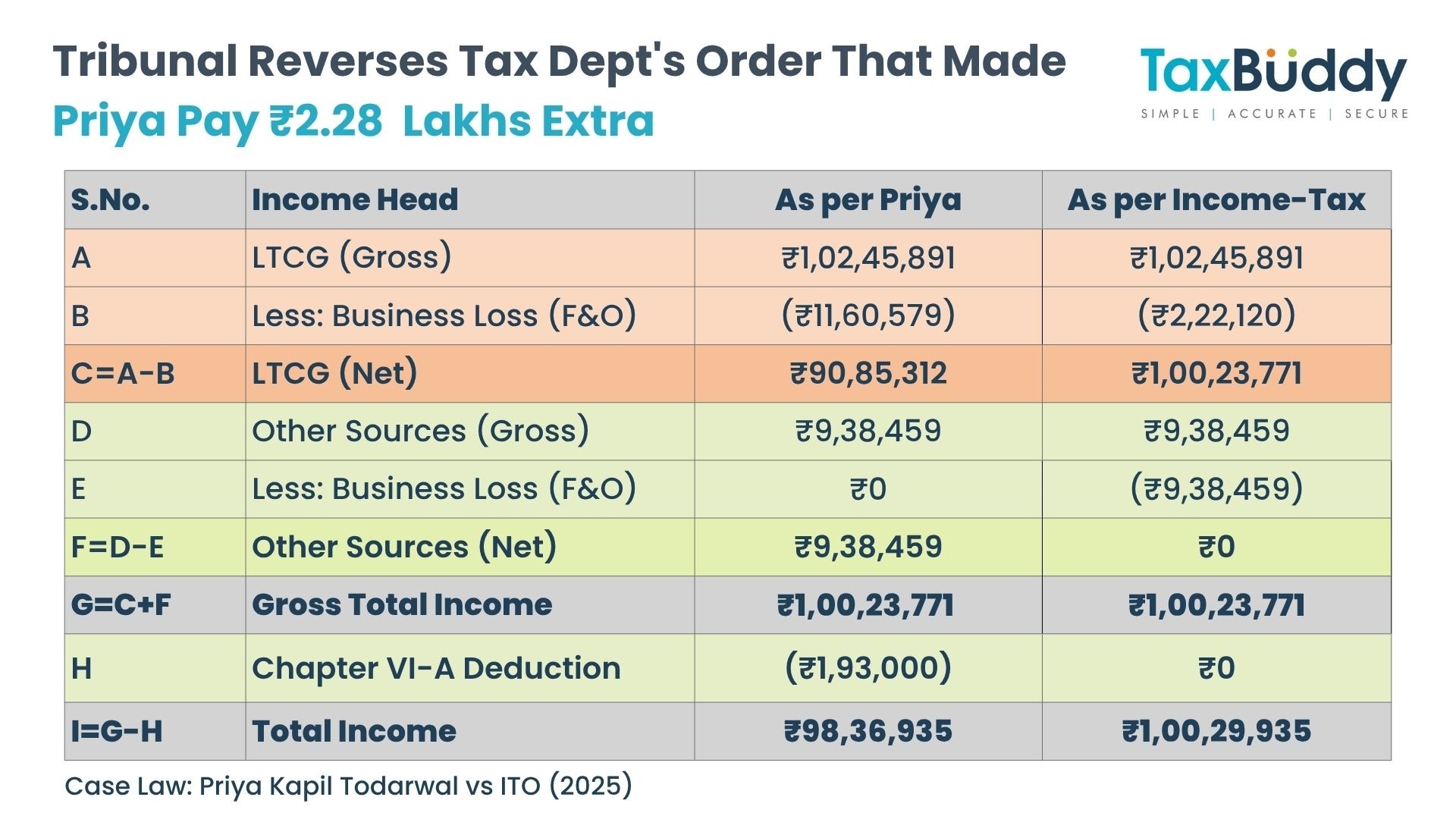

Take Priya’s case:

She reported the following income in a given financial year:

Business Loss (F&O): ₹11.6 lakh

Long-Term Capital Gains (LTCG): ₹1.02 crore

Interest Income: ₹9.38 lakh

Deductions claimed under Chapter VI-A: ₹1.93 lakh

Priya set off her F&O loss against LTCG, preserving her interest income from the “Income from Other Sources” head. This move allowed her gross total income (GTI) to include non-capital gains income — a prerequisite for claiming deductions under Chapter VI-A (like 80C, 80D etc.).

However, the Centralised Processing Centre (CPC) disallowed her ₹1.93 lakh deduction. Their reason? Her gross total income consisted only of capital gains, which is ineligible for such deductions.

But the Income Tax Appellate Tribunal (ITAT) ruled in her favour. Key observations:

Section 71(2) permits business losses to be set off against any other head of income, including capital gains.

The law does not mandate a specific sequence for setting off losses.

As her “Other Sources” income remained untouched, her GTI validly included income eligible for Chapter VI-A deductions.

The ₹1.93 lakh deduction was therefore allowed, and the ₹2.28 lakh demand raised by CPC (tax + penalty + interest) was quashed.

This judgment sets a precedent for how sequence of set-off can influence deduction eligibility and overall tax liability.

Understanding intra-head set-off for F&O losses

Intra-head set-off means adjusting losses against gains from other sources within the same income head. Since F&O income is business income, a trader can offset F&O losses against profits from any other business activity in the same year under PGBP. This is allowed under Section 70 of the IT Act.

For instance, if an F&O loss of ₹1 lakh is matched with ₹1.5 lakh profit from a small business, the net taxable income becomes ₹50,000 under PGBP.

This helps traders avoid unnecessary tax outgo in years of mixed performance across ventures.

Conclusion

With most F&O traders booking losses, knowing how to report, set off, and sequence income can make a significant difference. Proper application of the Income Tax Act provisions can reduce your taxable income, preserve deductions, and avoid litigation — turning an otherwise painful loss into strategic tax planning.

Centre to launch new series WPI, producer price indices on June 15

Centre to launch new series WPI, producer price indices on June 15 Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR

Mother Dairy expects 5% growth in FY27; eyes expansion beyond Delhi-NCR, Wipro and Tech Mahindra have seen renewed buying interest.") IT stocks stage a comeback: Five factors supporting the strong upmove

IT stocks stage a comeback: Five factors supporting the strong upmove ‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’

‘This is an incredible time to be a…’: Nvidia CEO Jensen Huang said on ‘SaaSpocalypse’ From Global Uncertainty To India's Opportunity: The Big Economic Outlook

From Global Uncertainty To India's Opportunity: The Big Economic Outlook Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services

Godrej Industries Is Entering The Wealth Management Space As It Looks To Scale Up Financial Services SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early?

SIP Vs SWP: The Two-Step Mutual Fund Strategy That Could Help Become A Millionaire & Retire Early? Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom

Retired At 39! How Sanjay Kathuria Turned A ₹2,000 SIP Into Complete Financial Freedom Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation

Tata Tech, Bharti Airtel, PFC, BLS International shares: Should you enter at current levels?Oyo parent Prism gets Sebi nod for ₹6,650-cr IPO; eyes $7-8 bn valuation Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove

Rs 75/share dividend by Tata Group stock – Record date next week IT stocks stage a comeback: Five factors supporting the strong upmove CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?

CMR Green Technologies IPO: GMP zooms 130% in a week; should you subscribe?