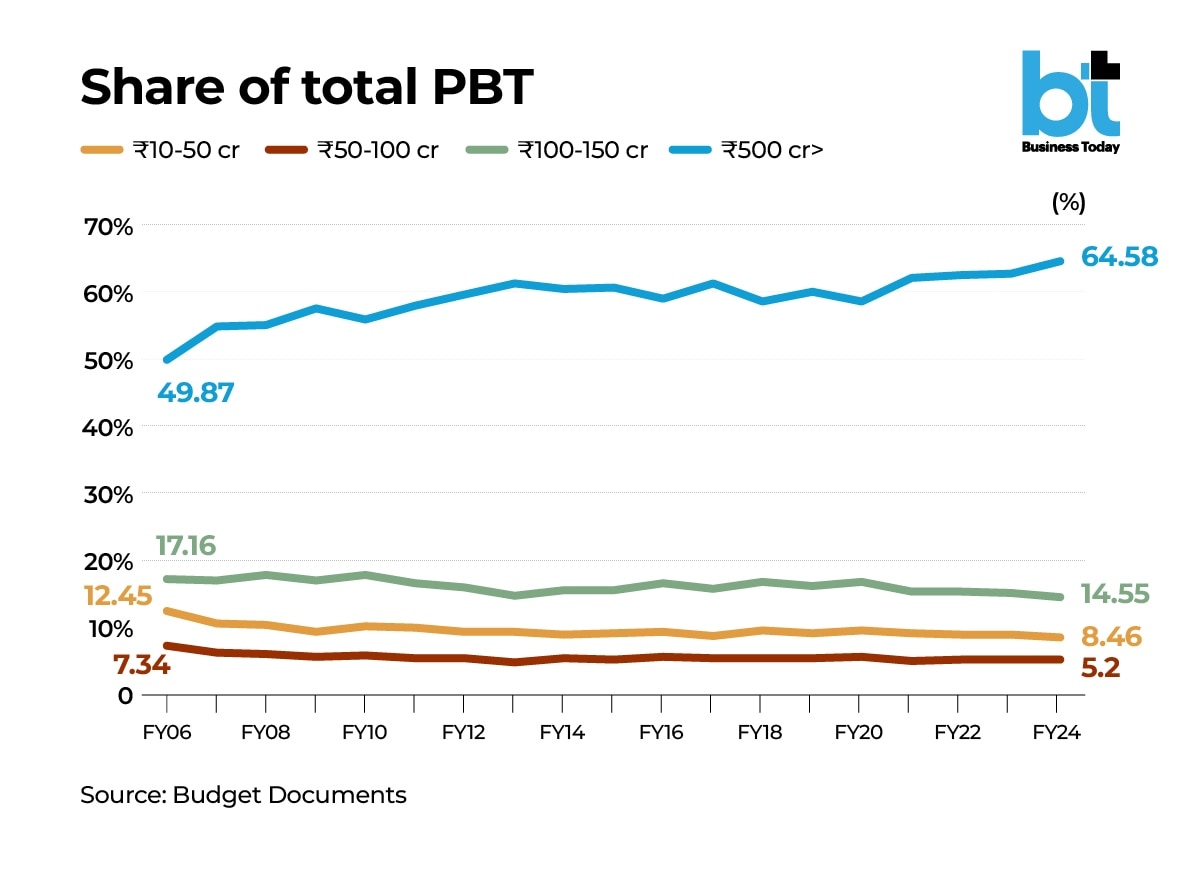

To be sure, the share of companies with PBT above Rs 500 crore has exceeded 60% of total PBT every year since FY21, hitting fresh all-time highs each year. It increased from 62.08% in FY21 to 62.54% in FY22, 62.59% in FY23, and 64.58% in FY24, according to Budget documents.

Budget documents over the years show that the share of such companies was less than 50% in FY06, rising above the halfway mark in the years that followed, with occasional dips, though it never declined below 50% after that year.

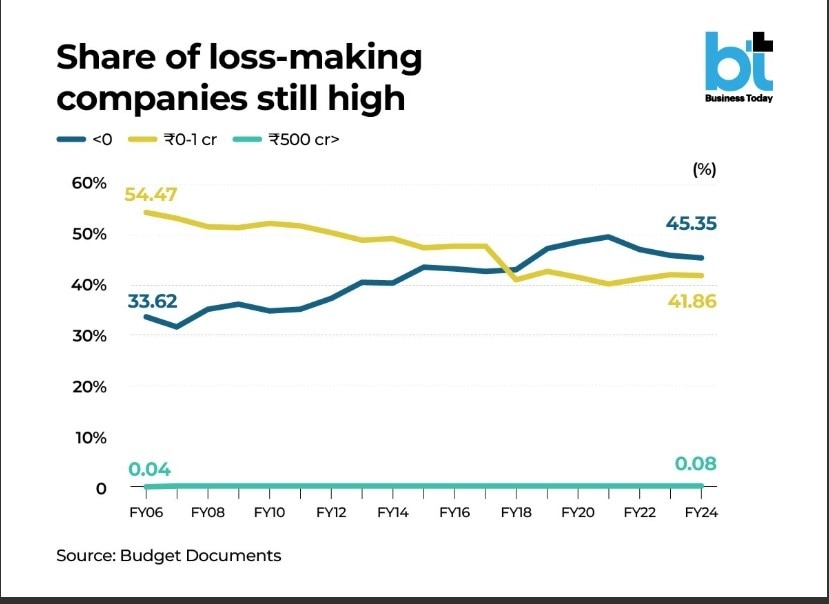

The data also show that the share of companies that reported losses rose from 33.6% in FY06 to more than 40% in FY13 and increased to 47% in FY19, rising to an all-time high of 49.6% in FY21, which was marred by the outbreak of Covid-19 and the lockdowns announced to slow the pandemic’s spread. The share of loss-making companies has dipped since then, reducing to 45.35% in FY24.

In fact, the increase in the share of loss-making companies is commensurate with a fall in the proportion of companies that reported profits up to Rs 1 crore. The share of the latter fell from 54.47% in FY06 to 48.91% in FY13, the first time it dipped below the halfway mark. The category witnessed a steep fall in FY18, when it fell to 41.04% from 47.67% the previous year, and hit an all-time low of 40.15% in Covid-hit FY21. It has recovered slightly since then but was still at 41.86% in FY24.

Overall, the share of firms that reported profits before tax has not breached the 50% mark since FY18, when it first dipped below that mark. It has improved from the all-time low of 46% in FY21, rising to just under 50% in FY24, though the share of loss-making companies and those that reported zero profits was still above 50%.

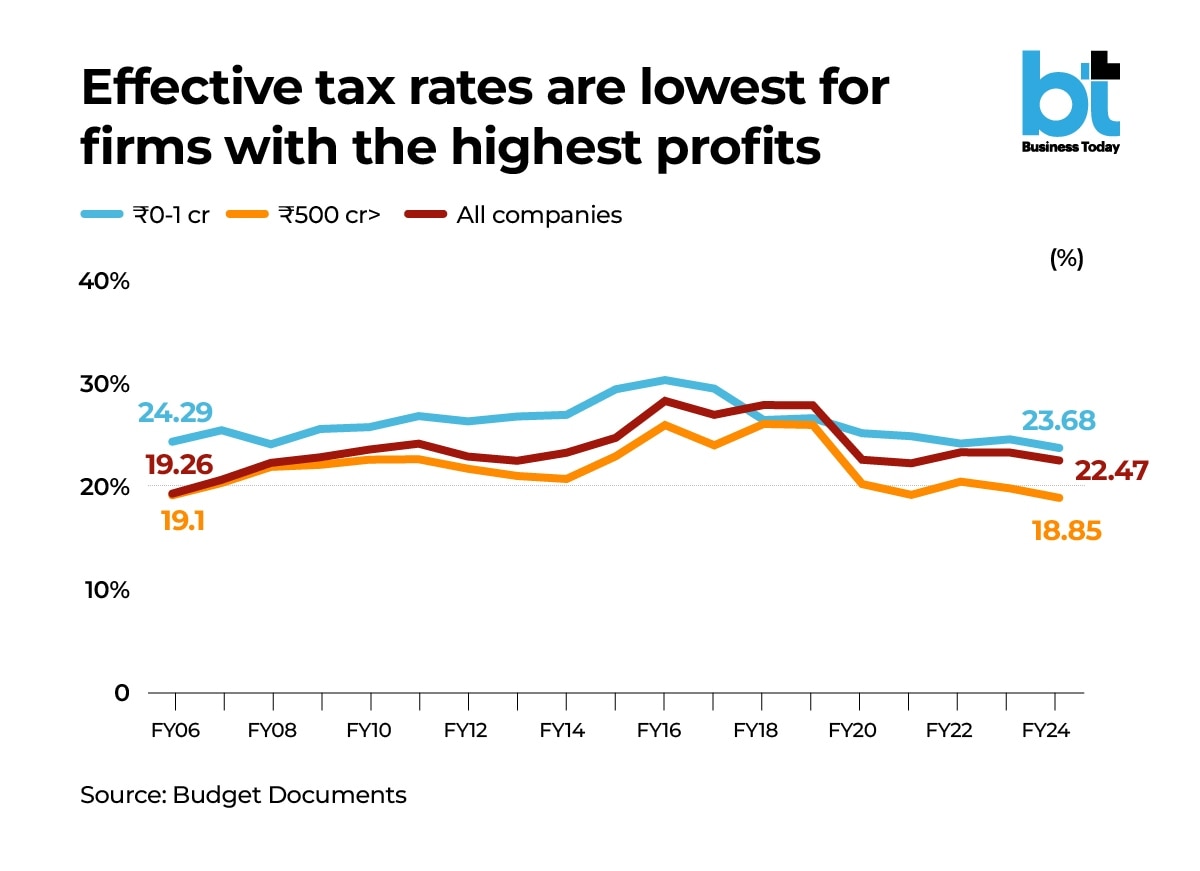

Significantly, Companies that made the most profit paid less tax than companies that made the least profit. For instance, in FY24, the effective tax rate for the companies that reported PBT above Rs 500 crore was 18.85%, which was lower than the overall rate of 22.47%, and much below the 23.68% that companies that reported PBT up to Rs 1 crore paid.

The document says the effective tax rate “is the ratio of total taxes (including surcharge and cess) to the total profits before taxes (PBT) and expressed as a percentage”.

Explaining the data, the Budget document says the statutory tax rate, including cess, for companies with income up to Rs 1 crore was 31.20% (33.38% including cess and surcharge) for companies with income up to Rs 10 crore, and 34.94% including cess and surcharge for companies with income exceeding Rs 10 crore. “Further, for existing companies which opted for the new concessional tax regime (lower tax rate without deductions and exemptions) under section 115BAA of the Income-tax Act, the statutory tax rate was 25.17%,” the document notes.

The overall effective tax rate fell sharply from 27.81% in FY19 to 22.54% in FY20 and has hovered around that rate since. However, this is still higher than the overall effective tax rate of 19.26% in FY06. The all-time high was recorded in FY16, when it was 28.24%.

The category that saw the biggest decline in effective tax rates in those years was companies with PBT above Rs 500. The rate for the category dropped from 27.81% in FY19 to 19.14% in FY20 to an all-time low of 18.85% in FY24. The previous low for the category was 19.1%. For companies that reported up to Rs 1 crore of PBT, though the effective tax rate has dipped in recent years, it was still higher than that for the companies with the highest PBT.

Speaking about the health of India Inc, Surajit Mazumdar, Professor at the Centre for Economic Studies and Planning, Jawaharlal Nehru University, says it depends on how one defines India Inc. “If by India Inc we mean the biggest companies, then they are clearly doing well. But if you look at it as a whole, then there are signs of distress,” he says.

Mazumdar says the Indian economy is witnessing a double concentration. The concentration of income in the hands of the rich and the concentration of profits among very few companies. These are also the companies that have very low effective tax rates, he highlights. And these are also the companies in which investment is heavily concentrated. “Measures to boost ease of doing business are not creating the conditions for a broad-based flowering of entrepreneurship,” Mazumdar says.

The data shows two distinct phases of distress, he adds. The first one began in FY13 because of the delayed impact of the global financial crisis, and the second one began in FY19 because of the impact of demonetisation and the passing of the goods and services tax (GST), that appear to have impacted smaller firms. This was compounded by the Covid-19 pandemic and does not appear to have reversed.

Speaking about the recent measures announced to boost consumption demand, like the cut in income tax rates in Budget 2025-26 and the subsequent rationalisation of the GST rates, Mazumdar says the problem was the persistently low wages in the country, which means a large proportion of the population is unable to increase its spending beyond essentials.

“Private sector investment is not increasing because sectors that can absorb large amounts of investment are not offering good returns. In manufacturing, there is a demand constraint because of inequalities in the economy,” he says.

He adds that in such a situation, the alternative is exports. “But even there, the way we are incorporated in the global value chains is such that what we produce is heavily dependent on imports.”

Considering the external environment, Mazumdar says the government should have used the Budget to increase expenditure. However, the government is constrained on that front from the cumulative impact of the cuts in corporate and income taxes and GST, he adds.

Just 877 or 0.08% of the 1.13 million companies that filed tax returns for FY24 accounted for two-thirds of India Inc’s profits before tax for that fiscal year.

Just 877 or 0.08% of the 1.13 million companies that filed tax returns for FY24 accounted for two-thirds of India Inc’s profits before tax for that fiscal year. Sajjan Jindal-led JSW Greentech enters electric bus market, rolls out first 100 buses at Dolvi plant

Sajjan Jindal-led JSW Greentech enters electric bus market, rolls out first 100 buses at Dolvi plant Why Air India is betting bigger on Canada new Mumbai-Toronto flights and new Dreamliner

Why Air India is betting bigger on Canada new Mumbai-Toronto flights and new Dreamliner Hyundai Motor India posts highest-ever monthly sales of 75,360 units in July, exports hit 100-month high

Hyundai Motor India posts highest-ever monthly sales of 75,360 units in July, exports hit 100-month high BT Explainer: Air India back with its long-haul monopoly as IndiGo ends widebody operations

BT Explainer: Air India back with its long-haul monopoly as IndiGo ends widebody operations GST collections jump 15.4% to ₹2.11 lakh crore in July, import tax revenues surge nearly 29%

GST collections jump 15.4% to ₹2.11 lakh crore in July, import tax revenues surge nearly 29% IRFC CMD Manoj Kumar Dubey Reveals Top Funding Priorities Beyond Railways & IRFC 2.0 Vision

IRFC CMD Manoj Kumar Dubey Reveals Top Funding Priorities Beyond Railways & IRFC 2.0 Vision "Mineral Security Is National Security": G Kishan Reddy On India’s Push For Aatmanirbharta

"Mineral Security Is National Security": G Kishan Reddy On India’s Push For Aatmanirbharta From Phones To Semiconductors: Why India Needs More Critical Minerals

From Phones To Semiconductors: Why India Needs More Critical Minerals Can India Power Millions Of Homes Without Generating More Electricity?

Can India Power Millions Of Homes Without Generating More Electricity? Women’s Financial Independence: Why Earning Money Is Not Enough| Priti Rathi Gupta Explains

Women’s Financial Independence: Why Earning Money Is Not Enough| Priti Rathi Gupta Explains HUL shares: Why analyst prefers Marico, Nestle to the FMCG sector leader in short term

HUL shares: Why analyst prefers Marico, Nestle to the FMCG sector leader in short term Tata Steel, Vedanta among top metal bets for a six-month view, says analyst

Tata Steel, Vedanta among top metal bets for a six-month view, says analyst Bajaj Housing Finance shares down 53% from its peak; is it time to buy?

Bajaj Housing Finance shares down 53% from its peak; is it time to buy? GMDC, IDFC First Bank: Expert shares outlook, key levels to watch

GMDC, IDFC First Bank: Expert shares outlook, key levels to watch Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36%

Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36% Your car loan is over but your checklist isn't: CA explains costly mistakes made after the last EMI

Your car loan is over but your checklist isn't: CA explains costly mistakes made after the last EMI