LTCG are calculated by subtracting transfer expenses, the cost of acquisition and the cost of improvement from the sale value of an asset.LTCG are calculated by subtracting transfer expenses, the cost of acquisition and the cost of improvement from the sale value of an asset.

LTCG are calculated by subtracting transfer expenses, the cost of acquisition and the cost of improvement from the sale value of an asset.LTCG are calculated by subtracting transfer expenses, the cost of acquisition and the cost of improvement from the sale value of an asset.Budget 2026: With the Union Budget 2026–27 around the corner, investors and tax experts are closely watching whether the government will tweak rules governing long-term capital gains (LTCG). Capital gains tax plays a crucial role in investment decisions, as it determines how profits from selling assets are taxed. India first introduced the levy in 1947, withdrew it briefly, and reintroduced it in 1956, after which it has been reshaped several times to suit evolving economic needs.

A major reset came in the Union Budget 2024, when Finance Minister Nirmala Sitharaman lowered the LTCG tax rate on property and gold from 20% to 12.5% and aligned holding periods across different asset classes.

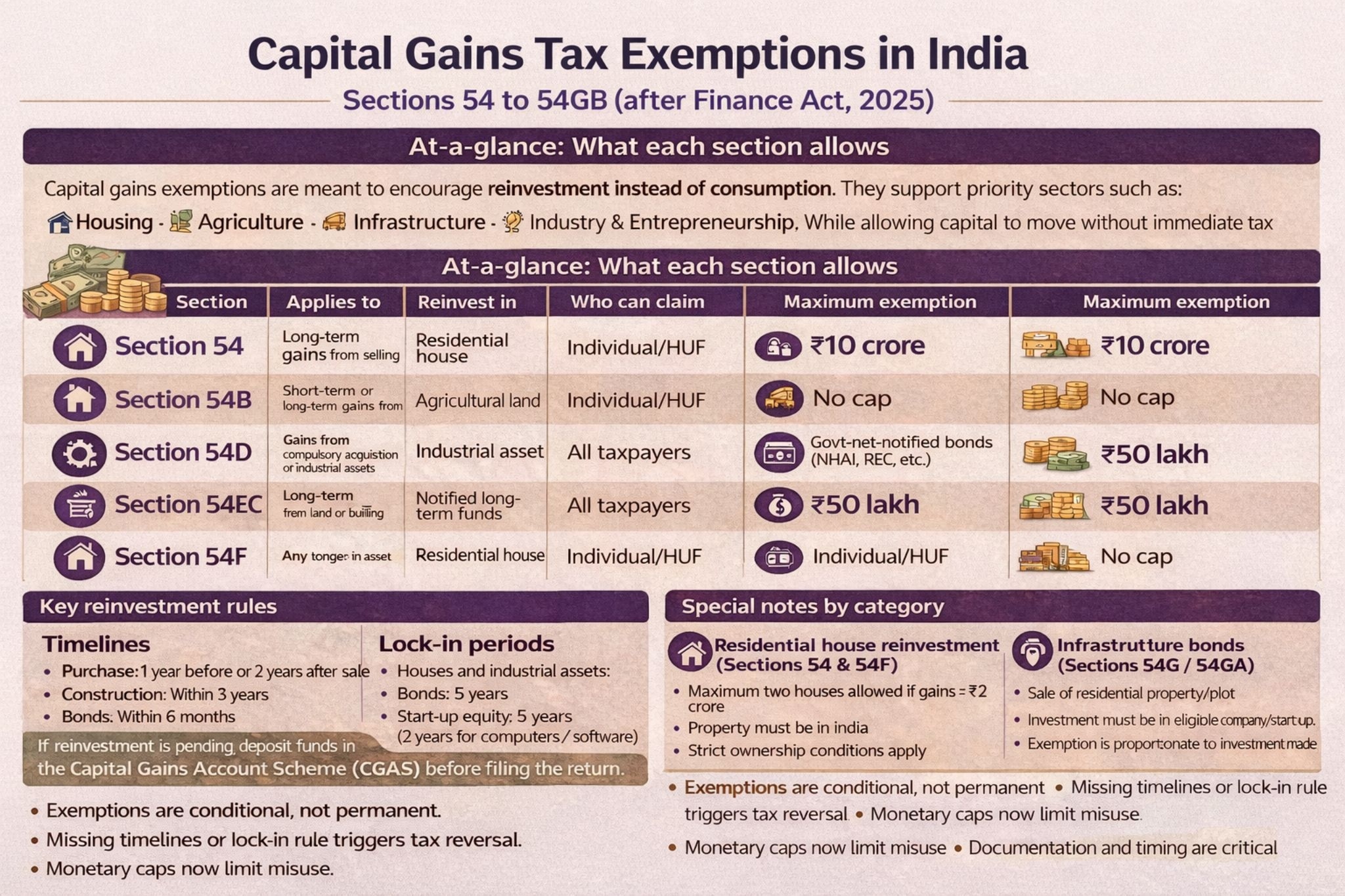

Capital gains tax exemptions under Sections 54 to 54GB of the Income-tax Act are designed to encourage reinvestment rather than consumption. The idea is simple: if you reinvest the gains from selling an asset into specified avenues, the tax on those gains can be deferred or fully exempted—provided you meet strict conditions.

Which capital gains qualify?

Rupeesh K., tax expert and family office investment advisor, explained most of these exemptions apply to long-term capital gains (LTCG), though a few also cover short-term gains in specific cases. For instance, Section 54 applies to LTCG from selling a residential house, while Section 54B covers gains from agricultural land, whether short-term or long-term. Sections such as 54F apply when any long-term asset other than a house is sold, and the proceeds are reinvested in a residential property. Sections 54G and 54GA deal with gains arising from shifting industrial undertakings, and Section 54GB applies when gains from selling residential property are invested in eligible start-ups or companies.

Where reinvestment is allowed

The law clearly defines where money must be reinvested to qualify for exemption. Broadly, reinvestment is permitted in:

Residential property (Sections 54 and 54F)

Agricultural land (Section 54B)

Government-notified bonds such as NHAI or REC bonds (Section 54EC)

Specified long-term assets including notified funds (Section 54EE)

Industrial assets when businesses relocate from urban areas (Sections 54G and 54GA)

Equity in eligible start-ups or companies that invest in new plant and machinery (Section 54GB)

Maximum limits and timelines

Exemptions come with clear caps and deadlines. Investment in bonds under Sections 54EC and 54EE is capped at Rs 50 lakh. For residential property reinvestment under Sections 54 and 54F, the exemption is capped at Rs 10 crore. Timelines are equally strict:

Purchase of property must usually be made within one year before or two years after the sale.

Construction must be completed within three years.

Bonds must be purchased within six months of the transfer.

If reinvestment is delayed, taxpayers can park funds in the Capital Gains Account Scheme (CGAS) before filing returns to preserve the exemption.

Lock-in periods and clawback risks

These benefits are conditional, not permanent. Most reinvestments carry a lock-in period of three to five years. If the new asset is sold too soon, the earlier exemption is withdrawn and the capital gain becomes taxable in the year of violation. This “clawback” rule applies to houses, bonds, industrial assets and even start-up investments.

Capital gains exemptions offer powerful tax relief, but only for disciplined investors who follow the rules to the letter. Missing timelines, exceeding limits or breaching lock-in conditions can quickly turn a tax-saving move into a costly mistake.

US and Iran halt strikes, head to Doha to save their 11-day-old peace deal from collapse

US and Iran halt strikes, head to Doha to save their 11-day-old peace deal from collapse HDFC Bank shares in focus: Legal review found no evidence backing Atanu Chakraborty's claims

HDFC Bank shares in focus: Legal review found no evidence backing Atanu Chakraborty's claims HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report

HDFC Bank likely to reappoint Sashidhar Jagdishan as CEO for a third term: Report Monsoon in India: IMD expects rains in next 5-6 days as Delhi, North India reels under intense heat

Monsoon in India: IMD expects rains in next 5-6 days as Delhi, North India reels under intense heat") This IndiGo aircraft used Gagan satellite system instead of ground radio to land; Here's how it did it

This IndiGo aircraft used Gagan satellite system instead of ground radio to land; Here's how it did it HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Indian Hotels, Max Healthcare, Bajaj Finance among top largecap picks; check targets

Indian Hotels, Max Healthcare, Bajaj Finance among top largecap picks; check targets FII selloff in H12026 exceeds 2025 outflows: Factors keeping investors on the edge

FII selloff in H12026 exceeds 2025 outflows: Factors keeping investors on the edge  Hind Zinc shares in focus amid pact with UP govt to explore Nawatola rare earths block

Hind Zinc shares in focus amid pact with UP govt to explore Nawatola rare earths block HDFC Bank, IndiGo, Inox Wind: Stocks to buy — Target prices, key levels, stop loss & moreHDFC Bank shares in focus: Legal review found no evidence backing Atanu Chakraborty's claims

HDFC Bank, IndiGo, Inox Wind: Stocks to buy — Target prices, key levels, stop loss & moreHDFC Bank shares in focus: Legal review found no evidence backing Atanu Chakraborty's claims