The fourth quarter (Q4) of FY19 might be a dampener for different sectorsThe fourth quarter (Q4) of FY19 might be a dampener for different sectors

The fourth quarter (Q4) of FY19 might be a dampener for different sectorsThe fourth quarter (Q4) of FY19 might be a dampener for different sectorsThe earnings season is all set to kick off and soon companies will start reporting their numbers for the recently concluded quarter. The estimates for the financial year 2019 (FY19) by Narnolia Financial Advisors (NFAL) point towards a double-digit topline year-on-year (y-o-y) growth of 11.8 per cent and net profit growth of 6 per cent in their coverage universe, which excludes financial companies.

In FY19, sales are expected to grow by 24 per cent, earnings before interest, tax, depreciation and amortisation (EBITDA) by 15 per cent and the bottom line numbers are expected to increase by 11 per cent. Though the overall picture looks impressive, the fourth quarter (Q4) of FY19 might be a dampener for different sectors.

The automobile and auto components sector, which had a dry run in FY19, is set to disappoint in the fourth quarter, too, along with the pharmaceutical sector. While the banking sector is expected to outperform in the net interest margin (NIM) and profit growth. Here's a look at their detailed outlook.

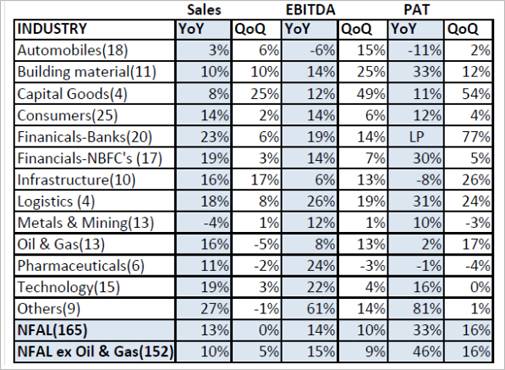

Q4FY19 growth estimates

Financials-Banks: Banks, especially, the corporate lenders are likely to report better earnings numbers during 4Q FY19 led by reversal of NPA (non-performing assets) cycle, lower provisioning, improvement in NIMs and lower credit cost. While banks contributed only 2.5 per cent to aggregate net profits of NFAL's 165 coverage companies in Q4FY18, they now will contribute 20 per cent to the total profits. The NIM is expected to witness a 23 per cent growth on a yearly basis. The growth in advances is likely to improve for most of the lenders due to pick up in large corporate loan demands and buyout of retail portfolios from NBFCs (non-banking financial companies). The infusion of capital in the public sector banks will also help in improving the credit growth.

Financials-NBFC: The cost of funds had eased during the quarter for the NBFCs but NIM would take one more quarter to show improvement. Industry-wide aggressive securitisation of the portfolio will also result in spread compression. The hikes in rates across the portfolio are expected to support the margins going ahead. The growth has become a key issue for the NBFCs industry, due to liquidity crunch and asset-liability mismatch. The slowdown in vehicle sales and problems in the real estate segment are hurting the segment. Liability raising plan will be key to watch in 4Q FY19.

Technology: The tech sector has posted a strong growth in the last few quarters due to the rise of the digital. It is expected to deliver a 19 per cent y-o-y sales growth in the revenue, while PAT (profit after tax) is estimated to increase by 16 per cent. Appreciation of rupee against the dollar is anticipated to impact the growth by 10 to 60 basis points in Q4FY19E (fourth quarter of FY19 estimate). Margins in Q4FY19E for technology sector are expected to remain under pressure for tier 1 companies as most of them will continue to invest in localisation, higher subcontracting cost and re-skilling of the employees. Even tier II companies will be no different as a sharp decline in IP due to seasonality, change in business mix and continued investment plan, will result in flat or de-growth for most of the companies.

Oil & Gas: The volumes of oil marketing companies (OMC) are expected to remain subdued due to low demand in January and February. Margins of OMCs are expected to improve sequentially led by the bounce back in the Singapore refining margin (benchmark) and better distillate yields.

Consumers: Consumer companies are expected to report slightly lower sales and volume growth considering slowing down of consumption in rural, as well as, the urban market due to tight liquidity, agrarian distress and prolonged winters. Though companies that are expanding their distribution reach will see slightly better volume growth, sales are expected to grow at 14 per cent y-o-y, while the PAT is expected to post a 12 per cent y-o-y growth.

Automobiles: Industry volume growth remained at 5 per cent y-o-y this quarter due to liquidity issue and weaker consumer sentiments led by increased ownership cost. The realisation is also expected to be flat on a sequential basis because of increased inventory levels leading to higher discounts. EBITDA margin will contract as there will be weaker operating leverage, though some of the contraction will be arrested on account of the reduction in raw material prices.

Metals & mining: In ferrous space, the realisation is expected to drop as 3QFY19 fall in steel price would come in effect in 4QFY19. The realisation for JSW Steel and JSPL are expected to fall by 7 per cent and 8 per cent respectively. In nonferrous space, the companies are expected to see margin contraction on y-o-y basis, due to lower commodity prices.

Building materials: The building materials comprising of cement, tiles and ply are expected to report 10 per cent q-o-q sales and 12 per cent q-o-q net profit growth for the quarter. Volumes are expected to grow by 6-7 per cent y-o-y. Improved realisations are expected to ease the EBITDA margins. The listed players in the tile industry will benefit from easing pricing pressure in the industry. The wood industry continues to face weak demand, higher raw material costs and over-capacities.

Infrastructure: Infrastructure companies are expected to report 16 per cent y-o-y sales growth, though net profits should remain under pressure. The un-executable order book is still higher due to muted land acquisition progress.

Capital goods: Revenue of capital goods companies is expected to increase by 13 per cent y-o-y. The government continues to drive the capex while private sector participation is still muted. PAT growth is expected to be at around 12 per cent on the back of healthy revenue growth.

Pharmaceuticals: The NFAL's pharma sphere may witness a small growth in sales in this quarter, while the PAT might witness a 1 per cent de-growth on a y-o-y basis due to the pricing pressures in the last couple of years on account of high competition. "US will report decent numbers in the coming quarters and expect India business to normalise in FY19 post-disruption in FY18 due to GST implementation," says Narnolia Financial Advisors.

Also read: Jet Airways bidding process: Etihad agrees to raise stake in airline; submits expression of interest

Also read: SpiceJet to lease 16 Boeing 737s to fill gap as groundings push up fares

") 'India Inc functions like zamindars': Navam Capital MD after Uday Kotak's wake-up call warning

'India Inc functions like zamindars': Navam Capital MD after Uday Kotak's wake-up call warning India may cut bond taxes, ease investment rules to attract foreign capital: Report

India may cut bond taxes, ease investment rules to attract foreign capital: Report Will RBI raise interest rates at upcoming MPC meet? Here’s what SBI chief says

Will RBI raise interest rates at upcoming MPC meet? Here’s what SBI chief says ₹10,000-crore support for aviation fuel: Will airfares stabilise after govt help?

₹10,000-crore support for aviation fuel: Will airfares stabilise after govt help? BT Explainer: Planning a rooftop solar system? New rule from June 1 could increase costs by this amount

BT Explainer: Planning a rooftop solar system? New rule from June 1 could increase costs by this amount Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion

Section 301 Tariffs Could Hit Indian Exports Just As Trade Deal Nears Completion Market Masters With Aniruddha Sarkar | Top Stock Ideas, Market Outlook & Investment Strategy

Market Masters With Aniruddha Sarkar | Top Stock Ideas, Market Outlook & Investment Strategy The Retirement Strategy: NPS, SWP, Mutual Funds, Insurance & Passive Income Explained

The Retirement Strategy: NPS, SWP, Mutual Funds, Insurance & Passive Income Explained What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Maruti's Flex-Fuel Car Launch: Ethanol Industry On Fuel Pricing, Mileage & Demand

Maruti's Flex-Fuel Car Launch: Ethanol Industry On Fuel Pricing, Mileage & Demand CMR Green Technologies IPO subscribed 2.46 times on Day 1; check latest GMP, other key details

CMR Green Technologies IPO subscribed 2.46 times on Day 1; check latest GMP, other key details Ola share price surged 10% amid heavy volumes; key details

Ola share price surged 10% amid heavy volumes; key details BT Closing Bell | Sensex recovers 850 pts from day's low on report of tax cut on foreign bonds

BT Closing Bell | Sensex recovers 850 pts from day's low on report of tax cut on foreign bonds IndiGo, SpiceJet, Taneja Aerospace, other aviation stocks jump up to 5%; here's why

IndiGo, SpiceJet, Taneja Aerospace, other aviation stocks jump up to 5%; here's why Reliance Jio IPO in focus ahead of AGM: What YES Securities said on valuations, growth & more

Reliance Jio IPO in focus ahead of AGM: What YES Securities said on valuations, growth & more