Choice Broking said BEL management's guidance of Rs 27,000 crore order inflows for FY26 appears conservatively framed.

Choice Broking said BEL management's guidance of Rs 27,000 crore order inflows for FY26 appears conservatively framed. Choice Broking said BEL management's guidance of Rs 27,000 crore order inflows for FY26 appears conservatively framed.

Choice Broking said BEL management's guidance of Rs 27,000 crore order inflows for FY26 appears conservatively framed.Choice Broking in its latest note said the December quarter results supported its constructive stance on the defence sector, adding that defence PSUs continued to anchor sector profitability with stable execution and margin discipline, while private players showed improvement in operating leverage despite bottom-line volatility. The combination of steady revenue growth, margin expansion at the aggregate level and sustained year-on-year profit growth signalled endorsement of the sector’s multi-year earnings cycle, the domestic brokerage said.

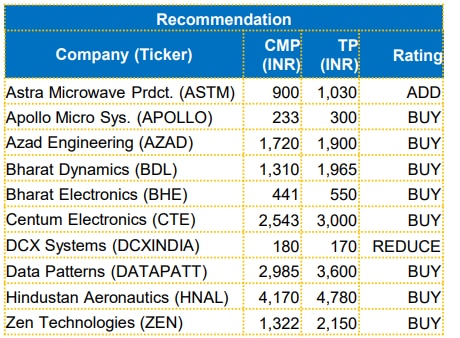

The brokerage suggested 'Buy' on Apollo Micro Systems, Azad Engineering, Bharat Dynamics Ltd, Bharat Electronics Ltd (BEL), Centum Electronics, Data Patterns (India) Ltd, Hindustan Aeronautics (HAL) and Zen Technologies Ltd. It suggested 'Add; rating on Astra Microwave Products Ltd and 'Reduce' rating on DCX Systems. Among these 10 defence stocks, it preferred BEL, BDL and Data Patterns.

BEL | Buy | Target: Rs 550

Choice Broking said the BEL management's guidance of Rs 27,000 crore order inflows for FY26 appears conservatively framed, with multiple large programmes now in advanced stages. It sees near-term optionality from NGC orders of Rs 3,000–5,000 crore in Q4, with a further Rs 10,000–12,000 crore spillover into H1FY27. It is also positive on LCA (Tejas) electronics orders of Rs 2,400 crore and EW programmes such as Satrugat/Samagat, where trial resolution has materially improved.

"We believe BEL's strategic shift, from supplier to system-level integrator, is the key rerating driver. Leadership roles in programmes, such as QRSAM and Project Kusha increase execution stickiness, pricing power and lifecycle revenues. Rising indigenisation level currently at appx. 70–75 per cent and proactive semiconductor redesign materially derisk supply chains and protect margin," Choice Broking said.

Choice said it likes BEL, underpinned by its robust long-term growth visibility, supported by a healthy order book and strong order pipeline.

Data Patterns | Buy | Target: Rs 3,600

Choice said it sees the management commentary as firmly reinforcing an IP-led, system-centric growth strategy, consciously prioritising earnings quality and long-cycle scale over near-term revenue acceleration. The all-time high order book of Rs 1867.80 crore and Rs 1,100 crore of negotiated but yet-to-be-awarded orders, suggests a strong near-term inflow pipeline, it said.

"Importantly, the management’s repeated emphasis on selective contract participation and a sharp focus on IP-owned, core-design programmes structurally protect margin and avoid commoditised L1-led contracts. Conversion of large development programmes into scalable production orders, we believe, is the key inflection point," it said.

Choice said it retained its positive stance on Data Patterns, underpinned by its robust long-term growth visibility, supported by a healthy order book and strong order pipeline. It suggested a 'Buy' and a target of Rs 3,600 on the stock.

BDL | Buy | Target: Rs 1,965

Choice Broking said BDL’s long-term investment case remains firmly intact, adding that the defence PSU is supported by a structurally strong missile demand outlook, a robust order book of 8 times FY25 revenue and an incremental opportunity pipeline of Rs 20,000 crore, providing multi-year earnings visibility.

"While near-term earnings volatility may persist due to delivery phasing, we expect FY27–FY28E to mark a more stable execution phase, translating into improved revenue and margin normalisation. Given BDL’s strategic relevance, deep programme pipeline and long runway of indigenous missile production, we maintain our BUY rating with a target price of INR 1,965, valuing the stock at 35x FY28E EPS," Choice Broking said.

How much gold, equity and debt should you hold in uncertain times? Experts explain

How much gold, equity and debt should you hold in uncertain times? Experts explain DRDO’s ‘eye in the sky’ gets final operational clearance: Here’s what it means

DRDO’s ‘eye in the sky’ gets final operational clearance: Here’s what it means Haryana's new plan for Gurgaon workers: More work from home to beat traffic chaos

Haryana's new plan for Gurgaon workers: More work from home to beat traffic chaos") India remains Russia's No. 2 oil buyer, imports jump 21% in May

India remains Russia's No. 2 oil buyer, imports jump 21% in May No more captchas, crashes and tatkal booking chaos? IRCTC's new website arrives on July 15

No more captchas, crashes and tatkal booking chaos? IRCTC's new website arrives on July 15 “The World Is Rebalancing”: EAM Jaishankar Explains Why Global Politics Is Getting Messier

“The World Is Rebalancing”: EAM Jaishankar Explains Why Global Politics Is Getting Messier Xi Jinping Meets Kim Jong Un In Pyongyang: China Counters Russia, Warns U.S. In Mega Power Shift

Xi Jinping Meets Kim Jong Un In Pyongyang: China Counters Russia, Warns U.S. In Mega Power Shift I.T. Stocks Crashed Too Much? Expert Says These Stocks Could Surprise

I.T. Stocks Crashed Too Much? Expert Says These Stocks Could Surprise Explained: Why Rawalakot & Muzaffarabad Are Burning & The Real 1947 History Behind The Crisis!

Explained: Why Rawalakot & Muzaffarabad Are Burning & The Real 1947 History Behind The Crisis! India Today’s SIT Sting: Rs 500 Cr Racket Selling Expired Medicines & Sanitary Pads By The Kilo!

India Today’s SIT Sting: Rs 500 Cr Racket Selling Expired Medicines & Sanitary Pads By The Kilo! ITC shares trading strategy: Stock in consolidation mode - Road ahead for investors

ITC shares trading strategy: Stock in consolidation mode - Road ahead for investors HDFC Bank, ICICI Bank, Axis Bank, RBL Bank, IndusInd Bank, BOB, SBI: Target prices

HDFC Bank, ICICI Bank, Axis Bank, RBL Bank, IndusInd Bank, BOB, SBI: Target prices Vedanta demerger entities listing: Valuations, debt allocation, expert views & fair values

Vedanta demerger entities listing: Valuations, debt allocation, expert views & fair values Vedanta demerger: Aluminium vs Power vs Oil & Gas vs Iron & Steel — Which stock to buy after listing?

Vedanta demerger: Aluminium vs Power vs Oil & Gas vs Iron & Steel — Which stock to buy after listing? 'SpaceX valuation does not fit any traditional matrix': Uday Kotak on historic IPO

'SpaceX valuation does not fit any traditional matrix': Uday Kotak on historic IPO