The brokerage has upgraded its rating on Coal India stock to ‘Buy’. The brokerage has raised its target price by nearly 25% to Rs 506.

The brokerage has upgraded its rating on Coal India stock to ‘Buy’. The brokerage has raised its target price by nearly 25% to Rs 506. The brokerage has upgraded its rating on Coal India stock to ‘Buy’. The brokerage has raised its target price by nearly 25% to Rs 506.

The brokerage has upgraded its rating on Coal India stock to ‘Buy’. The brokerage has raised its target price by nearly 25% to Rs 506.As summer sets in, so are the prospects for energy producers. Geojit Financial Services in its latest note, said the near to medium-term trigger as ‘rising heat, rising demand…’ for Coal India Ltd, highlighting that seasonal factors could accelerate power demand after a muted phase.

The brokerage expects a recovery in the company's coal offtake to offset its subdued performance from earlier in the fiscal year. Geojit noted that state-owned miner consolidated revenue slipped 5.2% year-on-year to Rs 34,924 crore, while profit after tax (PAT) dropped 15.6% to Rs 7,166 crore for the third quarter of FY26.

“Coal offtake reached 188.66 MT during the quarter; while this represents a 3% YoY decline due to a prolonged monsoon, the volume still reflects a continued prioritisation of supply security for the power sector,” Geojit said.

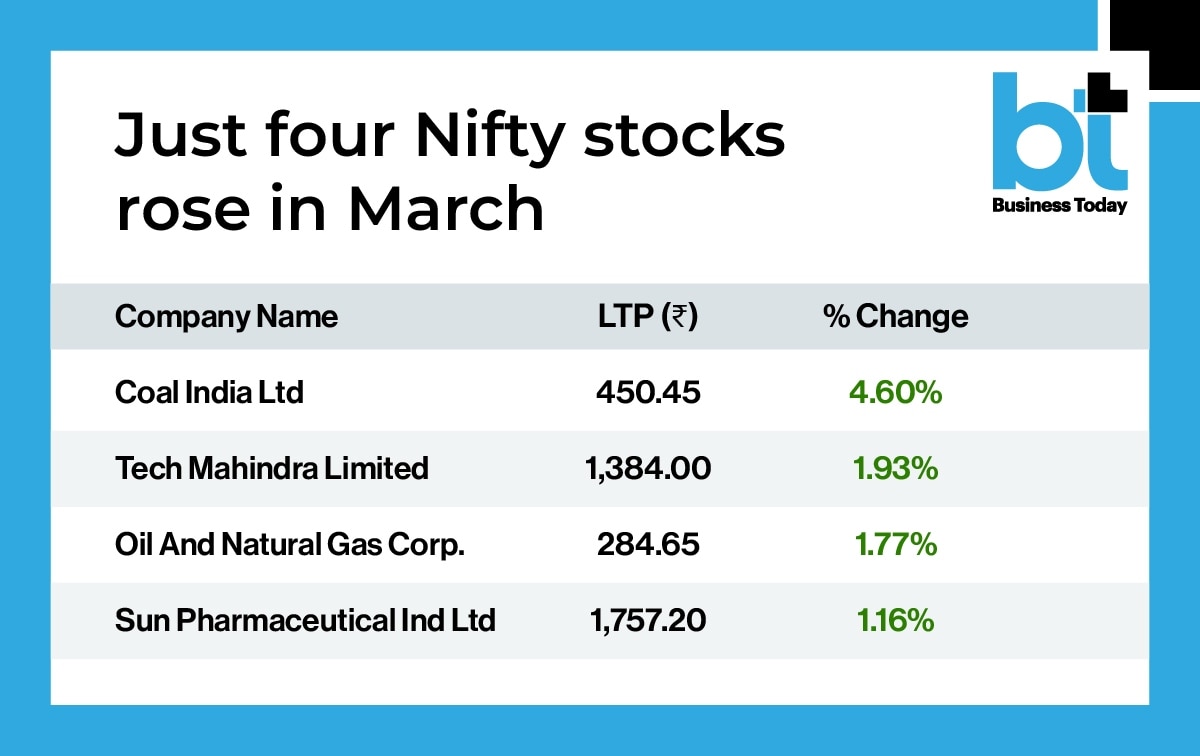

Amid a broader market downturn, the mining major stood out as one of just four Nifty stocks to end the month of March in the green.

Geojit also noted that tensions in Iran have sent global energy prices soaring, creating a highly favourable setup for Coal India to benefit from higher e-auction realisations as industries pivot from costly imports to domestic coal.

The brokerage has upgraded its rating on Coal India stock to ‘Buy’. The brokerage has raised its target price by nearly 25% to Rs 506 from its previous target of Rs 405 in August 2025. Valuing the stock at 6.3x FY28E EV/EBITDA, this revised target indicates a potential 12.38% upside from the current market price of Rs 450.25.

“The company aims to increase their coal production to 1 billion tonne by FY28-29,” Geojit said, highlighting a 500 MW solar power pact in Uttar Pradesh and a strategic foray into critical minerals with a rare earth element block in Maharashtra.

Here’s what the new IIP series shows about FY27 factory output

Here’s what the new IIP series shows about FY27 factory output Here’s how vaccine alliance Gavi committed to speed Ebola vaccine

Here’s how vaccine alliance Gavi committed to speed Ebola vaccine Vodafone Idea: After 32% in a month, is the stock headed for more upside in June?

Vodafone Idea: After 32% in a month, is the stock headed for more upside in June? Annamalai was offered Rajya Sabha seat, declined; likely to quit BJP: Report

Annamalai was offered Rajya Sabha seat, declined; likely to quit BJP: Report Zee secures FIFA World Cup rights for India, just 10 days before the tournament kicks off

Zee secures FIFA World Cup rights for India, just 10 days before the tournament kicks off Piyush Goyal: Most India-U.S. Trade Issues Already Resolved

Piyush Goyal: Most India-U.S. Trade Issues Already Resolved India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review

India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review "Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs

"Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices?

Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices? India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest Pace

India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest Pace NHPC OFS opens June 2 as govt sets ₹71 floor price for up to 6% stake sale

NHPC OFS opens June 2 as govt sets ₹71 floor price for up to 6% stake sale  NMDC Steel shares jump 14% on Q4 profit revival; more steam left in the stock?

NMDC Steel shares jump 14% on Q4 profit revival; more steam left in the stock? Zee Entertainment shares jump 16% in five sessions; key triggers, target price

Zee Entertainment shares jump 16% in five sessions; key triggers, target price Prestige Estates: Multibagger realty stock rises 24% from 52-week low; buy, sell or hold?

Prestige Estates: Multibagger realty stock rises 24% from 52-week low; buy, sell or hold? Why Sensex, Nifty plunged for fourth straight session today; what investors should watch next

Why Sensex, Nifty plunged for fourth straight session today; what investors should watch next