MOFSL estimated TCS to report CC revenue growth of 1.5 per cent QoQ in Q4, while it sees Wipro posting 1 per cent growth.

MOFSL estimated TCS to report CC revenue growth of 1.5 per cent QoQ in Q4, while it sees Wipro posting 1 per cent growth. MOFSL estimated TCS to report CC revenue growth of 1.5 per cent QoQ in Q4, while it sees Wipro posting 1 per cent growth.

MOFSL estimated TCS to report CC revenue growth of 1.5 per cent QoQ in Q4, while it sees Wipro posting 1 per cent growth.Ahead of March quarter results, MOFSL suggested a preference for HCL Technologies Ltd and Tech Mahindra Ltd, saying Coforge Ltd is its top midcap IT stock pick. The domestic brokerage said it likes HCL Tech as the IT firm remains the fastest-growing large-cap IT services firm. It likes HCL Tech's all-weather portfolio, which continues to outperform in an uncertain demand environment. At current valuations, upside risks meaningfully outweigh downside risks, MOFSL said.

For Tech Mahindra, it sees signs of transformation under the new leadership and improving execution in BFSI. TechM's transformation remains relatively decoupled from discretionary spending, it said.

In the case of Coforge, MOFSL said it remained its top pick.

"We believe Coforge's strong executable order book and resilient client spending across verticals bode well for its organic business. Encora’s acquisition expands Coforge's presence in the Hi-Tech and Healthcare verticals. We continue to view Coforge as a structurally strong mid-tier player well-placed to benefit from vendor consolidation/cost-takeout deals and digital transformation," it said.

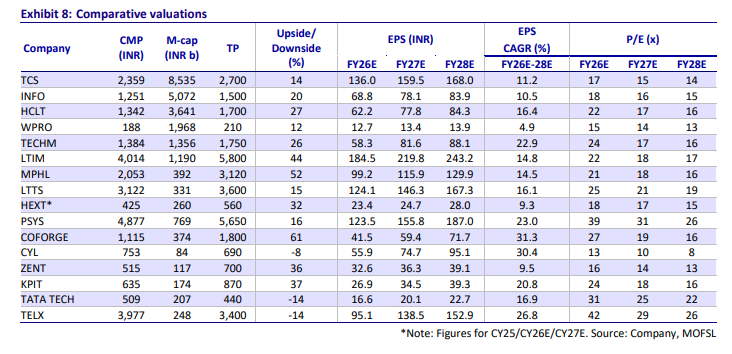

Target prices for TCS, Infosys, Wipro, HCL Tech, TechM, Coforge

MOFSL suggested 'Buy' on TCS, Infosys, Wipro, TechM, LTIMindtree (LTTS), Hexaware, Mphasis, Persistent Systems and KPIT Technologies. These stocks present up to 52 per cent potential upsides, as per MOFSL. The brokerage has has 'Sell' on Tata Tech, Tata Elxsi and Cyient and 'Hold' on Wipro and LTTS.

Q4 IT preview

MOFSL said after a whirlwind couple of months, driven by narrative shocks, Q4 numbers are likely to be somewhat uneventful. The IT witnessed no major disruptions from the ongoing war on numbers yet, and it does not see major evidence of deflationary shocks from AI implementation yet.

"However, we concede that both these data sets are backward-looking. If the war persists, demand is likely to be affected, whereas AI deflation is more a question of what AI will be capable of in the next two to five years, rather than the last quarter," it said.

MOFSL said Q4 results are likely to mirror this set-up, with quarter-on-quarter (QoQ) constant currency (CC) growth expected in the range of minus 1 per cent to 1.5 per cent for largecaps, and midcaps expected to outperform with a growth range of minus 0.5 per cent to 3.5 per cent. For Q4, it expects aggregate revenue for its coverage IT universe to grow 11.3 per cent YoY, while EBIT and PAT are likely to grow 12.9 per cent and 10.8 per cent YoY, in rupee terms, respectively.

FY27 guidance

On guidance, exit rates for most large-caps now appear relatively favorable. MOFSL expects organic year-on-year (YoY) CC growth exits of 4.3 per cent for Infosys and 4.9 per cent for HCL Tech in Q4FY26.

"However, we expect companies to exercise caution in light of the current geopolitical environment. We expect Infosys to guide FY27 revenue growth of 1.5-4.5 per cent YoY in CC terms. The CQGR ask at the lower end is 0.5 per cent, allowing for some deterioration in macros and headwinds from the Daimler ramp-down. There is potential for an upgrade if they backfill Daimler through the year," it said.

For HCL Tech, MOFSL sees 3–6 per cent YoY CC growth for services. The top-end of this guidance assumes mild improvement in CQGR over FY26, while the bottom end assumes uncertainty from war.

"We expect margins to be range-bound for TCS, Infosys, Mphasis, and Persistent. We expect a margin contraction for Wipro (Harman DTS dilution, wage hikes, slower growth) and HCL Tech (wage hikes, restructuring headwinds and P&P decline). Among mid-caps, Hexaware and LTTS may see 40bp/60bp pressure due to ramp-ups, seasonality, and wage hikes," MOFSL said.

It expects Infosys to maintain 20–22 per cent margin guidance. A slower-than-expected product growth, along with pressure from productivity, may puts HCL Tech's expectations of returning to the 18-19 per cent margin band at risk, MOFSL said.

IT Q4 revenue preview

MOFSL estimated TCS to report CC revenue growth of 1.5 per cent QoQ, while Wipro may post 1 per cent growth, supported by a two-month inorganic contribution from the Harman acquisition. In contrast, Infosys and HCL Tech are seen reporting revenue decline of 0.7 per cent and 0.9 per cent, respectively, due to a weaker second half compared with the first, reflecting front-ended growth and seasonality in software.

Among other large-cap names, Tech Mahindra may report 0.5 per cent QoQ growth, while LTIMindtree may deliver 1.5 per cent CC growth, aided by continued ramp-up of large deals, MOFSL said.

Among mid-tier firms, Persistent Systems is expected to lead with around 3.5 per cent CC QoQ growth. Coforge and Mphasis may post growth of 1.5 per cent and 2.5 per cent, respectively, while Hexaware Technologies could see a 0.5 per cent CC decline due to seasonality and delayed deal closures.

In the ER&D segment, MOFSL expected steady performance. KPIT Technologies may report 1.0 per cent QoQ CC growth, while Tata Technologies could deliver 9.5 per cent growth, driven by around 4.5 per cent inorganic contribution and recovery in the core business. Tata Elxsi and L&T Technology Services may see growth of 2.0 per cent and 1.2 per cent, respectively.

MOFSL added that Cyient DET was expected to report 2.1 per cent CC growth, indicating some stabilisation. It also expected a cross-currency tailwind of around 10-40 basis points sequentially across its coverage universe.

IT Q4 margin preview

MOFSL said TCS and Infosys may see Ebit margins remain stable. However, HCLTech margins are expected to contract 140 basis points QoQ, due to wage hikes, restructuring headwinds, and a decline in high-margin products and platforms business.

Tech Mahindra is likely to see margin expansion of around 50 basis points, driven by optimisation of fixed-price projects leading to gross margin gains. In contrast, LTIMindtree margins were expected to contract by about 90 basis points QoQ, due to wage hikes, fewer working days, and client-driven productivity programmes.

Among midcap firms, Coforge margins could expand by around 160 basis points QoQ to about 15 per cent, as wage hike-related headwinds ease.

Mphasis and Persistent Systems are likely to see margins remain range-bound. Meanwhile, Zensar Technologies could see a decline of 220 basis points, as earlier one-off benefits and efficiency gains fade along with slower revenue growth.

In the ER&D segment, MOFSL said margins are expected to remain stable or improve for most companies. However, Tata Elxsi may see margin pressure due to wage hikes in the fourth quarter.

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K crore 'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist

'You're in the wrong chair': When Gita Gopinath faced bias as IMF chief economist Can India monetise microdramas as the market booms but profitability remains elusive?

Can India monetise microdramas as the market booms but profitability remains elusive? India needs its own DeepSeek to avoid AI dependence, warns Bernstein

India needs its own DeepSeek to avoid AI dependence, warns Bernstein.") Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock WatchInfosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit Rs 53K croreLast chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet

Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet