Sun Pharma's specialty portfolio might also encounter challenges in passing on increased costs due to pre-existing elevated price points.

Sun Pharma's specialty portfolio might also encounter challenges in passing on increased costs due to pre-existing elevated price points.  Sun Pharma's specialty portfolio might also encounter challenges in passing on increased costs due to pre-existing elevated price points.

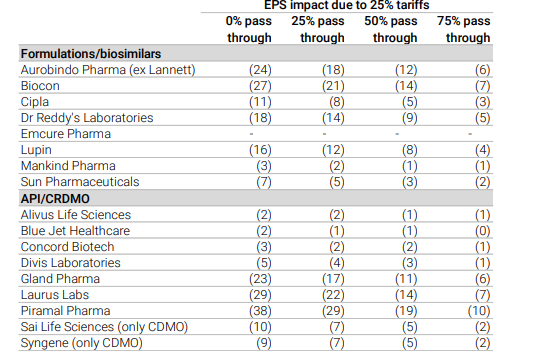

Sun Pharma's specialty portfolio might also encounter challenges in passing on increased costs due to pre-existing elevated price points. Kotak Institutional Equities has highlighted lingering uncertainty over whether a 25% tariff imposed by the US administration on Indian imports will extend to the pharmaceutical sector.

This situation arises amidst confusion regarding the inclusion of pharmaceuticals in the recent US-EU trade agreement. Even if clarity is achieved regarding the applicability of these tariffs to Indian pharmaceuticals, Kotak foresees ongoing ambiguities. The potential for these tariffs to add to existing country-specific tariffs further complicates the situation.

Kotak's analysis assumes a 25% tariff on Indian pharmaceutical companies with a zero pass-through, suggesting a potential earnings per share (EPS) impact ranging from 0 to 27% for generics. This analysis underscores the varied impact across different pharmaceutical sectors and highlights the potential financial repercussions for companies reliant on US markets.

Some Indian pharmaceutical companies may be positioned to mitigate these impacts better due to their US manufacturing presence. Companies such as Cipla, with flexible supply chains and US footprints, might manage potential tariff impacts more effectively than others. The ability to adapt supply chains could be a crucial factor in navigating these challenges.

The anticipated tariffs are expected to affect different pharmaceutical segments unevenly. For instance, Biocon and Aurobindo Pharma are identified as facing significant EPS impacts within the generics and biosimilars domain. The dependency on Indian generics in the US market contrasts with the lesser reliance on biosimilars, complicating the pass-through of higher tariffs.

Sun Pharma's specialty portfolio might also encounter challenges in passing on increased costs due to pre-existing elevated price points. However, limited substitutes for its specialty products may offer some protection against these impacts. For Contract Research and Development Manufacturing Organisations (CRDMOs), tariffs could partially be passed on to clients, though this remains uncertain.

In response to these uncertainties, there is an anticipation that increased US manufacturing by large pharmaceutical entities, particularly for active pharmaceutical ingredients (APIs), may slightly reduce outsourcing practices. The evolving trade landscape thus continues to pose significant strategic challenges for the Indian pharmaceutical sector.

Furthermore, the strategic positioning of companies with diversified portfolios and robust domestic operations may serve as a buffer against these external pressures. Overall, the ongoing developments necessitate careful monitoring as the situation evolves, with the potential for further policy shifts impacting the future outlook for Indian pharma firms reliant on US markets.

Break silos, focus on results: PM Modi's message at key meeting with secretaries

Break silos, focus on results: PM Modi's message at key meeting with secretaries Indian economy resilient despite global shocks; NPAs to remain low: RBI report

Indian economy resilient despite global shocks; NPAs to remain low: RBI report, with rainfall 43% below normal as of June 28.") Why a weak monsoon may not hurt India's economy as much as before, Finance Ministry report explains

Why a weak monsoon may not hurt India's economy as much as before, Finance Ministry report explains Visa-on-arrival for select countries, simpler hotel rules: NITI Aayog proposes tourism overhaul

Visa-on-arrival for select countries, simpler hotel rules: NITI Aayog proposes tourism overhaul First-time ITR filer? Why experts say you should enable the Income Tax Department's e-Filing Vault

First-time ITR filer? Why experts say you should enable the Income Tax Department's e-Filing Vault Rajnath Singh’s Big Vision: Why Gujarat Is Set To Become India’s Next Defence Manufacturing Hub!

Rajnath Singh’s Big Vision: Why Gujarat Is Set To Become India’s Next Defence Manufacturing Hub! WhatsApp's Biggest Transformation Begins! No Phone Number, Ads & Premium Plans

WhatsApp's Biggest Transformation Begins! No Phone Number, Ads & Premium Plans PM Modi Meets Top Secretaries | Watch To Know The Full Agenda

PM Modi Meets Top Secretaries | Watch To Know The Full Agenda 100% Road Tax Waiver For Clean Vehicles! Centre's Big Push For EVs & Green Transport

100% Road Tax Waiver For Clean Vehicles! Centre's Big Push For EVs & Green Transport IPhone 18 Pro Secrets Leaked? Tata Electronics Cyberattack Raises Major Security Concerns

IPhone 18 Pro Secrets Leaked? Tata Electronics Cyberattack Raises Major Security Concerns Calcutta Stock Exchange shares rally in unlisted market; details here

Calcutta Stock Exchange shares rally in unlisted market; details here YES Bank gets rating upgrade for infrastructure, tier II bonds; key details

YES Bank gets rating upgrade for infrastructure, tier II bonds; key details Tata Communications shares: Two factors that may move the Tata Group stock in short term

Tata Communications shares: Two factors that may move the Tata Group stock in short term  Sensex, Nifty extend slide: IT stocks drag markets lower; what to expect next

Sensex, Nifty extend slide: IT stocks drag markets lower; what to expect next Bharti Airtel deserves to trade at a valuation premium against global peers, says Nomura

Bharti Airtel deserves to trade at a valuation premium against global peers, says Nomura