Retail investors have a 15 per cent allocation in the buyback, which means that 1.5 crore shares worth Rs 2,700 crore shall be bought back from their quota.

Retail investors have a 15 per cent allocation in the buyback, which means that 1.5 crore shares worth Rs 2,700 crore shall be bought back from their quota. Retail investors have a 15 per cent allocation in the buyback, which means that 1.5 crore shares worth Rs 2,700 crore shall be bought back from their quota.

Retail investors have a 15 per cent allocation in the buyback, which means that 1.5 crore shares worth Rs 2,700 crore shall be bought back from their quota.Infosys announced its biggest ever share buyback of Rs 18,000 crore on Thursday, September 11, 2025. The IT solutions major said that it will be buying back 10 crore equity shares, representing 2.41 per cent of the total equity shares outstanding. The price of buyback has been fixed at Rs 1,800 per share, suggesting a 18 per cent premium at its price at Rs 1,525 as of September 12.

All equity shareholders of the company as on the record date (which is yet to be announced) shall be considered eligible to participate in the buy back. Retail investors have a 15 per cent allocation in the buyback, which means that 1.5 crore shares worth Rs 2,700 crore shall be bought back from their quota.

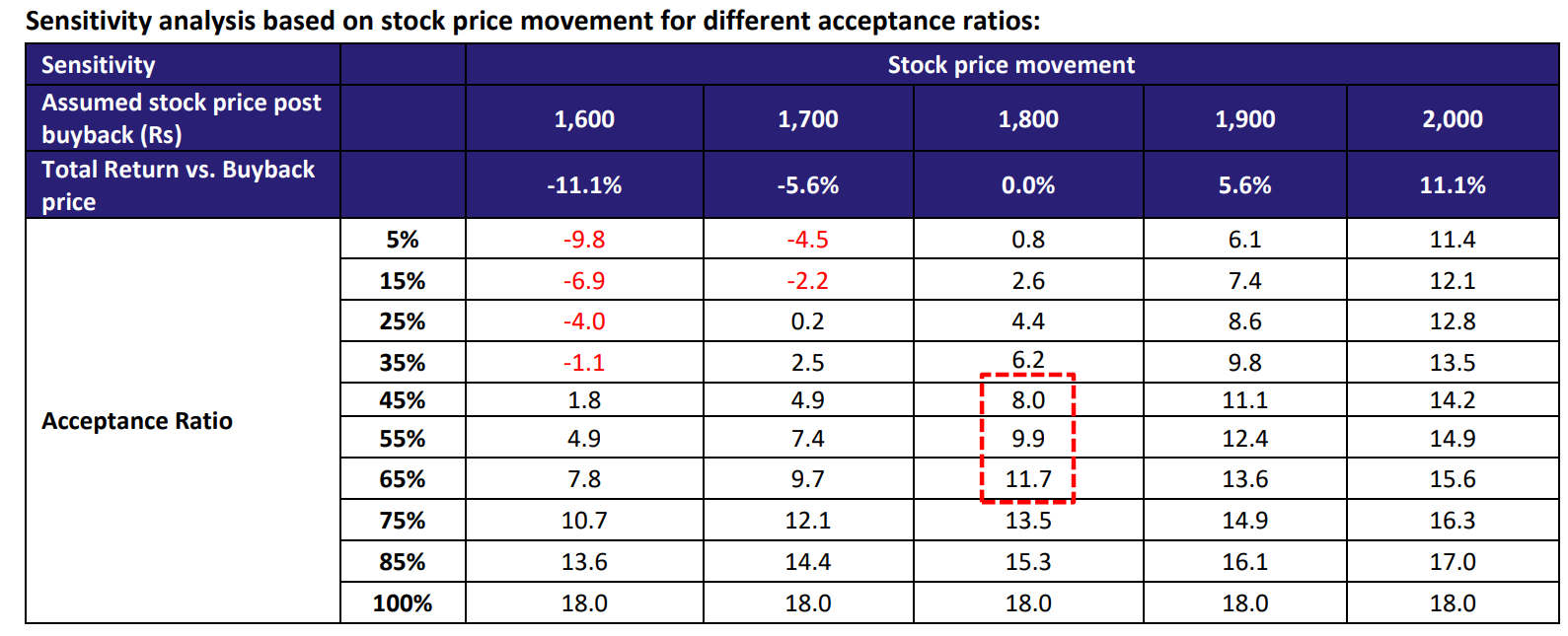

Sunny Agrawal, Head of Fundamental Equity Research at SBI Securities has penciled various pay-off scenarios based on the tentative acceptance ratio and calculated pre-tax return on investment (RoI) based on that calculation. The broking firm has assumed 100 per cent participation from the retail segment and an investor can buy a maximum of 111 equity shares (Rs 2,00,000) at Rs 1,800 apiece to be eligible in this category.

The acceptance ratio for the buyback is expected to be low due to heavy oversubscription and euphoria. A fraction of shares tendered by retail investors are likely to be accepted. Retail investors must understand that only a small portion of shares tendered will be accepted in the buyback and remaining shares will stay with them.

According to SBI's research, at 100 per cent participation for full quota an investor can see buyback of 5-111 equity shares, based on various acceptance ratios and make a profit of Rs 1,375-30,525. This indicates a tentative pre-tax RoI of 0.8-18 per cent for the investor.

According to Agrawal, 45-55 per cent acceptance ratio is the likely scenario for the small investor who will make a 8-11.7 per cent pre-tax RoI and profit of Rs 13,475-19,800, based on the buyback of 49 to 72 equity shares. One should note that the buyback is through a tender offer route and shareholders with holding value of less than Rs 2 lakh shall be considered in this category.

Tax Implication

A buyback is when a company purchases its own shares from existing shareholders, thereby reducing the total number of shares in the market. This route is taken due to various reasons including to push the value of existing shares, to improve earnings per share (EPS) by lowering the share count, to prevent hostile takeovers, or to deploy surplus cash effectively and others.

Since October 2024, the tax liability has shifted to individual shareholders, not to companies. Buyback amount received by shareholders will be deemed as dividend and will be taxed based on slab rates. The cost of the shares bought back by the company will be treated as a capital loss (either short term or long term), said Agrawal.

The loss may be offset against any other capital gains. If there are not enough capital gains to offset the loss in the current year, it can be carried forward and offset against capital gains in future years, up to a maximum of 8 years," he added.

and added Rs 352 per share for its various institutional subsidiaries.") SBI shares fall for fifth straight session – Should you buy?

SBI shares fall for fifth straight session – Should you buy? Anthropic's Claude chatbot is down in India; Users report error amid outage

Anthropic's Claude chatbot is down in India; Users report error amid outage ED searches Vedanta Group premises in FEMA case: Report

ED searches Vedanta Group premises in FEMA case: Report Bill Gates to not speak at Microsoft Summit? What we know so far

Bill Gates to not speak at Microsoft Summit? What we know so far Oracle’s Larry Ellison races past Bezos and Brin to become world’s third-richest person

Oracle’s Larry Ellison races past Bezos and Brin to become world’s third-richest person Piyush Goyal: Most India-U.S. Trade Issues Already Resolved

Piyush Goyal: Most India-U.S. Trade Issues Already Resolved India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review

India’s $11 Billion Semiconductor Plan | Extreme Summer Gadget Tips + MacBook Neo Review "Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs

"Complete Nonsense…": NVIDIA's Jensen Huang Explains Why AI Won't Steal Software Engineering Jobs Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices?

Gold Demand Falls 70% After Duty Hike; What Lies Ahead For Gold And Silver Prices? India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest PaceSBI shares fall for fifth straight session – Should you buy?

India Inc. Posts 15% Profit Growth In Q4FY26 As Revenue Expands At Fastest PaceSBI shares fall for fifth straight session – Should you buy? IRFC, Mazagon Dock, MRPL, NTPC Green, SJVN shares: Why are PSU stocks with high govt stakes falling?

IRFC, Mazagon Dock, MRPL, NTPC Green, SJVN shares: Why are PSU stocks with high govt stakes falling? Concord Biotech, Newgen Software, ACME Solar shares jump; see target prices, outlook

Concord Biotech, Newgen Software, ACME Solar shares jump; see target prices, outlook IREDA shares fall 8% in two days post Q4 – Brokerage target price hints at 45% upside

IREDA shares fall 8% in two days post Q4 – Brokerage target price hints at 45% upside NMDC shares: Brokerages raise target prices after Q4 earnings; NMDC Steel turns profitable

NMDC shares: Brokerages raise target prices after Q4 earnings; NMDC Steel turns profitable