A year which could have been stupendous year for life insurance industry in terms of business premium growth is suddenly staring at a situation where matching the last year figure seems a daunting challenge. Last three months of financial years have traditionally been the months which witnessed highest collection for the industry. Life insurance sector collected 17.4 per cent and 15.04 per cent premiums in the month of the March in FY18 and FY19, respectively. Now given the lockdown in critical second half of March, premium collection is bound to suffer significantly. "Impact is huge because most cities are now under lockdown. Because of flight cancellations, travel policies are not being bought by customers. Buying new policies where insurers need to carry out medical tests are taking time and have slowdown. No more new policy issuance for NRIs or those with recent travel history. So, overall, insurance industry has been hit from many directions" says Rakesh Goyal, Director, Probus Insurance Broker. We tell you how the insurance industry is dealing with novel coronavirus, or COVID-19.

Life Insurance stares at death claim challenge

Besides the loss of new business premium, the industry is staring at a challenge of increased death claims. Though government has acted proactively and gone for a complete lockdown of 21 days even before the number of death toll entered double digits. However, given the initial signs of community spread becoming apparent and the size of the country, nothing can be taken for granted. "It would be too early at this stage to comment on exponential increase in death claims in life insurance. If India is able to effectively control the spread, then, there could be lesser impact on life insurance claims. The next two weeks are very crucial" says Shailaja Lall, partner, Shardul Amarchand Mangaldas & Co. As India has taken pro-active steps at early stage of the disease the chances of higher death rate and rising claims looks less.

"The threat still remains. Talking about life insurance policies, a number of establishments will continue to honor the claims on existing policies however; the cost of future policies will witness a surge and the number of policies that provide complete coverage might see a fall," says Pankaj Chauhan, MD & CEO, EPOCH Indurance Brokers.

There have also been some proactive steps taken by the industry on product innovation front."IRDA has asked insurers to come up new need-based products for coronavirus, and for which, a few insurers have come up with such need-based specific products to cater to the current requirement," says Goyal of Probus Insurance Broker. These are defined benefit-based product where the benefit is paid on occurrence of the event and no bills are required.

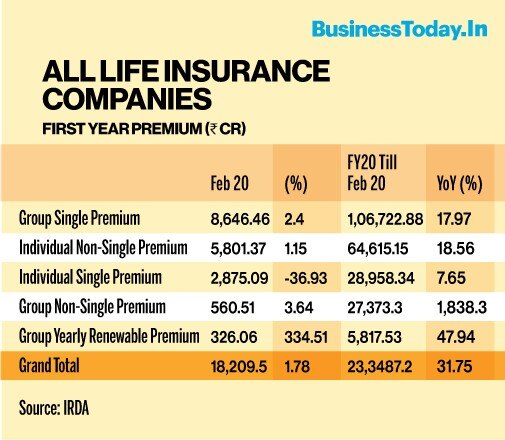

The industry has done well to find an opportunity even in such a situation however it still depends heavily on offline distribution which is bound to suffer. On top of it the market crash could end up deterring new ULIP investors and some existing investors may take the exit. The prospect of industry getting back its momentum will depend both upon the time that India takes to recover from coronavirus and market crash.

General Insurance a mixed bag

Fire and Aviation premium saw one of the biggest rise this year however the given the fact that travel and tourism is the sector which have been worst hit by this crisis. Given the changes in motor insurance by IRDA, third party premium has seen a good surge of 14.3 per cent in FYTD February 2020 as people are going for cheap alternatives for compliance. However, the fall in motor sales was reflected in the tepid growth of 1.2 per cent in the premium collection till February in FY 2020. Till February 2020 the General Insurance industry has maintained FYTD growth of 13.92 per cent, so even in worst case scenario, the industry is expected to close the year with some growth. However, it will be a challenge to recover and register a growth in the new financial year.

Health Insurance to go through corona test

Health Insurance segment has been one of the brightest spot in the general insurance category. This is offered by both multi line general insurance companies and specialised standalone health insurance companies as well. Health insurance premium through multi-line general insurance companies was Rs 46,774 crore till FYTD February 2020, whereas standalone health insurance companies collected a premium of Rs 12,560.96 crore during the same period. Taken together health insurance segment alone had a 34 per cent share in the total business of the entire General Insurance industry.

Corona is going to the biggest challenge the industry has seen so far. The disease has pan-India spread and there is very real risk of it spreading exponentially. Treatment of COVID-19 may need prolonged hospitalisation which could be costly. Many people have some form of health cover, be it corporate of personal health cover. However, as this virus is new, there is a lot of confusion if corona cases would be covered under existing health policies or not. To address the concerns of the policyholders and to bring clarity on the coverage of coronavirus, insurance regulator IRDA came up with guidelines for the insurance companies on March 4. The IRDA guideline stated: "Where hospitalisation is covered in a product, insurers shall ensure that the cases related to coronavirus disease shall be expeditiously handled."

Many health insurers came forward and clarified to their policyholders about the coverage of corona. However, on March 11, WHO notified COVID-19 as pandemic and hence health insurers are no more obligated to entertain defined benefit claim. Despite this there are many health insurers like Aditya Birla Health Insurance, Bajaj Allianz General Insurance and Edelweiss General Insurance who have come forward and clarified that they are still providing cover for coronavirus.

This means the future course of coronavirus will decide the level of challenge health insurers face. "Since, it has been announced that if there are any claims due to coronavirus, wherein the case is of hospitalisation for at least 24 hours, it will be covered under a health policy as per the contract. If things go out of control or claims grow exponentially, this may impact insurance space hugely. However, with recent announcement of coronavirus as a notified disaster, the cost for managing COVID-19 infected patients would be at the rates fixed by the state government, which may come as a cushion for everyone," says Goyal.

This may also be an opportunity for the health insurance industry to prove its metal and win the trust of the prospective customers. "In a high contagion scenario, the ability of all insurers to speedily assess claims, detect fraudulent claims and disburse genuine payments under the policies will go a long way in tempering the pandemic's impact. We could expect a lot of co-operation between the IRDAI, insurers, network hospitals and intermediaries for standardisation in COVID-19 claim settlements to meet the needs of the country" says Shailaja from Shardul Amarchand Mangaldas & Co. This event is likely to re-enforce the need for a health cover which could be a positive for the health insurance industry.

Digital savvy companies will minimise losses

Though insurance offices are included under the list of exempted services under the lockdown however with general restriction on movement there is hardly any chance of new business. "Insurance players with robust digital infrastructure should fare better than others, if there is a sharp rise in COVID-19 cases (as seen in China and Italy). One of the biggest challenges for insurers could be enabling alternative work arrangements for their employees and sales force such that they are more resilient and able to deal with increasing claims and shorter response times" says Shailaja.

Even when the dust settles with weakness in economy is bound to persist in the near term with threat of pay cut and job losses. Many of the answers lies in the next few weeks as how India tackles the corona issue.

ALSO READ: Coronavirus linked insurance claims trickle in; have you bought a policy yet?

ALSO READ: 40% jump in online insurance sales on Covid-19 lockdown

ALSO READ: How to manage your mutual funds in coronavirus-led lockdown

'Positive progress' on Hormuz but no breakthrough: US-Iran indirect talks in Doha conclude

'Positive progress' on Hormuz but no breakthrough: US-Iran indirect talks in Doha conclude  Adani Group, Abu Dhabi’s IHC to invest $11.5 billion in aluminium plant in Odisha: Report

Adani Group, Abu Dhabi’s IHC to invest $11.5 billion in aluminium plant in Odisha: Report India's gold loan rally faces its biggest test: What happens if gold prices correct?

India's gold loan rally faces its biggest test: What happens if gold prices correct? Top stocks in news: CSM Tech, Coal India, Hero Moto, Airtel, Lupin, Tata Tech, NMDC, Vmart

Top stocks in news: CSM Tech, Coal India, Hero Moto, Airtel, Lupin, Tata Tech, NMDC, Vmart Wipro shares in focus as ADRs tumble 17%; all eyes on Infosys, TCS, KPIT Tech

Wipro shares in focus as ADRs tumble 17%; all eyes on Infosys, TCS, KPIT Tech India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump

India-U.S. Trade Deal: Only 1% Remains! Why The Final Stretch Is The Toughest For Modi And Trump Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks

Market Commentary LIVE: Piyush Pandey On Nifty, Sensex & Top Stock Picks TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt!

TN Politics Explodes: 3 Arrested For Alleged ₹35 Cr Plot To Topple Vijay’s TVK Govt! Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities

Market Master LIVE: Ravi Dharamshi On India's Next Big Investment Opportunities Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed!

Ram Mandir Theft Exclusive: The 'Ram Rajya Kosh' Mystery Box & The Inside Nexus Exposed! Stock to buy: Clean Max shares offer 31% upside, says Antique; initiates with 'Buy'

Stock to buy: Clean Max shares offer 31% upside, says Antique; initiates with 'Buy' Eternal, Hexaware Technologies, RITES: Top stocks to buy — Target prices, stop loss & more

Eternal, Hexaware Technologies, RITES: Top stocks to buy — Target prices, stop loss & more Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 95 points; key levels to watch

Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 95 points; key levels to watch Vedanta Aluminium share price target: Emkay sees 22% upside, says risk-reward attractiveWipro shares in focus as ADRs tumble 17%; all eyes on Infosys, TCS, KPIT Tech

Vedanta Aluminium share price target: Emkay sees 22% upside, says risk-reward attractiveWipro shares in focus as ADRs tumble 17%; all eyes on Infosys, TCS, KPIT Tech