The savings generated through NCB can become substantial over time, especially for vehicles with higher own-damage premiums.The savings generated through NCB can become substantial over time, especially for vehicles with higher own-damage premiums.

The savings generated through NCB can become substantial over time, especially for vehicles with higher own-damage premiums.The savings generated through NCB can become substantial over time, especially for vehicles with higher own-damage premiums.For car owners, a claim-free year can translate into significant long-term savings through the No Claim Bonus (NCB), a reward offered by insurers for not raising claims during a policy period. Insurance experts say understanding how NCB works can help policyholders make smarter financial decisions and reduce annual motor insurance costs substantially.

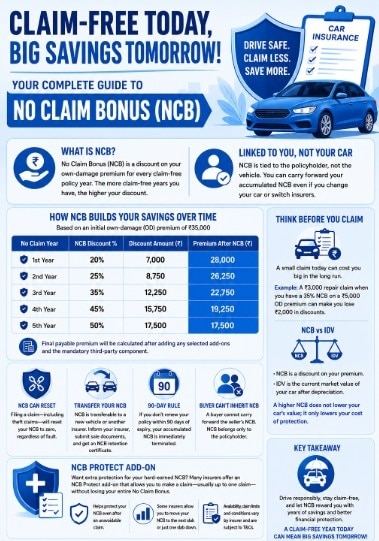

The No Claim Bonus is essentially a discount on the own-damage component of a car insurance premium and is offered during policy renewal. Typically, the discount starts at 20% after the first claim-free year and can gradually rise to as much as 50% after five consecutive years without claims.

Importantly, NCB is linked to the policyholder and not the vehicle itself. This means car owners can retain their accumulated bonus even if they switch insurers or purchase a new car.

MUST-READ: Selling your old car? Have you secured your No Claim Bonus before it expires?

How NCB helps

The savings generated through NCB can become substantial over time, especially for vehicles with higher own-damage premiums.

Based on an initial own-damage premium of Rs 35,000, the discount progression can significantly reduce the payable premium over five years. A 20% NCB in the first claim-free year lowers the premium by Rs 7,000, while a 50% NCB after five consecutive years can reduce the premium by Rs 17,500.

Insurance experts note that many policyholders underestimate the long-term financial value of preserving their NCB.

Mayur Kacholiya, Head – Motor Product at Go Digit General Insurance, said vehicle owners should carefully evaluate the long-term cost of filing small claims.

“A crucial rule of thumb for every car owner is to calculate the long-term impact of a claim before filing it. While it may be tempting to use insurance for minor repairs, a small claim can lead to significant financial loss over time,” he said.

He explained that if a repair costs around Rs 3,000 but the accumulated NCB discount is already substantial, filing a claim may erase years of premium savings.

NCB and IDV

Insurance companies also caution customers against confusing NCB with Insured Declared Value (IDV).

While NCB is a discount applied on the insurance premium, IDV represents the current market value of the vehicle after depreciation. A higher NCB does not reduce the value of the car; it only lowers the cost of insurance coverage.

However, insurers point out that certain situations can reset the NCB regardless of fault. For instance, if a vehicle is stolen and the policyholder raises a claim for the IDV amount, the accumulated NCB is reset to zero.

MUST READ: Workplace injury claims jump 31% YoY, manufacturing sector sees highest claims: Report

NCB can be transferred

Since NCB belongs to the policyholder, it can be transferred to another vehicle or even to a different insurer.

To transfer the bonus, customers generally need to inform their insurer while selling the old vehicle, submit the required sale documents, and obtain an NCB retention or protection certificate.

Insurers also clarify that buyers cannot inherit the previous owner’s NCB. Additionally, policyholders need to remember the 90-day renewal rule. If the insurance policy is not renewed within 90 days of expiry, the accumulated NCB is terminated.

What is NCB protect add-on?

Many insurers now offer an “NCB Protect” add-on cover that allows customers to make limited claims without losing their entire accumulated bonus.

The terms differ across insurers, but some plans allow one claim during the policy year without resetting the NCB completely. Certain insurers also provide options where the NCB moves down by only one slab instead of dropping to zero after a claim.

Insurance experts say such add-ons can help policyholders protect years of disciplined, claim-free driving while still benefiting from insurance coverage during emergencies.

IT stocks: Rebound soon? How Gen AI is driving sentiment — 'Buy' calls, target prices

IT stocks: Rebound soon? How Gen AI is driving sentiment — 'Buy' calls, target prices What triggered the sharp rally in gold and silver ETFs and MCX bullion prices?

What triggered the sharp rally in gold and silver ETFs and MCX bullion prices? Over Rs 22 lakh import duty on 1 kg of gold! Capitalmind's Deepak Shenoy on the flip side of duty hike

Over Rs 22 lakh import duty on 1 kg of gold! Capitalmind's Deepak Shenoy on the flip side of duty hike ") 'Goa could have been our Bali': Investor Shankar Sharma tears into India's tourism failures

'Goa could have been our Bali': Investor Shankar Sharma tears into India's tourism failures Record jet fuel prices bite: Air India suspends Chicago, Shanghai flights; reduces overseas frequencies till August

Record jet fuel prices bite: Air India suspends Chicago, Shanghai flights; reduces overseas frequencies till August Syrma SGS Technology Q4 Results | Profit jumps 55%, Dividend declared | Management On Q4 Performance

Syrma SGS Technology Q4 Results | Profit jumps 55%, Dividend declared | Management On Q4 Performance Tata Power Q4 Results | FY26 PAT Hits Record High; Management Shares Outlook

Tata Power Q4 Results | FY26 PAT Hits Record High; Management Shares Outlook Panic At Chandni Chowk: Will PM Modi’s ‘No Gold’ Call Cripple Delhi’s Iconic Jewellery Hub?

Panic At Chandni Chowk: Will PM Modi’s ‘No Gold’ Call Cripple Delhi’s Iconic Jewellery Hub? From Horoscopes To High Office: CM Vijay’s Astrologer Radhan Pandit Appointed As OSD To Government

From Horoscopes To High Office: CM Vijay’s Astrologer Radhan Pandit Appointed As OSD To Government 'Free Up The Banks': NK Singh Backs New Banking Committee To Overhaul Lending And Infrastructure

'Free Up The Banks': NK Singh Backs New Banking Committee To Overhaul Lending And Infrastructure Gold, silver ETFs: What should you do after Wednesday's rise? | Daily Calls on BTTV

Gold, silver ETFs: What should you do after Wednesday's rise? | Daily Calls on BTTV 'Best investors can...' - Robert Kiyosaki has a Rich Dad lesson, and crash warning!

'Best investors can...' - Robert Kiyosaki has a Rich Dad lesson, and crash warning! Vedanta Demerger: Waiting for new shares? Step-by-step guide to check latest allotment

Vedanta Demerger: Waiting for new shares? Step-by-step guide to check latest allotment Dr Reddy's Laboratories shares: Poor Q4 show — Buy, sell or hold?

Dr Reddy's Laboratories shares: Poor Q4 show — Buy, sell or hold? BT Closing Bell | Sensex, Nifty snap 4-day losing streak; Asian Paints, Tata Steel shares up 4%

BT Closing Bell | Sensex, Nifty snap 4-day losing streak; Asian Paints, Tata Steel shares up 4%