Private sector banks are offering FD rates in the 6.25%–6.50% range, with small differences that can add up over time.Private sector banks are offering FD rates in the 6.25%–6.50% range, with small differences that can add up over time.

Private sector banks are offering FD rates in the 6.25%–6.50% range, with small differences that can add up over time.Private sector banks are offering FD rates in the 6.25%–6.50% range, with small differences that can add up over time.Fixed deposits (FDs) continue to remain a preferred investment avenue for conservative investors, offering predictable returns and capital protection in a volatile global environment. With interest rates stabilising after the Reserve Bank of India (RBI) held the repo rate steady at 5.25%, private sector banks have largely aligned their FD offerings within a narrow range, balancing safety with moderate returns.

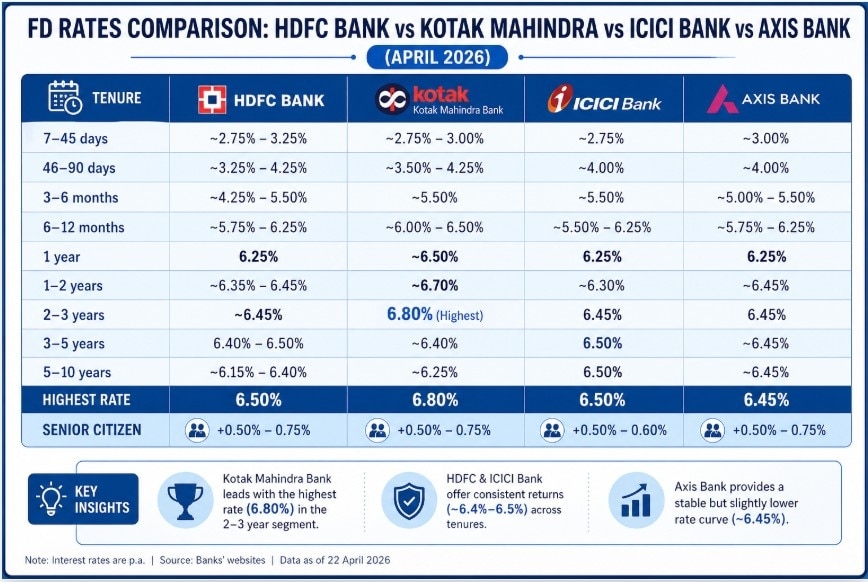

A comparison of four leading private lenders — HDFC Bank, Kotak Mahindra Bank, ICICI Bank, and Axis Bank — shows that while rates are broadly similar, subtle differences across tenures can influence investor decisions.

HDFC Bank

HDFC Bank offers FD rates in the range of 6.25% to 6.50% for key tenures. The highest rate of 6.50% is available for deposits between 3 years and 4 years 7 months.

1 year: 6.25%

2–3 years: ~6.45%

3–5 years: up to 6.50%

The bank maintains a consistent rate structure across tenures, making it suitable for investors seeking stability rather than aggressive returns.

ICICI Bank

ICICI Bank remains competitive, especially in the 3–5 year bucket, where it offers up to 6.50%.

1 year: 6.25%

2 years: 6.30%

3–5 years: 6.50%

5–10 years: 6.50%

Its uniformity across longer tenures makes it attractive for investors locking in rates for the medium to long term.

Axis Bank

Axis Bank follows a relatively flat interest rate curve, offering around 6.25% to 6.45% across most tenures.

1 year: 6.25%

2–5 years: ~6.45%

Up to 10 years: ~6.45%

While it does not lead in any specific tenure, Axis Bank provides predictable and stable returns across durations.

Kotak Mahindra Bank

Kotak Mahindra Bank offers marginally higher rates in certain tenures, with a peak rate of 6.80% for 2–3 year deposits, making it one of the more attractive options among large private banks.

1 year: ~6.50%

2–3 years: up to 6.80%

3–5 years: ~6.40%

This gives Kotak a slight edge for investors targeting mid-term deposits.

Senior citizens

Across all four banks, senior citizens typically receive an additional 0.50%–0.75%, pushing effective returns closer to 7%+ in some cases.

Key takeaways

Kotak Mahindra Bank stands out for mid-term (2–3 year) deposits with higher rates

HDFC Bank and ICICI Bank offer consistent returns across tenures, ideal for stability

Axis Bank provides a balanced but slightly lower rate structure

Overall, private sector banks are offering FD rates largely in the 6.25%–6.50% range, with differences of 20–30 basis points. While these variations may seem small, they can impact returns over longer investment horizons.

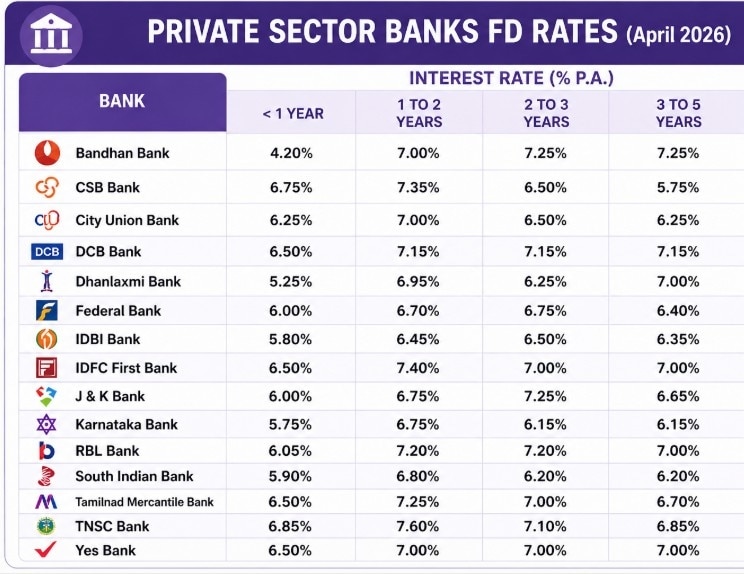

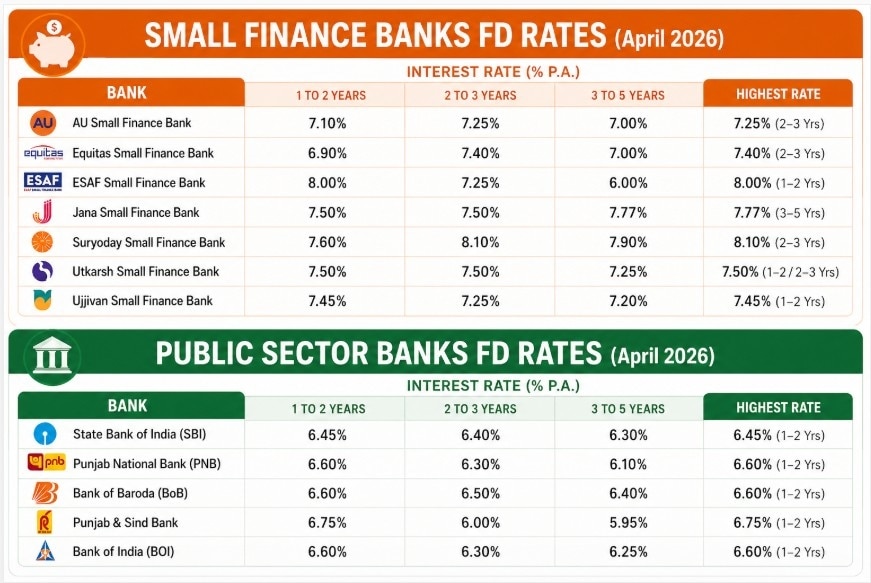

Other banks

Small Finance Banks: Small finance banks offer the highest FD rates, with Suryoday leading at 8.1% (2–3 years) and 7.9% (3–5 years). ESAF offers up to 8%, while Jana provides up to 7.77%. Ujjivan (7.45%) and AU (7.25%) also remain competitive. These banks are attractive for higher returns, but investors should assess credit risk and deposit insurance.

Public Sector Banks: PSU banks like SBI, PNB, and Bank of Baroda offer stable returns of 6.3%–6.6%, with Punjab & Sind Bank slightly higher at 6.75%. While rates are lower, they remain popular due to safety and sovereign backing.

For investors, the decision should not be based on interest rates alone. Factors such as liquidity needs, tenure alignment, and trust in the institution remain equally important. In the current rate cycle, locking in rates for 2–3 years appears to be the most rewarding strategy within private sector banks.

'He's a very tough cookie': Donald Trump praises PM Modi, says he stays out of wars

'He's a very tough cookie': Donald Trump praises PM Modi, says he stays out of wars 'You gotta calm down sometimes and...': Trump claims he urged Israel to agree to Hezbollah ceasefire

'You gotta calm down sometimes and...': Trump claims he urged Israel to agree to Hezbollah ceasefire Iran is the biggest winner from US truce push: Jefferies report

Iran is the biggest winner from US truce push: Jefferies report From cosmic to cosmetic: Why communist China is obsessed with Hindu sacred Rudraksha

From cosmic to cosmetic: Why communist China is obsessed with Hindu sacred Rudraksha India's mutual fund boom faces its biggest test: Can investors stay patient with near-zero returns?

India's mutual fund boom faces its biggest test: Can investors stay patient with near-zero returns? Why Would The RBI Buy Dollars When The Rupee Is Strong?

Why Would The RBI Buy Dollars When The Rupee Is Strong? How Ashishkumar Chauhan Revived NSE & Cleared The IPO Path

How Ashishkumar Chauhan Revived NSE & Cleared The IPO Path Software Stocks Fell Sharply On Accenture's Guidance Cut; Nifty Slips

Software Stocks Fell Sharply On Accenture's Guidance Cut; Nifty Slips "Fast-Track Growth": SEBI Launches GARUDA For AIFs And Aligns SDI Rules With RBI Standards

"Fast-Track Growth": SEBI Launches GARUDA For AIFs And Aligns SDI Rules With RBI Standards Indian IT Stocks Crash To Multi-Year Lows Following Accenture’s Weak Revenue Guidance

Indian IT Stocks Crash To Multi-Year Lows Following Accenture’s Weak Revenue Guidance Jio Platforms IPO: Mukesh Ambani about to realise ₹15 lakh crore dream a decade in making?

Jio Platforms IPO: Mukesh Ambani about to realise ₹15 lakh crore dream a decade in making? Sensex, Nifty snap five-day gaining streak; analysts expect recovery in short term

Sensex, Nifty snap five-day gaining streak; analysts expect recovery in short term  Jio Platforms files DRHP to launch IPO: Check business, financials, key shareholders & more

Jio Platforms files DRHP to launch IPO: Check business, financials, key shareholders & more NSE, India’s financial heartbeat, files for jumbo public listing; sparks global interest

NSE, India’s financial heartbeat, files for jumbo public listing; sparks global interest RIL stock outlook post 49th AGM: Stay cautious, say analysts; price targets, resistance and more

RIL stock outlook post 49th AGM: Stay cautious, say analysts; price targets, resistance and more