Zerodha CEO Nithin Kamath noted that STT was originally introduced at a time when long-term capital gains (LTCG) tax on equities was zero.

Zerodha CEO Nithin Kamath noted that STT was originally introduced at a time when long-term capital gains (LTCG) tax on equities was zero.Ahead of the Union Budget 2026, Zerodha CEO Nithin Kamath has flagged concerns over the steady rise in Securities Transaction Tax (STT), arguing that higher transaction levies may be hurting market activity and even government revenues. “As a market participant, I always hope the Budget will reduce STT, but it keeps going up,” Kamath said, pointing to what he sees as a weakening rationale for the tax in its current form.

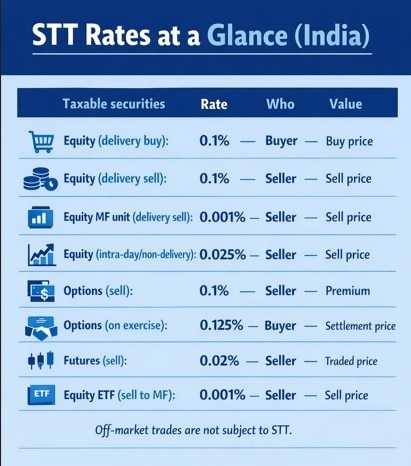

STT is a direct tax levied on the purchase and sale of securities, including equities, derivatives and equity-oriented mutual funds, on recognised stock exchanges. Introduced as a simple, non-refundable levy on transaction value, it was designed to curb tax evasion while ensuring steady revenue collection from capital market activity.

Kamath noted that STT was originally introduced at a time when long-term capital gains (LTCG) tax on equities was zero. “It made sense then as a low-friction way for the government to collect revenue from markets,” he said. However, with LTCG tax now reinstated, he questioned the logic of repeatedly raising STT rather than rolling it back. “In effect, investors are being taxed twice—once per transaction through STT and again on capital gains,” he added.

The concern has sharpened after the sharp hike in STT on derivatives announced in Budget 2024. STT on futures was raised by about 60% from 0.0125% to 0.02%, while options STT was increased from 0.0625% to 0.1%. Kamath acknowledged that the immediate impact appeared muted. “The bull market continued and participation surged, so volumes didn’t fall right away,” he said.

However, he argued that the true impact of higher transaction costs becomes visible when market conditions normalise. “Markets don’t always have bull runs. The effect of higher STT showed up in the year we just had,” Kamath said, suggesting that elevated costs disproportionately hurt trading activity during periods of lower volatility and weaker sentiment, especially in the highly volume-sensitive derivatives segment.

Kamath also pointed to what he described as a revenue paradox. The government had projected STT collections of about ₹78,000 crore for FY 2025–26. Actual collections so far, until January 11, stand at roughly ₹45,000 crore. Even assuming an additional ₹12,000 crore by March-end, total collections would be around ₹57,000 crore—nearly 25% below projections. “I think the government would have collected a lot more without the 2024 hike,” he said, implying that higher rates may have shrunk the tax base.

At the same time, Kamath acknowledged his own conflict of interest. “Of course, disclaimer: I’ll benefit from lower STT, so my opinion is naturally biased,” he said.

Separately, Kamath flagged an operational nuance for market participants this year. With the Union Budget falling on a Sunday and markets open, Zerodha is among a handful of brokers allowing BTST (buy today, sell tomorrow) trades on that day. However, investors buying mutual funds on Sunday will not receive the same-day NAV, he cautioned.

STT applicability

STT applies to transactions in “securities” traded on recognised stock exchanges in India. While the STT Act does not independently define the term, it borrows the definition from the Securities Contracts (Regulation) Act, 1956 and the Income-tax Act, 1961. Under these laws, securities include shares, stocks, bonds, debentures and other marketable instruments of companies, derivatives, units issued by collective investment schemes, equity-oriented mutual fund units, government securities of an equity nature, rights or interests in securities, and securitised debt instruments. STT is levied only when these securities are traded on recognised exchanges; off-market and private transactions remain outside its scope.

STT is designed as a simple, transaction-based direct tax. It is primarily imposed on sell-side transactions in futures and options. For calculation purposes, futures are valued at the actual traded price, while options are taxed on the premium or, in case of exercise, on the settlement price. The clearing member is responsible for paying the aggregate STT collected from all trading members under it.

The tax is levied immediately upon completion of a transaction, making the system transparent and efficient, and minimising defaults. However, as STT is charged over and above the transaction value, it increases the overall cost of trading for investors and traders in the securities market.

Trump declares US guardian of Strait of Hormuz and mandates 20% global cargo fee

Trump declares US guardian of Strait of Hormuz and mandates 20% global cargo fee ") Crude oil, electronics and gems and jewellery top three imports adding to trade deficit

Crude oil, electronics and gems and jewellery top three imports adding to trade deficit What's driving the rapid growth and interest in India's gold loan market

What's driving the rapid growth and interest in India's gold loan market How REITs are becoming a rewarding investment proposition

How REITs are becoming a rewarding investment proposition Banks set for Q1 credit boost, but margin pressure may spoil the party

Banks set for Q1 credit boost, but margin pressure may spoil the party Indian I.T. Stocks Face AI Disruption: Why Growth, Margins And PE Multiples May Fall

Indian I.T. Stocks Face AI Disruption: Why Growth, Margins And PE Multiples May Fall The AI Cost Illusion Explained | Instagram New Updates & GoPro Mission 1 Pro First Look | Tech Today

The AI Cost Illusion Explained | Instagram New Updates & GoPro Mission 1 Pro First Look | Tech Today IT Stocks Rally After TCS Q1 Results: Nifty IT Surges, ICICI Direct Shares Outlook

IT Stocks Rally After TCS Q1 Results: Nifty IT Surges, ICICI Direct Shares Outlook India’s Astra Mk2 Missile Production May Open To Private Firms | Defence Policy Shift Explained

India’s Astra Mk2 Missile Production May Open To Private Firms | Defence Policy Shift Explained AI Sector Boom: Pankaj Pandey Reveals The Best Sectors To Invest In India's Data Centre Growth

AI Sector Boom: Pankaj Pandey Reveals The Best Sectors To Invest In India's Data Centre Growth HCLTech Q1 FY27: Profit rises 20% YoY to Rs 4,624 crore; announces Rs 12/share interim dividend

HCLTech Q1 FY27: Profit rises 20% YoY to Rs 4,624 crore; announces Rs 12/share interim dividend Vedanta, demerged stocks: What should investors do? Centrum's Nilesh Jain shares his view

Vedanta, demerged stocks: What should investors do? Centrum's Nilesh Jain shares his view Reliance Power, BLS International, Bajaj Healthcare: Analyst decodes trading strategy

Reliance Power, BLS International, Bajaj Healthcare: Analyst decodes trading strategy  Sensex, Nifty end marginally higher after volatile session; what should investors watch now?

Sensex, Nifty end marginally higher after volatile session; what should investors watch now? Rs 1,616 to Rs 18,141 in five years: Now, this defence stock set to nearly halve, says Kotak

Rs 1,616 to Rs 18,141 in five years: Now, this defence stock set to nearly halve, says Kotak