For any income generated on the 60 per cent amount will be taxable according to the tax slab.

For any income generated on the 60 per cent amount will be taxable according to the tax slab. For any income generated on the 60 per cent amount will be taxable according to the tax slab.

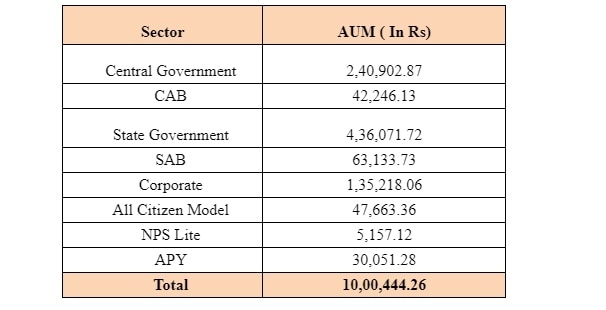

For any income generated on the 60 per cent amount will be taxable according to the tax slab.Assets under management (AUM) of the National Pension System (NPS) and the Atal Pension Yojana (APY) together have crossed Rs 10 trillion. In all they have 66.2 million subscribers, with Rs 47,663, Rs 30,051 and Rs 5,157 coming from NPS Private, APY and NPS Lite, respectively.

NPS was introduced for all central government employees, except those in the armed forces, who joined on or after January 1, 2004. Additionally, many States and Union Territories have adopted the NPS. As of May 1, 2009, NPS has been made accessible to all Indian citizens voluntarily. Furthermore, starting from June 1, 2015, the launch of the Atal Pension Yojana has significantly boosted the reach and effectiveness of social security schemes but is currently open only to non-taxpayers.

The segment-wise status of the NPS and APY as of 25.08.2023:

Deepak Mohanty, Chairperson of the Pension Fund Regulatory and Development Authority (PFRDA), also announced that new features such as a Systematic Withdrawal Plan (SWP) and annuity mix from the same insurer, are expected to be introduced by October, 2023.

Currently, when NPS participants reach the age of 60, they have the option to receive 60 per cent of their retirement savings as a lump sum, with the remaining 40 per cent being automatically allocated towards purchasing an annuity. SWP feature will allow NPS subscribers to opt for periodic withdrawal, monthly, quarterly, half-yearly, or annually, from the lump sum amount until the age of 75.

Also read: Tax calendar for September 2023: Don’t miss these important dates

“There will be no tax on withdrawals up to 60 per cent. For any income generated on the 60 per cent amount will be taxable according to the tax slab,” clarified Mohanty. He added that NPS subscribers will soon be able to choose an annuity mix from the same insurance provider, which means one can get a customised combination like 40 per cent in a single annuity and 60 per cent in a joint annuity plan.

operations") Exclusive: Adani Group to start coal gasification work this year, expand MRO operations, says Jeet Adani

Exclusive: Adani Group to start coal gasification work this year, expand MRO operations, says Jeet Adani Suzlon Energy price target cut by 33%, order inflows at risk; here's why

Suzlon Energy price target cut by 33%, order inflows at risk; here's why  HbA1c-only diagnosis may misclassify diabetes in India, Lancet warns

HbA1c-only diagnosis may misclassify diabetes in India, Lancet warns Tata Steel shares hit record high on Q3 earnings; here's what brokerages say

Tata Steel shares hit record high on Q3 earnings; here's what brokerages say  to Rs 951.62 crore.") YES Bank shares snap two-day fall; analysts advise caution on near-term outlook

YES Bank shares snap two-day fall; analysts advise caution on near-term outlook India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers

India-U.S. Trade Deal Triggers Political Storm As Congress Says Trump Wins, Modi Loses On Farmers US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China

US Map On Trade Deal Shows Full J&K As India, Sending Sharp Signal To Pakistan And China “India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal

“India’s Trade Policy Has Shifted Fundamentally After The US Deal,” Says Piyush Goyal Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted

Govt Scraps Small Car Concessions In Emission Norms; Maruti Seen Most Impacted Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political Firestorm

Bhaijaan Meets Bhagwat: Salman’s RSS Appearance Triggers Political Firestorm Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why

Kalyan Jewellers, Vaibhav Global, Thangamayil, Senco, PN Gadgil & Goldiam jump up to 15%; here's why Shipping Corp shares zoom 14% on Q3 earnings, dividend; check details YES Bank shares snap two-day fall; analysts advise caution on near-term outlookTata Steel shares hit record high on Q3 earnings; here's what brokerages say Suzlon Energy price target cut by 33%, order inflows at risk; here's why

Shipping Corp shares zoom 14% on Q3 earnings, dividend; check details YES Bank shares snap two-day fall; analysts advise caution on near-term outlookTata Steel shares hit record high on Q3 earnings; here's what brokerages say Suzlon Energy price target cut by 33%, order inflows at risk; here's why