Surcharge is an additional tax on income tax payable, not directly on capital gains. It applies once total income (including capital gains) crosses ₹50 lakh.Surcharge is an additional tax on income tax payable, not directly on capital gains. It applies once total income (including capital gains) crosses ₹50 lakh.

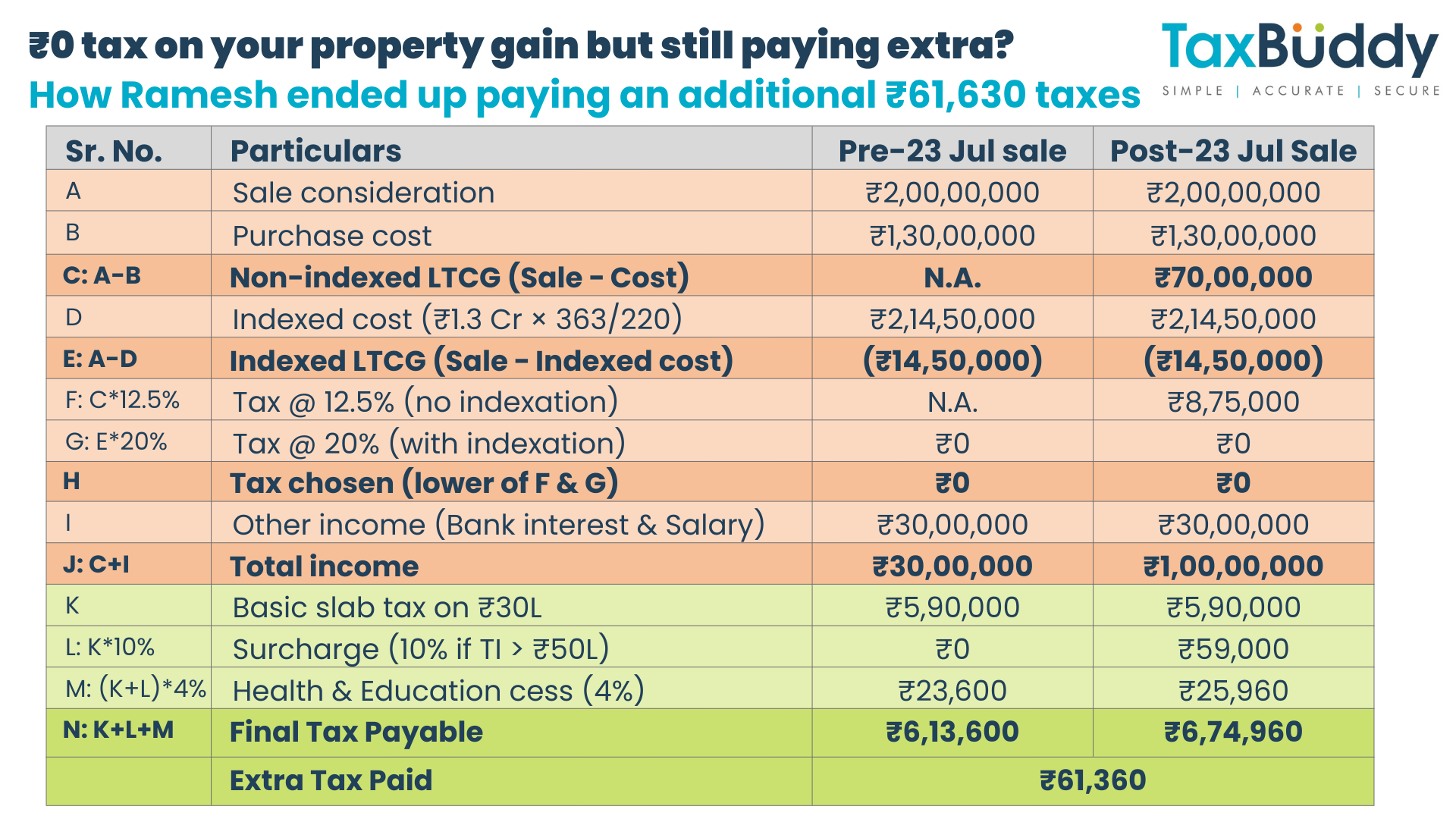

Surcharge is an additional tax on income tax payable, not directly on capital gains. It applies once total income (including capital gains) crosses ₹50 lakh.Surcharge is an additional tax on income tax payable, not directly on capital gains. It applies once total income (including capital gains) crosses ₹50 lakh.When Ramesh sold his property in early 2025, he was shocked to see an additional Rs 61,630 tax liability, even though his sale price generated no real gains after indexation. The reason? Surcharge on property sale transactions, a tax trap many property owners don’t anticipate. For property sellers, the date of transfer now matters more than ever. Two people selling the same house at the same price could end up in very different surcharge brackets depending on whether their sale was before or after July 2024.

Tax advisory platform Tax Buddy explains what happened in Ramesh’s case and how the surcharge rules apply.

1. Ramesh’s Case – No Gain, Still Extra Tax

Purchase: Rs 1.30 crore on 01-Jan-2014

Sale: Rs 2.00 crore in Jan 2025

Other Income: Rs 30 lakh (salary + bank interest)

CII 2013-14 = 220; CII 2024-25 = 363 → Indexed cost = ₹2.145 crore

If indexation was allowed, Ramesh would have made a loss, as his indexed cost exceeded the sale price. Normally, that loss could be carried forward for 8 years to offset future gains.

But after 23 July 2024, indexation for immovable property was removed (except for a comparison benefit). So, for income purposes, his sale was treated as a non-indexed gain of Rs 70 lakh. Even though he didn’t really earn anything, his income jumped from Rs 30 lakh to Rs 1 crore, pushing him into the surcharge bracket.

Before July 2024 (sale in April 2024): Total income = Rs 30 lakh → Tax = Rs6.13 lakh

After July 2024 (sale in Jan 2025): Total income = Rs 1 crore → Surcharge kicks in → Tax = Rs 6.74 lakh

That’s an extra Rs 61,630, purely because of the surcharge trigger.

2. Why this happens

The reason lies in how income vs. tax is calculated post-July 2024 rule change:

Income Rule: For properties bought before 23 July 2024, owners must compute gains both ways (12.5% without indexation vs. 20% with indexation) and pay whichever is lower.

Tax Rule: The “ignored” indexed loss helps reduce tax payable, but not income reported. So for surcharge purposes, the higher non-indexed income is considered.

This mismatch creates a situation where even a loss-making property sale can trigger a higher surcharge slab.

3. Carry forward of losses

Before 23 July 2024: Indexed cost could exceed sale price → Long-term capital loss (LTCL) recognized → Could be carried forward for 8 years.

After 23 July 2024: Indexed loss is ignored → No LTCL recognized → No carry forward or set-off benefit.

This means taxpayers like Ramesh lose both the loss shield and face a surcharge hit.

4. Surcharge slabs on property sale

Surcharge is an additional tax on income tax payable, not directly on capital gains. It applies once total income (including capital gains) crosses Rs 50 lakh.

Old & New Regime Surcharge Slabs (Individuals):

Rs 50 lakh – Rs 1 crore → 10% surcharge

Rs 1 crore – Rs 2 crore → 15% surcharge

Rs 2 crore – Rs 5 crore → 25% surcharge

Above Rs 5 crore → 37% (capped at 25% in New Regime)

Relief for Property Sellers: Surcharge on long-term capital gains (LTCG) is capped at 15%, even for the highest earners.

5. Important Points

Holding Period: Property held for more than 24 months qualifies as long-term.

Tax Rate: LTCG taxed at 12.5% (no indexation) post 23 July 2024. Pre-23 July buyers can compare 20% with indexation vs. 12.5% without.

Exemptions: Sections 54, 54EC, 54F can help reduce tax if reinvested in a house, bonds, or other specified assets.

Marginal Relief: Available if surcharge increase is greater than income exceeding the threshold.

Nominee Complications: On inheritance or transmission, rules differ—important for estate planning.

Ramesh’s case shows how a tax meant for the wealthy can catch ordinary sellers off-guard. Even without real gains, surcharge can inflate your tax bill if the timing of your sale pushes your income over the threshold. If you’re considering selling property, check how your sale impacts total income, whether exemptions can soften the blow, and if timing can help you avoid unnecessary surcharge.

'US stands in danger, not Iran': Trump's ex‑counterterror chief warns after fresh threat to Tehran

'US stands in danger, not Iran': Trump's ex‑counterterror chief warns after fresh threat to Tehran.") Sebi extends IPO approval validity till Sept 30 amid West Asia tensions, weak sentiment

Sebi extends IPO approval validity till Sept 30 amid West Asia tensions, weak sentiment  Major US-Iran war impact: $900 mn loss hits this energy firm's quarterly results – Here is how

Major US-Iran war impact: $900 mn loss hits this energy firm's quarterly results – Here is how 'A whole civilisation will die tonight': Trump's chilling warning to Iran as deadline nears

'A whole civilisation will die tonight': Trump's chilling warning to Iran as deadline nears Nifty at 27,000? Why extreme pessimism could signal a long-term buying opportunity

Nifty at 27,000? Why extreme pessimism could signal a long-term buying opportunity Aludecor – Powering India’s Modern Facades

Aludecor – Powering India’s Modern Facades "Pakistan Ke Kitne Tukde Honge": Rajnath Singh’s Big Warning Amid Bengal Political Battle | Exclusive

"Pakistan Ke Kitne Tukde Honge": Rajnath Singh’s Big Warning Amid Bengal Political Battle | Exclusive "Pakistan Ke Kitne Tukde Honge": Rajnath Singh’s Big Warning Amid Bengal Political Battle | Exclusive

"Pakistan Ke Kitne Tukde Honge": Rajnath Singh’s Big Warning Amid Bengal Political Battle | Exclusive Tata Trusts Row Deepens After Venu Srinivasan Exit, Legal Battle Intensifies

Tata Trusts Row Deepens After Venu Srinivasan Exit, Legal Battle Intensifies Fresh Row At Tata Trusts Over Non-Parsi Trustees | Matter Headed For Courts?

Fresh Row At Tata Trusts Over Non-Parsi Trustees | Matter Headed For Courts? Top stocks in news: Infosys, GAIL, Auro Pharma, AB Capital, Biocon, CleanMax, Muthoot, SRFSebi extends IPO approval validity till Sept 30 amid West Asia tensions, weak sentiment Major US-Iran war impact: $900 mn loss hits this energy firm's quarterly results – Here is how

Top stocks in news: Infosys, GAIL, Auro Pharma, AB Capital, Biocon, CleanMax, Muthoot, SRFSebi extends IPO approval validity till Sept 30 amid West Asia tensions, weak sentiment Major US-Iran war impact: $900 mn loss hits this energy firm's quarterly results – Here is how Sensex, Nifty outlook for tomorrow: Market bull holds edge; levels to watch on Wednesday

Sensex, Nifty outlook for tomorrow: Market bull holds edge; levels to watch on Wednesday