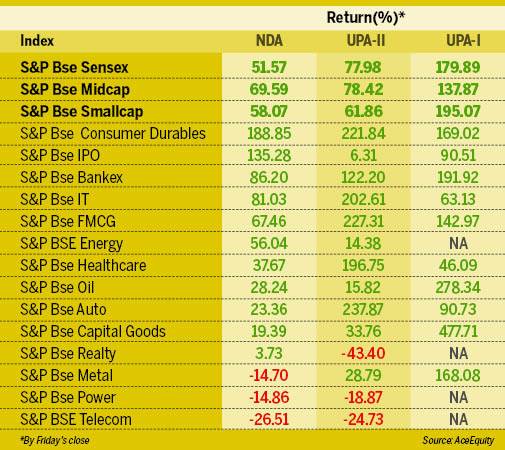

About 900 million voters are sealing the fate of the incumbent government in the world's largest democratic election. Meanwhile, the Sensex has fallen over 6 per cent (by Friday's closing) from an all-time high it hit on April 18. In fact, contrary to what most market participants had anticipated, the Sensex has returned just 51 per cent under PM Narendra Modi's term as compared to UPA-II's (United Progressive Alliance) 78 per cent and UPA-I's 180 per cent, under the then prime minister Manmohan Singh. (See graphic)

The price-to-equity (PE) multiple had jumped quite a bit by May 2014 on hopes of PM Modi winning the elections. The multiple continued to expand and hit 22-mark within the first year of Modi's tenure, suggesting the market had faith in the new leadership. The PE gyrated in 17-22 range over the next three years, only to see a steep fall led by an alarming rise in non-performing assets (NPAs) and hence losses reported by banks over the past couple of quarters. Hopes of earnings rebound never fructified. At present, the Nifty is trading at a 12-month forward P/E of 19.1 times, 8 per cent premium to its long-period average of 17.7 times.

The Modi administration introduced many structural reforms in the last five years. Banks now have more teeth to drag defaulting companies to the National Company Law Tribunal (NCLT), the cash ban of November 2017 led to a surge in online payments and a shift in preference from fixed to financial assets. The introduction of the Real Estate Regulatory Authority (RERA) brought back some faith in real estate. Infrastructure also got a leg up. A prudence fiscal math made the Modi administration a hit among global investors. However, poor job growth and, of late, signs of slowdown in sectors such as auto, FMCG and aviation have put a dent on Modi's reform-oriented image.

BT Buzz: Data localisation - Datacentre service providers see gold

Here is a five-year report card of the Modi government:

DIIs at driving seat

The emergence of the retail investor as a solid source of inflows to financial markets could be seen as one of the biggest achievements of Modi's tenure. From 6.2 million SIP accounts in March 2014 to 26.2 million by March 2019, the cash ban changed investor preference in a big way. Assets under management (AUM) of the mutual fund industry grew more than two-fold to Rs 23.79 lakh crore by March 2019 from Rs 10.10 lakh crore in May 2014. This lifted total market capitalisation of BSE-listed companies to Rs 146 lakh crore from Rs 85.20 lakh crore as on May 26, 2014. So bullish was the sentiment that mutual funds injected over Rs 24,000 crore of inflows in October 2018, their highest ever, even as the benchmark Nifty fell 5 per cent during the month - never seen before.

Macro stability

Another positive development under PM Modi's tenure has been stability in macro indicators. In 2013, India was counted among 'fragile five' nations as it grappled with twin deficits. The fiscal and current account deficit widened at a time when inflation was ruling in two-digit. Inflation quoted at 11.5 per cent in November 2013. Today, it is at 2.9 per cent. Current account deficit (CAD) was at 5.1 per cent of GDP in the December quarter of 2012 as compared to 2.33 per cent in the same quarter of 2018. Fiscal deficit, which was at 4.6 per cent of GDP in FY14, has been reduced to 3.4 per cent of GDP in FY 2018-19.

Thanks to falling crude oil prices, the Modi government had a tailwind for the economy for a considerable part of its tenure. But the government didn't go for a reciprocal cut in duties on fuel, even when Brent crude touched a record low of $30. A few analysts feel the government could have used the opportunity to spur growth. "The government took it easy when oil prices fell. It did not adopt right measures to instil growth during that period," says Sanjiv Bhasin, Executive VP, Markets & Corporate Affairs, IIFL Securities.

Markets versus key policies

The reforms under the Modi government were mostly structural. Some of them have had a visible impact, some are still struggling. Among them is the Goods and Services Tax (GST). Launched in July 2017, it is yet to add desired revenues to the government's kitty. However, the move is said to have triggered a shift in demand from unorganised to organised sectors. This has given a lift to stocks of sectors such as FMCG, retail, food services, luggage, footwear, and apparel.

"Several stocks of these sectors have been re-rated in the past couple of years," says Amnish Aggarwal, Head Research - Prabhudas Lilladher. In the last five years, the BSE Consumer Durables has soared 189 per cent in Modi's tenure. The BSE FMCG index gained 61 per cent during the same period. By comparison, the Sensex has gained just 51 per cent.

The NPA clean-up drive and tranches of capital infusion in public sector banks in all these years bore fruits as the BSE Bankex emerged the second best sectoral performer. The massive Rs 2.11 lakh crore recapitalisation move, executed majorly through bonds, budget, and equity from the capital market, not only revived lending in public sector banks but also improved the SME and MSME space to some extent. Data showed 21 public sector banks (PSB) had gross NPAs of Rs 8.9 lakh crore in FY18, up from Rs 2.09 lakh crore in FY14, as the RBI asked banks to recognise bad loans and make appropriate provisions.

"The IBC has seen some of the largest NPAs in steel, cement and infra sectors being settled," pointed out Aggarwal of Prabhudas Lilladher. According to the rating agency Crisil, the recovery rate under IBC has been 43 per cent as of March 2019. It estimates the banking sector's gross NPA (aggregate) to drop to 10 per cent in March 2019 from 11.5 per cent at the end of FY18.

BT Buzz: Consumer companies are bracing themselves for the worst

Divestment drive

The average yearly divestment under Modi government stood at Rs 57,100 crore, quite higher than UPA-II's Rs 19,873 crore. FY18 became the first year ever when government offloaded stake worth over Rs 1 lakh crore. But, that was largely on the account of ONGC acquiring the government's entire 51.11 per cent stake in oil refiner HPCL for Rs 36,915 crore.

In FY19, disinvestment touched Rs 85,000 crore against the target of Rs 80,000 crore. It was largely done via several tranches of Exchange Traded Fund (ETF) of state-owned companies and cross-selling of government equity in same sector companies. For example, the government transferred its controlling stake in REC to PFC. The real privatisation drive, however, went missing. Air India is a big example.

In 2016-17, the government mopped up Rs 46,247 crore through CPSE disinvestment, as against the budget target of Rs 56,500 crore. In 2015-16, it raised Rs 23,997 crore, as against the budget target of Rs 69,500 crore. In 2014-15, receipts from disinvestment stood at Rs 26,068 crore against a target of Rs 58,425 crore.

Pain points

Although intended good, RERA failed to revive the real estate sector and stocks. The BSE Realty index added only 14 per cent in the last five years. The market didn't appreciate the implementation of long-term capital gains tax either. The government could not bring in reforms in agriculture and labour markets as expected.

"The failure to amend the land acquisition act was not well received by investors and though some progress has been made in labour reforms, by and large, these are areas that need significant reforms," says Vivek Ranjan Misra, Head of Fundamental Research, Karvy Stock Broking.

"Agriculture needs structural reforms, though many reforms need to be carried out at the state level, the centre can nudge states in the desired direction. APMC (agricultural produce market committee) reforms, pricing mechanism and public investment are areas that need attention," he adds.

IPOs under Modi government

In 2014, only seven IPOs had hit Dalal Street. However, 2015 showed a big improvement with 21 IPOs raising Rs 13,513 crore as compared to little over Rs 1,200 crore in 2014. The public issues collected Rs 26,500 crore money in 2016 (26) and Rs 75,278 crore in 2017 (38). IPO listings though fell drastically to 24, raising just Rs 31,731 crore in 2018 as bank frauds, concerns over corporate governance, liquidity issue arising post IL&FS default and a rout in mid and smallcap stocks hit investor sentiment. The IPO mart has somewhat revived in 2019, with six out of eight newly listed companies trading above their issue price so far this year.

As verdict day nears, Dalal Street investors expect the next government - whoever it might be - to continue with the reform process and make the businesses environment friendlier for more investment to keep flowing into Indian equities.

BT Buzz: With or without Modi, 'achche din' ahead for Ayushman Bharat  About 900 million voters are sealing the fate of the incumbent government in the world's largest democratic election.

About 900 million voters are sealing the fate of the incumbent government in the world's largest democratic election. Vinod Aggarwal, Vice Chairman of Eicher Motors; Sanjeev Arora, President, Motion Business at ABB India; Palash Srivastava, Deputy Managing Director at IIFCL and Nilesh Tribhuvan, Managing Partner, White & Brief Advocates & Solicitors") BT Infra Summit 2026: What will power India's next growth spurt?

BT Infra Summit 2026: What will power India's next growth spurt? BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth

BT Infra Summit 2026: How Sagarmala 2.0 is going to steer India's maritime growth Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms

Why Bloomberg isn't ready to add Indian bonds yet despite sweeping market reforms BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage

BT Infra Summit 2026: India's energy security needs a new playbook as clean power, storage and grid modernisation take centre stage ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline

ITR filing 2026: WazirX launches free crypto tax reporting platform ahead of ITR deadline Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down

Why Indians Feel Foreign Infrastructure Is Better: Hitachi India CEO Breaks It Down #BTInfrastructureSummit: How India Is Building Its Infrastructure Muscle For 2047

#BTInfrastructureSummit: How India Is Building Its Infrastructure Muscle For 2047 India's Energy Security: Kearney's Gaurav Gulati On Import Dependence, Storage & Logistics Risks

India's Energy Security: Kearney's Gaurav Gulati On Import Dependence, Storage & Logistics Risks IRFC CMD Manoj Kumar Dubey On ₹20 Lakh Crore Rail Funding, IRFC 2.0 & India's Infra Push

IRFC CMD Manoj Kumar Dubey On ₹20 Lakh Crore Rail Funding, IRFC 2.0 & India's Infra Push "Critical Minerals Are Shaping The Future": G Kishan Reddy On India’s Next Infra Push

"Critical Minerals Are Shaping The Future": G Kishan Reddy On India’s Next Infra Push Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36%

Maruti Suzuki Q1 results: Profit slips 9% YoY to Rs 3,447 crore; revenue climbs 36% ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28%

ITC Q1 results: Profit slips 16% to Rs 4,394 crore YoY; revenue climbs 28% BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more

BTTV Exclusive: M&M CEO Rajesh Jejurikar on Q1 earnings, business outlook, order book and more  Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play?

Nifty IT stocks rebound in July as semiconductor shares falter; reverse AI trade at play? Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21%

Dixon Technologies Q1 earnings: Net profit at Rs 718 crore, revenue rises 21% Amit Gossain, MD, Kone Elevator – India and South Asia; Rajeev Garg, Chief Sales Officer of Jindal Stainless; Bharat Kaushal, Executive Officer at Hitachi India and Ankur Periwal, MD, KPT Pipes.") BT Infra Summit 2026: Experts call for sustainable solutions, technology integration in India’s massive infra push

BT Infra Summit 2026: Experts call for sustainable solutions, technology integration in India’s massive infra push