Bengal’s GDP share decline is structural, driven by industrial slowdown, fiscal constraints, slower growth, and weak private investment—not any single party.Bengal’s GDP share decline is structural, driven by industrial slowdown, fiscal constraints, slower growth, and weak private investment—not any single party.

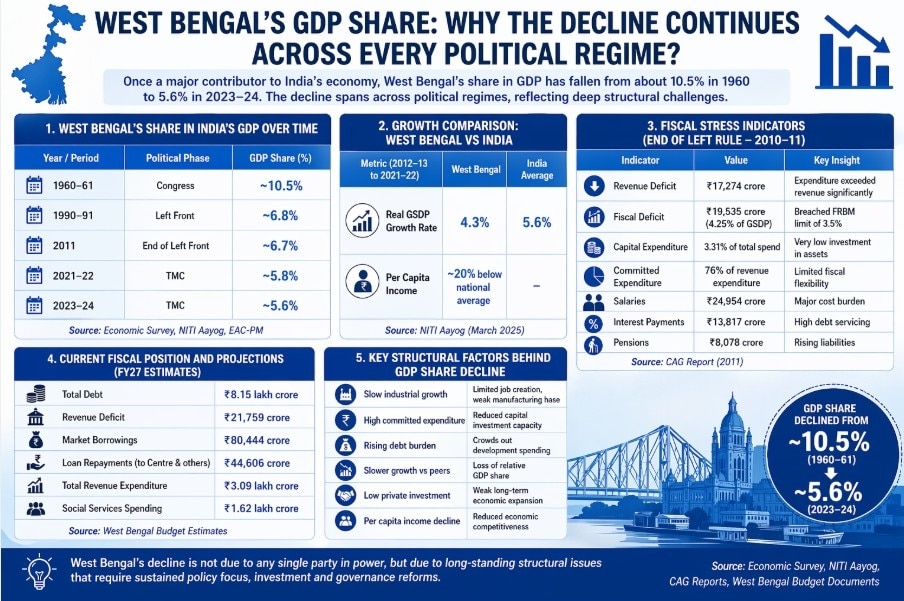

Bengal’s GDP share decline is structural, driven by industrial slowdown, fiscal constraints, slower growth, and weak private investment—not any single party.Bengal’s GDP share decline is structural, driven by industrial slowdown, fiscal constraints, slower growth, and weak private investment—not any single party.Bengal news: West Bengal’s economic trajectory presents a paradox: steady growth in absolute terms, yet a persistent decline in its share of India’s GDP across decades and governments. From contributing around 10.5% to India’s GDP in 1960, the state’s share has fallen to about 5.6% in 2023–24, according to recent estimates and policy reports. This long-term slide spans multiple political regimes — from Congress to the Left Front and now the Trinamool Congress (TMC) — suggesting structural, rather than purely political, causes.

At a headline level, the state’s economy is growing. The Economic Survey 2025 notes that West Bengal’s Net State Domestic Product (NSDP) reached ₹16.32 lakh crore in FY25, with growth improving to around 9%. However, this growth has not kept pace with faster-expanding states, resulting in a relative decline in national share. In essence, West Bengal is growing—but others are growing faster.

MJUST READ: Beach lockdown before ballots: EC bars tourists from Bengal's coastal hubs

Historical legacy and industrial stagnation

The roots of the decline trace back to the post-1960s period, when industrial stagnation began to set in. Labour unrest, capital flight, and policy uncertainty during the 1970s and 1980s weakened the state’s industrial base. While the Left Front government (1977–2011) achieved notable gains in land reforms and rural development, critics argue it struggled to attract large-scale private investment, particularly in manufacturing.

By the end of Left rule, fiscal stress had become acute. A 2011 CAG report highlighted that 76% of revenue expenditure was committed to salaries, pensions, and interest payments, leaving minimal room for capital investment. Capital expenditure stood at just 3.31% of total spending—far below the average for Indian states—indicating a systemic underinvestment in growth-enhancing infrastructure.

Structural fiscal constraints persist

The transition to the TMC government in 2011 brought a renewed focus on growth and welfare, but structural fiscal challenges have persisted. While the debt-to-GSDP ratio improved due to higher nominal growth, underlying issues such as high committed expenditure and limited fiscal space remained unresolved.

A 2021 CAG report pointed to continued reliance on debt-funded consumption and relatively low capital expenditure. Budget estimates suggest the state’s debt could reach ₹8.15 lakh crore by March 2027, with significant portions of expenditure allocated to interest payments and loan repayments. This crowds out productive investment in infrastructure, industry, and job creation.

Growth below national average

Another critical factor is comparative underperformance. According to a NITI Aayog report (March 2025), West Bengal’s real GSDP grew at an average of 4.3% between 2012–13 and 2021–22, compared to the national average of 5.6%. This gap, sustained over a decade, has steadily eroded the state’s share in India’s GDP.

Per capita income trends reinforce this concern. Once above the national average in the 1960s, West Bengal’s per capita income is now about 20% lower, trailing several historically less-developed states.

Limited industrial revival and private investment

Despite improvements in ease of doing business and infrastructure, West Bengal has struggled to replicate the manufacturing-led growth seen in states like Gujarat, Tamil Nadu, or Karnataka. The services sector, while expanding, has not been sufficient to offset the absence of large-scale industrialisation.

Policy uncertainty, land acquisition challenges, and legacy perceptions continue to affect investor sentiment, even as the state attempts to reposition itself as an investment destination.

West Bengal politics and development

The decline in West Bengal’s GDP share is not attributable to any single political party. Instead, it reflects a combination of historical industrial decline, persistent fiscal constraints, slower relative growth, and limited private investment.

How not to lose money in markets: Experts on why protecting capital matters more than chasing returns

How not to lose money in markets: Experts on why protecting capital matters more than chasing returns Meta, Oracle layoffs: Indian H-1B workers in US have 60 days to find a job or leave; Here's why

Meta, Oracle layoffs: Indian H-1B workers in US have 60 days to find a job or leave; Here's why Bought an EV in Delhi? You may not be able to sell it anytime soon

Bought an EV in Delhi? You may not be able to sell it anytime soon 'It is a...' - What Equirus says on Dalmia Bharat acquiring JP Associates cement biz from Adani

'It is a...' - What Equirus says on Dalmia Bharat acquiring JP Associates cement biz from Adani BT Exclusive: We are providing infra to people coming to work from the beach, says Goa CM Pramod Sawant

BT Exclusive: We are providing infra to people coming to work from the beach, says Goa CM Pramod Sawant VA Tech Wabag Q4 Results | Management On Growth, Margins & Massive Order Pipeline

VA Tech Wabag Q4 Results | Management On Growth, Margins & Massive Order Pipeline Daily Calls LIVE: Ask Your Gold Related QUERIES | Gold Update LIVE | Share Market News Today

Daily Calls LIVE: Ask Your Gold Related QUERIES | Gold Update LIVE | Share Market News Today Pakistan’s China-Made JF-17 Faces Scrutiny After Crash During Routine Training Mission

Pakistan’s China-Made JF-17 Faces Scrutiny After Crash During Routine Training Mission Europe Blinked First? Putin Gains Big As UK, EU Quietly Return To Russian Oil Dependence

Europe Blinked First? Putin Gains Big As UK, EU Quietly Return To Russian Oil Dependence Rubio’s India Visit Revives Big Questions Over Quad’s Momentum And Strategic Future

Rubio’s India Visit Revives Big Questions Over Quad’s Momentum And Strategic Future Are India-focused funds showing early signs of recovery after 11 weeks?

Are India-focused funds showing early signs of recovery after 11 weeks? Adani Power, Adani Green, APSEZ share price targets: Bernstein on what funds may have missed

Adani Power, Adani Green, APSEZ share price targets: Bernstein on what funds may have missed BT Closing Bell | Sensex settles 232 pts higher, Nifty above 23,700; Trent shares up 3%

BT Closing Bell | Sensex settles 232 pts higher, Nifty above 23,700; Trent shares up 3% Sun Pharma Q4 PAT up 26% to Rs 2,714 crore; announces final dividend — check amount here'It is a...' - What Equirus says on Dalmia Bharat acquiring JP Associates cement biz from Adani

Sun Pharma Q4 PAT up 26% to Rs 2,714 crore; announces final dividend — check amount here'It is a...' - What Equirus says on Dalmia Bharat acquiring JP Associates cement biz from Adani