YES Bank's return on asset (0.2 per cent) and return on equity (2 per cent) were subdued in FY23 largely on account of lower margins of 2.7 per cent, Nomura India said.

YES Bank's return on asset (0.2 per cent) and return on equity (2 per cent) were subdued in FY23 largely on account of lower margins of 2.7 per cent, Nomura India said. YES Bank's return on asset (0.2 per cent) and return on equity (2 per cent) were subdued in FY23 largely on account of lower margins of 2.7 per cent, Nomura India said.

YES Bank's return on asset (0.2 per cent) and return on equity (2 per cent) were subdued in FY23 largely on account of lower margins of 2.7 per cent, Nomura India said.A day ahead of its September quarter results, YES Bank on Friday received a 'Neutral' call from Nomura India, which initiated coverage on the private lender with a target of Rs 16.50 per share. Nomura said YES Bank's revival post reconstruction in March 2020 has been commendable but the stock adequately captures the positives.

Nomura said the sixth largest private sector bank's return profile, though on an improving trajectory, is significantly lower than peers. YES Bank trades at 1.1 times September 2025 book value per share (BVPS), which the foreign broking firm said adequately captures the positives. Higher recoveries from stress pool pose upside risks to its target while intense competition in deposits could impact margins, stress formation in retail and MSME segments, the brokerage said.

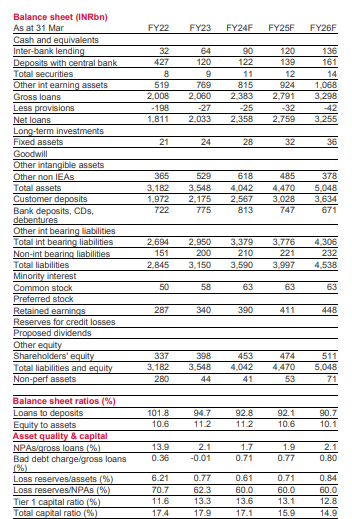

Nomura said YES Bank's return on asset (0.2 per cent) and return on equity (2 per cent) were subdued in FY23 largely on account of lower margins of 2.7 per cent. It expects margins to improve to 3.3-3.6 per cent in FY26-27, driven by a reduction in drag arising out of non-interest earning assets, increase in loan yields and improvement in funding mix.

"Further, we expect healthy growth in core fees to sustain (18 per cent CAGR over FY23-27F) largely driven by robust retail fees, cross-sell and transaction banking. However, elevated opex is expected to limit RoA/RoE improvement to 1 per cent/10 per cent by FY27," it said.

The brokerage said YES Bank has incrementally focused on lending to the retail and SME segments, while running down its bulky corporate book. It expects granular loans to continue to be the key drivers of loan growth (17 per cent CAGR over FY23-27).

The bank’s deposit base halved in FY20. Since then, deposits have witnessed a strong 25 per cent CAGR (FY20-1Q24), with the share of retail deposits inching up, albeit gradually. Nomura India expect a deposits CAGR of 19 per cent over FY23-27F and CASA to improve to 34 per cent by FY27F (vs 31 per cent in FY23.

NOmura said while the bank's non-NPL stress pool (9 per cent of loans) is higher than peers, NPL recoveries continue to be strong, cushioning credit cost. It sees a benign credit environment to keep slippages in the range of 2-2.3 per cent, with credit costs at 0.9-1.1 per cent over FY24-27.

"We expect improving margins and strong core-fee income growth to expand RoA from 0.2 per cent in FY23 to 1 per cent in FY27F, still significantly lower than peers. YES Bank is well positioned to deliver on growth and CET1 (13.6 per ecnt) is comfortable, in our view. We expect a 17 per cent CAGR in loans over FY23-27 (vs 5 per cent in FY20-1Q24) on strong growth in the retail and SME segments," it said.

Also read: ITC shares fall post Q2 results: Should you buy, hold or sell?

Also read: Indraprastha Gas shares tank 10% as Jefferies sees Delhi EV policy impacting CNG sales

WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED

WhatsApp gets a new boss: Kunal Shah to lead platform as Meta bets $900 million on CRED India wants to make more at home. So why are imports still surging?

India wants to make more at home. So why are imports still surging? From BrahMos to Akashteer: UAE explores buying India's frontline defence systems

From BrahMos to Akashteer: UAE explores buying India's frontline defence systems UK PM Keir Starmer steps down: What happens next, how long will it take?

UK PM Keir Starmer steps down: What happens next, how long will it take?") Can you repaint, redecorate or install AC in a rented flat? Here's what the law says

Can you repaint, redecorate or install AC in a rented flat? Here's what the law says Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today

Snap Specs Smart Glasses, Redmi Turbo 5 & OnePlus N Series Launch | Tech Gear EP 7 | Business Today US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students

US Visa Rules Set For Major Overhaul | What It Means For 3.5 Lakh Indian Students Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors?

Market Rally Resumes! Nifty Gains, Crude Falls | What's Next For Investors? UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports

UAE In Talks To Buy BrahMos Missiles? | Big Boost For India's Defence Exports CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era!

CEO-Style Governance & Direct Action: CM Vijay’s First Month Decodes The Shift From Stalin’s Era! Sensex, Nifty trim gains but settle higher; what's ahead for investors?

Sensex, Nifty trim gains but settle higher; what's ahead for investors? Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding

Nearly 121x profit! HFCL promoter's Rs 10 Jio Platforms bet may yield a Rs 5,800 crore holding Explained: Open market share buybacks are back, what this means for Indian investors

Explained: Open market share buybacks are back, what this means for Indian investors Kirloskar Brothers shares jump 7%; key technical levels to watch out for

Kirloskar Brothers shares jump 7%; key technical levels to watch out for CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies

CONCOR shares set for 27% upside despite weak Q1 expectations, says Jefferies