Shares of Ashok Leyland declined 4.95 per cent on Friday to settle at Rs 155.45.

Shares of Ashok Leyland declined 4.95 per cent on Friday to settle at Rs 155.45. Shares of Ashok Leyland declined 4.95 per cent on Friday to settle at Rs 155.45.

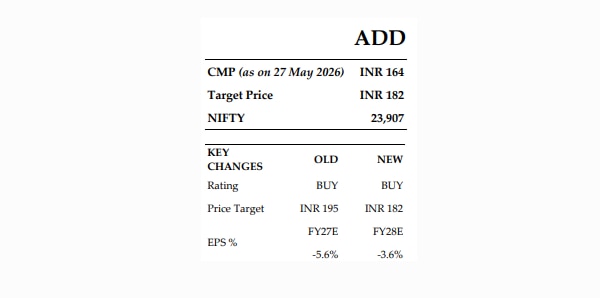

Shares of Ashok Leyland declined 4.95 per cent on Friday to settle at Rs 155.45.HDFC Securities has maintained its 'Add' rating on Ashok Leyland Ltd but lowered the target price on the commercial vehicle maker, citing a challenging near-term business environment.

Commenting on the company's quarterly performance, HDFC Securities said, "EBITDA margin, at 14.6 per cent, declined 46bps YoY but improved 128bps QoQ, above ours and Bloomberg consensus estimates of 14.4 per cent and 14.3 per cent respectively, driven by better price realisations, revenue mix, and focus on cost reduction."

It added, "Despite 20.5 per cent QoQ rise in volumes, operating costs went down only marginally (as a percentage of sales), with main benefits coming from better gross margins (higher by 82bps QoQ)."

On the outlook, HDFC Securities said, "Management is cautiously optimistic on the business, going forward, as while baseline demand drivers remain intact for now, there is rising uncertainty due to geopolitical tensions, commodity cost inflation, and diesel price hikes. It mentioned no significant slowdown in May'26 for both the MHCV and LCV segments, and large fleet operators are still sticking to their fleet replacement plan made for the next 12-18 months."

The brokerage further highlighted that Ashok Leyland expects any near-term weakness in demand to eventually translate into recovery-led growth later in the fiscal year.

"It remains confident that while some setback in demand is expected at the end of Q1 or in Q2, it expects this to convert into pent-up demand rather than lost demand, which will bounce back in H2 FY27, as the average age of the fleet continues to remain high. On exports, it highlighted no significant slowdown in retail demand, although wholesales should drop in Q1 FY27," HDFC Securities stated.

The brokerage also flagged concerns around diesel price hikes. "Though it does not expect it to be a major impact for up to Rs 10-15 hike in diesel prices. However, there are issues with regard to availability of diesel in certain pockets of the country, which management believes could be due to hoarding. It has taken a price hike of 1-1.5 per cent in Apr'26 (over the 1 per cent hike taken in Jan'26). For the remainder of the cost inflation impact in Q1, it expects to mitigate it by focusing on value engineering and controlling operating expenses," HDFC Sec added.

On valuation, the brokerage said, "We value the company's core business at 12.0x Mar-28 EV/EBITDA (vs 12.5x earlier), and add the value of Hinduja Leyland Finance (Rs 14) for a TP of Rs 182 (from Rs 195 earlier), maintaining an ADD rating."

Meanwhile, shares of Ashok Leyland declined 4.95 per cent on Friday to settle at Rs 155.45.

AMFI to renew push for higher overseas investment cap for mutual funds

AMFI to renew push for higher overseas investment cap for mutual funds IPO wealth creators of 2026: One tripled investors’ money; another added ₹1,340 crore

IPO wealth creators of 2026: One tripled investors’ money; another added ₹1,340 crore EPFO offline for 4 days: Is ATM-based PF withdrawal finally around the corner?

EPFO offline for 4 days: Is ATM-based PF withdrawal finally around the corner? Ayodhya Ram Mandir row: Champat Rai, Anil Mishra resign amid donation probe

Ayodhya Ram Mandir row: Champat Rai, Anil Mishra resign amid donation probe Is passport a valid document for SIR? Here's what Election Commission says

Is passport a valid document for SIR? Here's what Election Commission says Tech Gear Show | Latest Tech News, G-Shock, Redmi Turbo 5, HP EliteBook X G2a | EP 8 | Business

Tech Gear Show | Latest Tech News, G-Shock, Redmi Turbo 5, HP EliteBook X G2a | EP 8 | Business Yogi Adityanath Alleges ₹4,600 Crore Purvanchal Expressway Tender Scam By SP

Yogi Adityanath Alleges ₹4,600 Crore Purvanchal Expressway Tender Scam By SP NSE CEO Ashishkumar Chauhan Explains Why Every Entrepreneur Should Consider Listing

NSE CEO Ashishkumar Chauhan Explains Why Every Entrepreneur Should Consider Listing Ram Mandir To Tirupati: Inside Temple Scandals That Shook Devotees' Faith Over The Years

Ram Mandir To Tirupati: Inside Temple Scandals That Shook Devotees' Faith Over The Years Is An Indian Passport Proof Of Citizenship? Harish Salve On Aadhaar, NRC And SIR Controversy

Is An Indian Passport Proof Of Citizenship? Harish Salve On Aadhaar, NRC And SIR Controversy Adani Enterprises, Adani Power, Adani Ports rally up to 61% in three months; is more upside left?

Adani Enterprises, Adani Power, Adani Ports rally up to 61% in three months; is more upside left? TMPV or TMCV shares: Which Tata Motors stock has higher upside potential?

TMPV or TMCV shares: Which Tata Motors stock has higher upside potential? 'Those sectors that were new in 1990s...': Samir Arora says history is repeating

'Those sectors that were new in 1990s...': Samir Arora says history is repeating NSE chief urges startups, MSMEs to view listing as a tool for scale

NSE chief urges startups, MSMEs to view listing as a tool for scale  Indian equities third-biggest losers after Indonesia, Hong Kong in 2026

Indian equities third-biggest losers after Indonesia, Hong Kong in 2026