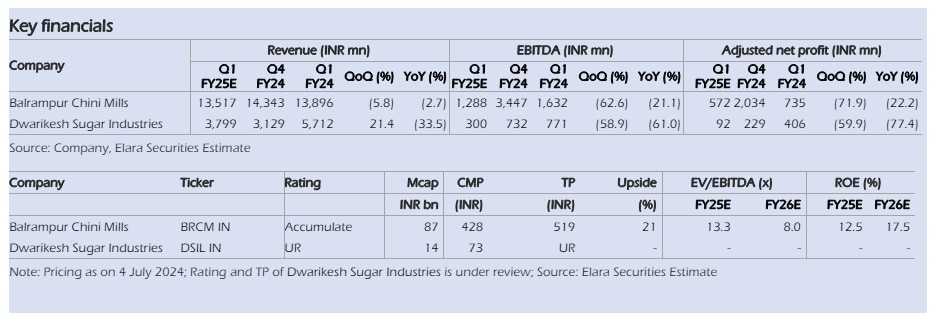

For Balrampur Chini, Elara sees adjusted net profit declining 22.2 per cent to Rs 57.20 crore for the June quarter from Rs 73.50 crore in the same quarter last year.

For Balrampur Chini, Elara sees adjusted net profit declining 22.2 per cent to Rs 57.20 crore for the June quarter from Rs 73.50 crore in the same quarter last year. For Balrampur Chini, Elara sees adjusted net profit declining 22.2 per cent to Rs 57.20 crore for the June quarter from Rs 73.50 crore in the same quarter last year.

For Balrampur Chini, Elara sees adjusted net profit declining 22.2 per cent to Rs 57.20 crore for the June quarter from Rs 73.50 crore in the same quarter last year.The June quarter is likely to be a subdued quarter for the sugar industry due to declining sugar and ethanol volumes on account of lower year-on-year (YoY) quota allocations, Elara Securities said in its preview note. Around 5 per cent growth in sugar price and 10-13 per cent rise in blended distillery realisation would partly offset the loss of lower volume and input cost pressures, it said while preferring Balrampur Chini Mills Ltd over Dwarikesh Sugar Industries Ltd from its tracked sugar stocks.

For the quarter, the domestic sugar sales quota was up 8 per cent YoY at 7.8 million tonnes. Domestic sugar realisation stood at Rs 38.50 per kg (ex-mill), up 5 per cent YoY and largely flat sequentially. Despite the increase in domestic quota, ex-mill sugar prices have been resilient, the brokerage noted.

"The changes in the Ethanol Procurement Policy this year are likely to be a one-off (as a precautionary measure against the risk of low sugar production) and valid between November 2023 and October 2024. Hence, these changes may impact only H2FY24-H1FY25 financials. We expect normalization from H2FY25. We have a neutral view on the sugar sector in the short term, given earnings strain in H1FY25, but we

retain our positive stance in the medium to long term, due to the ethanol blending program," it said.

For Dwarikesh Sugar Industries, Elara expects adjusted net profit to drop 77.40 per cent to Rs 9.2 crore for the June quarter from Rs 40.60 crore in the same quarter last year. It sees sales dropping 33.50 per cent YoY to Rs 379.90 crore from Rs 571.20 crore. The brokerage has 'under review' rating on thus stock.

For Balrampur Chini, Elara sees adjusted net profit declining 22.2 per cent to Rs 57.20 crore for the June quarter from Rs 73.50 crore in the same quarter last year. It sees sales falling 2.7 per cent YoY to Rs 1,351 crore. from Rs 1,387 crore YoY. The brokerage has an 'Accumulate' rating on Balrampur Chini Mills.

Delhi EV policy 2026: Should you buy these premium electric SUVs & MPVs under ₹30 lakh?

Delhi EV policy 2026: Should you buy these premium electric SUVs & MPVs under ₹30 lakh? Big news for commercial petrol, diesel buyers: India lifts emergency curbs on retail sales from July 1

Big news for commercial petrol, diesel buyers: India lifts emergency curbs on retail sales from July 1 ") 'Never seen so many tankers': India's Russian crude imports may hit record high in June

'Never seen so many tankers': India's Russian crude imports may hit record high in June Delhi EV Policy 2026 Explained: What's changing for car, bike and auto buyers

Delhi EV Policy 2026 Explained: What's changing for car, bike and auto buyers space – Prism Hybrid Long-Short Fund") Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space

Why Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space Why Jio BlackRock AMC Is Launching Hybrid Long-Short As It's First SIF

Why Jio BlackRock AMC Is Launching Hybrid Long-Short As It's First SIF Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers

Delhi Unveils ₹15,000 Crore EV Policy: What It Means For Auto Companies And Consumers Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti

Gold, Silver Or Crude? Where Should Investors Bet Now? | Vandana Bharti How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains

How India Strategically Managed LPG & Crude Oil Supplies During West Asia War | K. Surana Explains Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat Pollution

Delhi’s Green Revolution: CM Rekha Gupta Unveils Massive ₹15,000 Crore EV Policy To Combat Pollution Top stocks in news: HDFC Bank, RITES, YES Bank, Concor, Axis Bank, SW Solar, Afcons InfraWhy Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space

Top stocks in news: HDFC Bank, RITES, YES Bank, Concor, Axis Bank, SW Solar, Afcons InfraWhy Jio BlackRock feels hybrid long-short is the perfect fund to launch now as it enters the SIF space Where should investors put their money? PL Wealth CEO has some tips

Where should investors put their money? PL Wealth CEO has some tips  Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday

Axis Bank CFO Puneet Sharma steps down; stock likely in focus on Tuesday Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook

Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook