IndiGo share price: The brokerage highlighted heightened regulatory uncertainty following multiple actions by the DGCA and the Ministry of Civil Aviation.

IndiGo share price: The brokerage highlighted heightened regulatory uncertainty following multiple actions by the DGCA and the Ministry of Civil Aviation.  IndiGo share price: The brokerage highlighted heightened regulatory uncertainty following multiple actions by the DGCA and the Ministry of Civil Aviation.

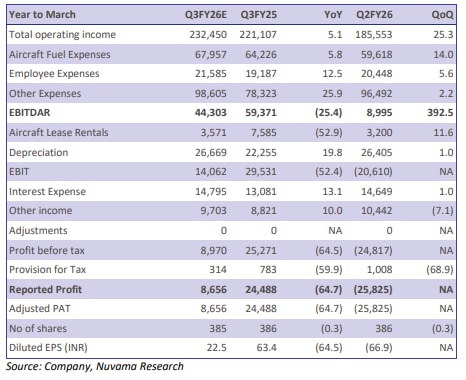

IndiGo share price: The brokerage highlighted heightened regulatory uncertainty following multiple actions by the DGCA and the Ministry of Civil Aviation. Nuvama on Thursday said InterGlobe Aviation (IndiGo) is likely to see one of its weakest quarters, with the peak earnings period turning challenging due to operational disruptions, higher costs and regulatory uncertainty. The brokerage expects IndiGo’s Q3FY26 EbitdaR (Earnings before interest, taxes, depreciation, amortization, and rent) to decline sharply and retained a cautious stance on the stock, citing near-term earnings pressure and the risk of valuation de-rating amid rising competition.

“We expect peak earnings quarter to be one of IndiGo’s worst. IndiGo’s Q3FY26E EbitdaR is expected to fall 25 per cent year on year due to one of the airline’s worst operational disruptions, while the outcome of various regulatory actions remains uncertain and could have both actual and implicit implications,” Nuvama said.

Adjusted profit is seen falling 64.7 per cent YoY on a 5.1 per cent rise in total operating income. It suggested a target price of Rs 5,069 on the IndiGo stock.

Nuvama said Q3FY26 EbitdaR is expected to decline 25 per cent YoY, driven by a 4 per cent YoY fall in yields and a 26 per cent YoY increase in operating expenses. The rise in costs was largely due to forex losses of about Rs 1,100 crore and FDTL-related disruption costs of around Rs 830 crore incurred in December 2025, Nuvama said.

These included compensation vouchers, accommodation and refreshments provided to affected passengers. Earnings were partly supported by around 10 per cent year-on-year growth in available seat kilometres, although this was muted and significantly lower than earlier expectations of high-teens growth.

The brokerage highlighted heightened regulatory uncertainty following multiple actions by the DGCA and the Ministry of Civil Aviation.

These included the formation of a committee to examine the root causes of operational issues and suggest preventive measures, a 10 per cent cut in IndiGo’s winter schedule, and show-cause notices issued to senior management. Nuvama said potential outcomes could range from further schedule cuts and monetary penalties to mandated changes in internal processes.

“Various regulatory actions have been taken against IndiGo, with the outcome and impact currently uncertain. Moreover, there has been no extension of IndiGo-specific relaxations under certain FDTL norms, which raises the risk of a re-occurrence of operational disruption and adds to concerns around growth and competition,” the brokerage said.

Nuvama said revised FDTL norms had materially affected IndiGo’s operations, including an increase in weekly rest requirements from 36 hours to 48 hours, expansion of the night-duty window to midnight to 6 am, limits on consecutive night duties and a reduction in permissible night landings. It said inadequate planning led to a significant pilot shortage under Phase II of the revised norms that came into effect from November 1, 2025.

While the DGCA later allowed pilot leave to count towards the 48-hour rest requirement for all airlines and temporarily relaxed night-duty restrictions for IndiGo’s A320 fleet until February 2026, the brokerage viewed this relief as interim.

On outlook and valuation, Nuvama said the near-term environment remained challenging due to operational disruptions, the 10 per cent capacity cut and rising costs linked to fresh pilot and crew hiring.

It added that premium valuation multiples were vulnerable to de-rating amid regulatory overhang and competition-related concerns. Nuvama retained its HOLD rating, noting that at the current market price, InterGlobe Aviation was trading at about 17 times FY27 estimated earnings per share.

India hikes gold, silver import duty to 15% to curb imports, but industry warns, 'grey marketers may...'

India hikes gold, silver import duty to 15% to curb imports, but industry warns, 'grey marketers may...' Amid austerity push, PM Modi orders 50% reduction in convoy size

Amid austerity push, PM Modi orders 50% reduction in convoy size") Gold, silver customs duty hikes impact: Titan Company, Kalyan Jewellers, Senco Gold among stocks in focus today

Gold, silver customs duty hikes impact: Titan Company, Kalyan Jewellers, Senco Gold among stocks in focus today Buying a house with your spouse? Here’s how it can reduce your tax bill

Buying a house with your spouse? Here’s how it can reduce your tax bill Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 10 points; key levels to watch

Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 10 points; key levels to watch GADGET GARAGE | The Tech Gear Show EP 2 | IZI Brephos, Oben RORR EVO | Business Today

GADGET GARAGE | The Tech Gear Show EP 2 | IZI Brephos, Oben RORR EVO | Business Today Vijay Sales – Building An Omnichannel Retail Powerhouse

Vijay Sales – Building An Omnichannel Retail Powerhouse Rupee Crashes To All-Time Low Amid Iran-US Tensions | Oil Shock Hits Markets

Rupee Crashes To All-Time Low Amid Iran-US Tensions | Oil Shock Hits Markets "We Knew It All Along": MEA Reacts To Reports Of China Backing Pak During Ops Sindoor

"We Knew It All Along": MEA Reacts To Reports Of China Backing Pak During Ops Sindoor Market Crash Deepens! IT Stocks Sink, Crude Surges | Nischal Maheshwari

Market Crash Deepens! IT Stocks Sink, Crude Surges | Nischal Maheshwari MSCI Rejig Impact: 3 stocks may see $1.2 bn inflows; Adani Power, Trent, BPCL among shares in focus

MSCI Rejig Impact: 3 stocks may see $1.2 bn inflows; Adani Power, Trent, BPCL among shares in focus MSCI rejig: Adani Energy, Nalco, MCX shares in; RVNL, Kalyan, Hyundai, SBI Card out Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 10 points; key levels to watchGold, silver customs duty hikes impact: Titan Company, Kalyan Jewellers, Senco Gold among stocks in focus today

MSCI rejig: Adani Energy, Nalco, MCX shares in; RVNL, Kalyan, Hyundai, SBI Card out Nifty, Sensex, Nifty Bank outlook for today: GIFT Nifty up 10 points; key levels to watchGold, silver customs duty hikes impact: Titan Company, Kalyan Jewellers, Senco Gold among stocks in focus today Top stocks in news: Dr Reddy's, Tata Power, Voda Idea, RVNL, Dixon, MTAR, Sagility, Nazara

Top stocks in news: Dr Reddy's, Tata Power, Voda Idea, RVNL, Dixon, MTAR, Sagility, Nazara