The short-term rally in Polycab stock is powered by a recovery in the broader market from US-Iran war shock and a stellar set of Q4 and FY26 earnings.

The short-term rally in Polycab stock is powered by a recovery in the broader market from US-Iran war shock and a stellar set of Q4 and FY26 earnings.  The short-term rally in Polycab stock is powered by a recovery in the broader market from US-Iran war shock and a stellar set of Q4 and FY26 earnings.

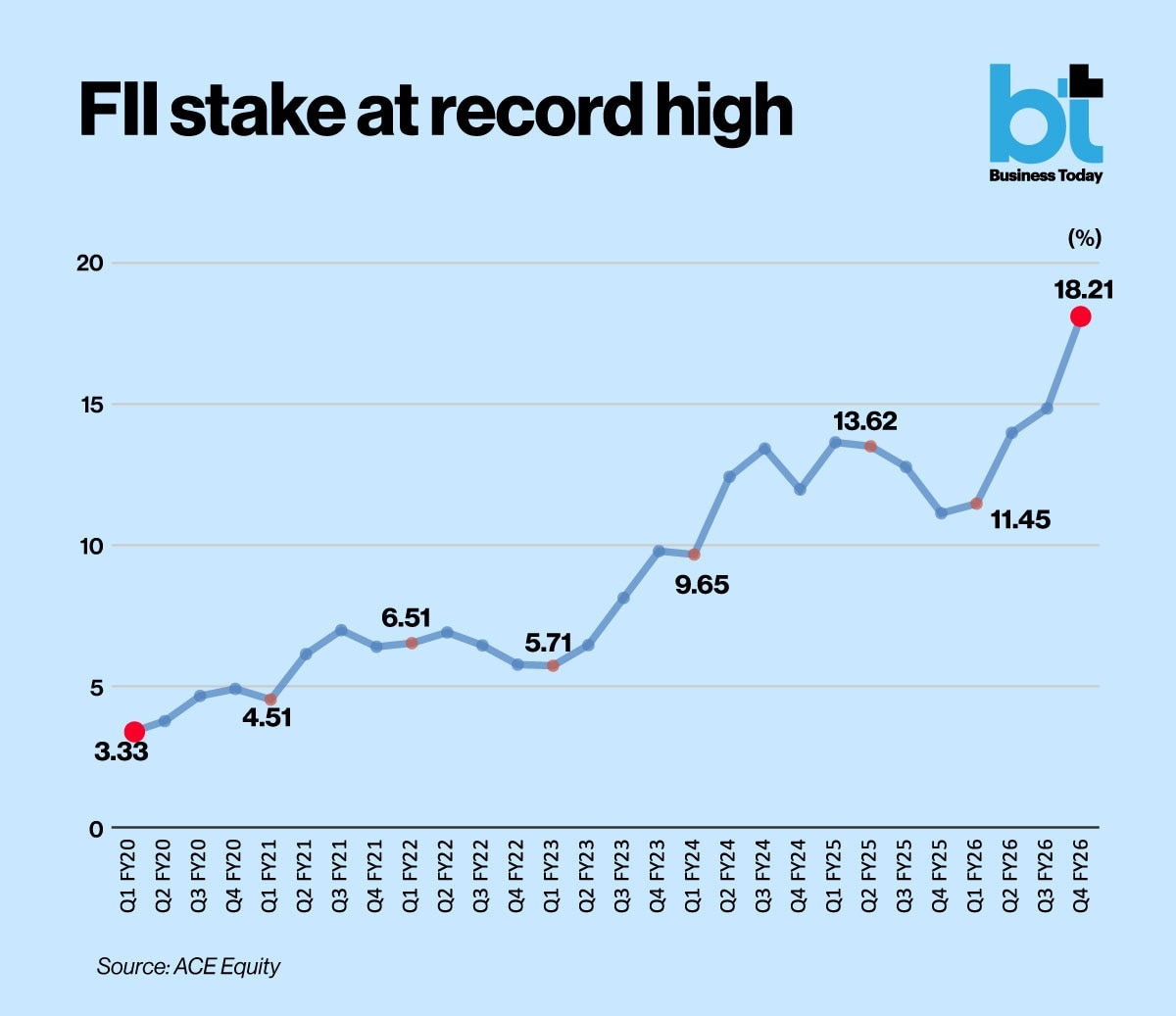

The short-term rally in Polycab stock is powered by a recovery in the broader market from US-Iran war shock and a stellar set of Q4 and FY26 earnings. Shares of market leader Polycab India saw mild profit-booking from its record high reached last week. The fast-moving electrical goods (FMEG) player logged the highest ever foreign institutional investors (FII) holding in the March 2026 quarter. The FII holding in Q4 rose to 18.2% from 14.8% in the December 2025 quarter. In Q2 of the previous fiscal, FII stake in Polycab rose to 14% against 11.5% in Q1 of FY26.

Usually, high FII holding in a stock signals strong confidence from international investors, which can drive liquidity and price stability.

Meanwhile, the stock of the FMEG multibagger also hit a record high last week. It touched a high of Rs 10,128 on June 22, 2026. The short-term rally in Polycab stock is powered by a recovery in the broader market from US-Iran war shock and a stellar set of Q4 and FY26 earnings.

Polycab logged its highest-ever quarterly revenue of Rs 8,864 crore in Q4 FY26, clocking 26.9% YoY growth compared to Rs 6,986 crore in the year-ago quarter. The company’s cables and wires (C&W) segment, which contributes about 87% of the total revenue, clocked around 30% YoY growth led by healthy domestic demand, institutional orders, and retail expansion.

Consolidated EBITDA zoomed 13.3 per cent to Rs 1,160 crore, while adjusted net profit rose 6.3 per cent Y-o-Y to Rs 770 crore.

In FY26, the company clocked its best annual performance to date. Revenue surged by 29% year-on-year, reaching Rs 28,884 crore, while EBITDA climbed 35% to Rs 4,006 crore. Profit after tax rose 32% to Rs 2,708 crore, with net profit margins improving to 9.4%.

Meanwhile, in the current session, the FMEG stock ended 2.69% higher at Rs 9790 against the previous close of Rs 9533.80.

Total 0.30 lakh shares of the firm changed hands amounting to a turnover of Rs 29.30 crore. Market cap of the firm stood at Rs 1.47 lakh crore in the current session.

The FMEG stock is neither overbought nor oversold on charts, indicates its RSI of 50.7.

However, the multibagger stock has gained 53% from 52-week low of Rs 6389.50 on June 26, last year.

Polycab share price targets

Brokerage Anand Rathi expects the stock to hit a price target of Rs 10,351 against the earlier Rs 9073 earlier.

According to the brokerage, Polycab is well-placed to benefit from structural tailwinds including domestic electrification, export opportunities and global grid upgradation demand. With improving FMEG profitability, strong execution and sustained growth visibility, the outlook remains positive. The brokerage has a BUY rating on the stock, valuing it at 38.5x FY28e EPS of Rs269.

"Factoring in the strong Q4 performance, we expect revenue/earnings to clock 22/23% CAGR over FY26-28e. We retain BUY rating on the stock with a TP of Rs 10,351 (from Rs 9,073 earlier, valuing it at 38.5 times FY28e EPS of Rs269."

It mentioned (a) Lower government spending on infra; (b) higher-than-expected investment in capacity and branding; (c) volatility in commodity prices; and (d) intense competition as key risks for the assumptions.

Jefferies has upgraded its target to Rs 10,920 with a Buy rating following a strong rally, citing market share gains, data center opportunities, and a healthy order pipeline.

Polycab India logged its sharpest single-year market share gain in recent history during the last fiscal. Polycab India's organised Wires and Cables market share rose 300-400 bps YoY to 30-31% against 26-27% in FY25. The growth in market share came on the back an 18% domestic volume growth against an industry growth of 11%.

Foreign brokerage Citi has assigned a price target of Rs 10,500 per share and maintained its buy rating on the stock.

The brokerage said that margins in the cables and wires business are expected to remain near the upper end of the company's guided 12-14% range.

Following a meeting with Polycab's management, Citi said domestic demand has recovered after a relatively weak March quarter, which had been hit by geopolitical uncertainties in West Asia. According to the brokerage, management highlighted that secondary sales began improving from early April, while channel inventories have now normalized, indicating healthier demand conditions.

The company also reported encouraging business momentum during the first two months of the quarter, with volume growth in the mid- to high-single digits across April and May. This performance came despite a challenging base, as sales volumes during the corresponding period last year had surged by more than 25%.

To mitigate the impact of rising input costs and the depreciation of the Indian rupee, Polycab implemented another round of price hikes of approximately 8-10% during the first quarter. The company expects these pricing actions to help protect margins amid continued raw material cost pressures.

") 'Never seen so many tankers': India's Russian crude imports may hit record high in June

'Never seen so many tankers': India's Russian crude imports may hit record high in June Delhi EV policy approved: Road tax exempted for cars over ₹30 lakh; ₹50,000 subsidies for EV buyers

Delhi EV policy approved: Road tax exempted for cars over ₹30 lakh; ₹50,000 subsidies for EV buyers 9 shares may enter AMFI largecap list: BSE, Vodafone Idea, Groww, BHEL among probables

9 shares may enter AMFI largecap list: BSE, Vodafone Idea, Groww, BHEL among probables Persistent Systems shares tumble nearly 12%; is this a buying opportunity?

Persistent Systems shares tumble nearly 12%; is this a buying opportunity? What is loop engineering? The AI trend replacing prompt engineering

What is loop engineering? The AI trend replacing prompt engineering Market LIVE: What's Next For Nifty? Anshul Saigal Decodes The Market Strategy

Market LIVE: What's Next For Nifty? Anshul Saigal Decodes The Market Strategy Why Gold Prices Are Falling Despite U.S.-Iran Tensions And Rising Oil Prices

Why Gold Prices Are Falling Despite U.S.-Iran Tensions And Rising Oil Prices LIVE Daily Calls: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today

LIVE Daily Calls: Ask Your STOCK MARKET TODAY QUERIES | Market Update LIVE | Share Market News Today LIVE What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

LIVE What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Earnings Outlook: Anshul Saigal On Q1FY27 Earnings And Best Bets

Earnings Outlook: Anshul Saigal On Q1FY27 Earnings And Best Bets Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook

Apollo Hospitals, Medanta, Healthcare Global, Max Healthcare, Artemis Medicare: Check target prices, outlook Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside

Polycab: Amid record FII buying, shares at all-time high but brokerages expect more upside Sensex, Nifty close in the red: Why markets fell and what to expect next

Sensex, Nifty close in the red: Why markets fell and what to expect next GIFT Nifty logs record open interest, contracts on June 25Persistent Systems shares tumble nearly 12%; is this a buying opportunity?

GIFT Nifty logs record open interest, contracts on June 25Persistent Systems shares tumble nearly 12%; is this a buying opportunity?