April 2026 had three market holidays, each adversely affecting NSE.April 2026 had three market holidays, each adversely affecting NSE.

April 2026 had three market holidays, each adversely affecting NSE.April 2026 had three market holidays, each adversely affecting NSE.Every trading activity, particularly in the institutional segment in the equity derivatives market, depends on liquidity and seeks deeper markets. The National Stock Exchange of India (NSE) has maintained structural dominance in trading activity (premium turnover), liquidity, tighter spreads, and higher investor participation over decades, making it a preferred destination for the institutional segment. Recent commentary suggesting that NSE lost meaningful equity derivatives market share in April 2026 is far from the factual position.

The data, when read correctly and interpreted precisely using the right metric, tells a very different story altogether.

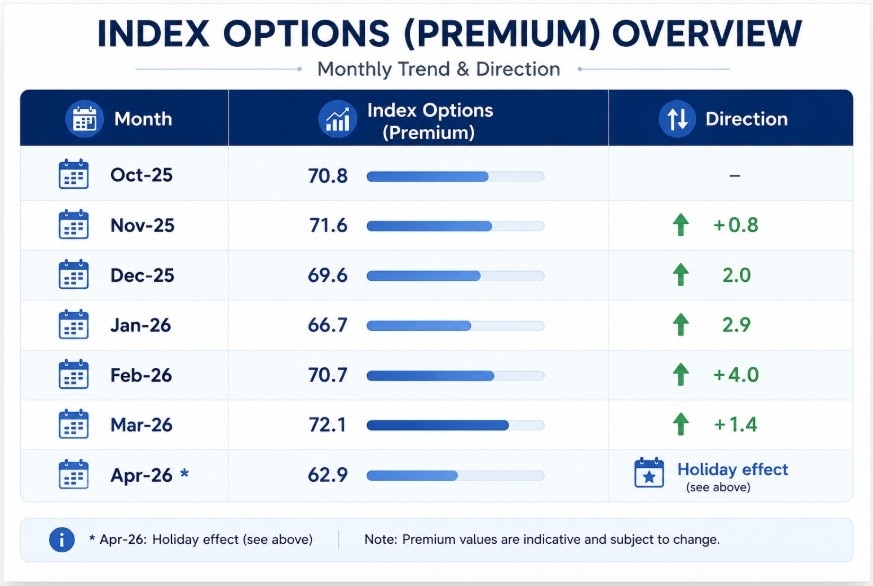

1. Market Share Was Rising Consistently from January to March 2026

On premium turnover — the correct measure of options market activity — NSE's index options market share improved steadily across the three months prior to April 2026, as shown below:

Index options market share moved from 66.7% in January to 72.1% in March — a clear gain of 540 basis points in three months. This is clearly the underlying trend.

2. The April Figure Is a Distortion, Explained Below

April 2026 had three market holidays, each adversely affecting NSE.

It is a well-known fact that weekly expiry sessions are the highest-volume sessions in any given week. For NSE, Nifty 50 and Nifty Bank contracts expire every Tuesday, unlike BSE, where Sensex and Bankex contracts expire every Thursday.

Critically, none of the three holidays fell on a Thursday. BSE's Sensex and Bankex expiry cycles ran uninterrupted across all four weeks of April. NSE operated only two weeks of expiry cycles. With half its expiry sessions lost, a decline in NSE's monthly market share figure becomes a mechanical outcome — not a reflection of any competitive or market preference shift. In cricketing terms, NSE was deprived of middle-overs consolidation as well as the advantage of accelerating in the death overs.

3. NSE's Market Share Has Been Consistently Growing, Not Declining

The January–March 2026 data establishes a clear recovery trend from a trough in late 2025. The table below places this in context:

April 2026 excluded from trend analysis given the holiday-driven structural distortion described in Point 2.

The February and March data points confirm a genuine recovery in market share. The narrative of a declining NSE is not supported by the underlying data.

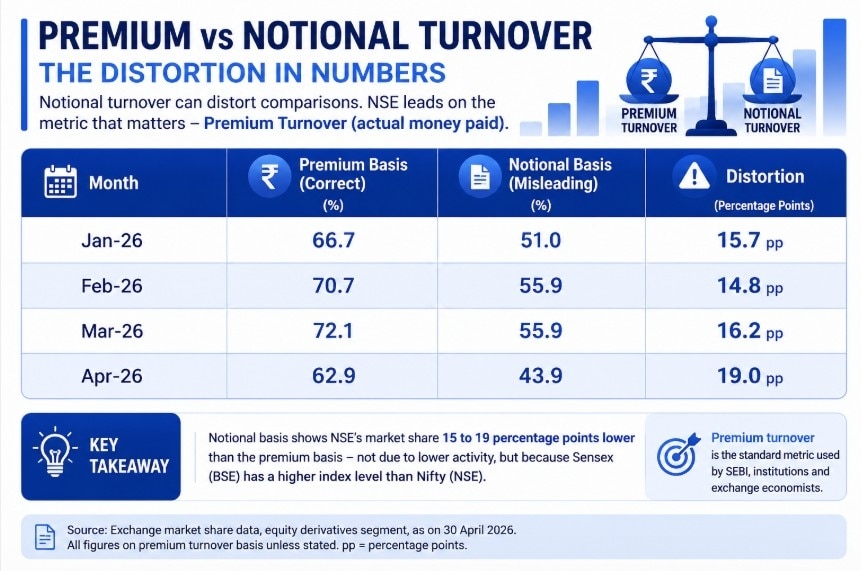

4. Notional Turnover Is Not the Right Metric

Some market participants have chosen to present exchange market share using notional turnover for options — a figure calculated by multiplying contract volumes by the underlying index level rather than by the premium actually paid. This is not an appropriate measure.

Options premium is what participants actually pay and receive. It reflects the economic size of the trade — the risk transferred and the capital at stake. Notional value is the face value of the underlying exposure. Because Sensex trades at a higher absolute index level than Nifty, any notional comparison will mechanically inflate BSE's share, independent of actual liquidity or market activity.

The notional basis produces a figure 15–19 percentage points lower than the premium basis — not because of any difference in actual market activity, but because of index price-level differences. Premium turnover is the standard measure used by SEBI, institutional market participants, and exchange economists. Presenting notional turnover as the primary metric is a selective analytical choice that does not reflect competitive reality.

Reality: NSE's equity derivatives market share was on a consistent upward trajectory from January to March 2026, rising 540 basis points in index options premium share. The April 2026 dip is explained entirely by the loss of two Tuesday expiry sessions to market holidays, with no equivalent impact on competing exchange expiry schedules. The underlying trend remains intact. Framing this period using notional turnover rather than premium turnover further distorts the picture and is not an analytically defensible choice.

Notional vs Premium Turnover: BSE was ahead for a brief period in notional turnover (contract value × underlying index level), which can distort comparisons by a significant margin. NSE still dominates premium turnover (actual money paid for options contracts), the metric regulators and institutions use.

Source: Exchange market share data, equity derivatives segment, as of 30 April 2026. All figures are on a premium turnover basis unless stated. pp = percentage points.

Uday Tardalkar is Chairperson and Independent Director at RoseMerc Limited, with over three decades of experience in the financial services industry spanning securities, broking, custodial services and asset management.

'Name any one vehicle which...': Nitin Gadkari's dare to critics amid E20 fears

'Name any one vehicle which...': Nitin Gadkari's dare to critics amid E20 fears 'I came to Mumbai with just a baksa and a dream to make it': Vedanta's Anil Agarwal

'I came to Mumbai with just a baksa and a dream to make it': Vedanta's Anil Agarwal Meet IMF's new Chief Economist Silvana Tenreyro, who takes charge amid global uncertainty

Meet IMF's new Chief Economist Silvana Tenreyro, who takes charge amid global uncertainty Market crash in numbers: Sensex tanks 1,100 pts, Rs 5 lakh cr investor wealth gone and more

Market crash in numbers: Sensex tanks 1,100 pts, Rs 5 lakh cr investor wealth gone and more  Oil prices soar, Hormuz shipping risk raised to severe as US strikes Iran

Oil prices soar, Hormuz shipping risk raised to severe as US strikes Iran Reasons Why Energy Stocks Could Be The Next Big Market Bet: Ajay Bagga Explains

Reasons Why Energy Stocks Could Be The Next Big Market Bet: Ajay Bagga Explains Bank Stocks In Focus: Ajay Bagga Shares Outlook On FPIs, Fed & Credit Growth

Bank Stocks In Focus: Ajay Bagga Shares Outlook On FPIs, Fed & Credit Growth Q1 Earnings Season: Which Sectors Could Surprise & Which May Disappoint?

Q1 Earnings Season: Which Sectors Could Surprise & Which May Disappoint? Did Trump's Iran Gamble Fail? How Khamenei's Death Changed Tehran's Power Structure

Did Trump's Iran Gamble Fail? How Khamenei's Death Changed Tehran's Power Structure India At UN: AI Must Empower Global South, Not Deepen Inequality, Says Kirti Vardhan SinghMarket crash in numbers: Sensex tanks 1,100 pts, Rs 5 lakh cr investor wealth gone and more

India At UN: AI Must Empower Global South, Not Deepen Inequality, Says Kirti Vardhan SinghMarket crash in numbers: Sensex tanks 1,100 pts, Rs 5 lakh cr investor wealth gone and more  YES Bank, Bandhan, RBL, IDFC, HDFC Bank, KMB, SBI, BOB: Target prices ahead of Q1 results

YES Bank, Bandhan, RBL, IDFC, HDFC Bank, KMB, SBI, BOB: Target prices ahead of Q1 results INOX India shares jump nearly 6% today; here is why

INOX India shares jump nearly 6% today; here is why Banks, defence, auto to shine; IT may lag: SBICAP Securities' MD on Q1, markets & FII flow

Banks, defence, auto to shine; IT may lag: SBICAP Securities' MD on Q1, markets & FII flow Swiggy share price target: JM cites Eternal case on global index weights

Swiggy share price target: JM cites Eternal case on global index weights