The impact of the rate hike is much more significant if you compare the tenure of your loan

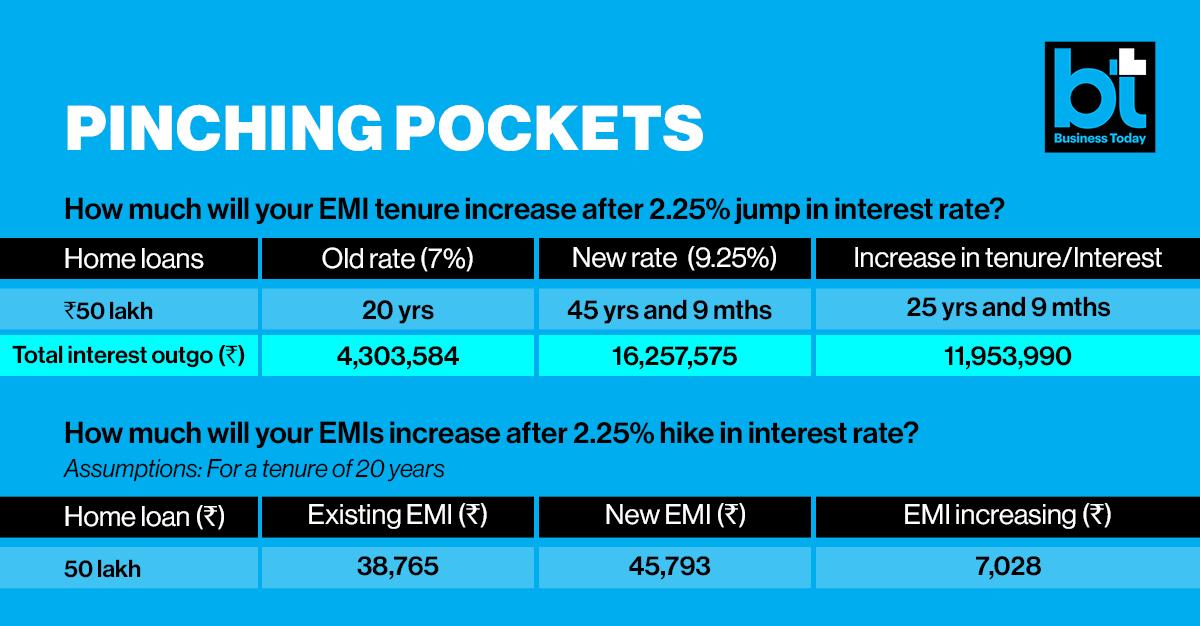

The impact of the rate hike is much more significant if you compare the tenure of your loanFollowing the rise in the repo rate, your home loan interest rate has risen by 2.25 percentage points since May 2022. The jump might not have pinched you if you continued paying the same amount of EMI without checking the revised tenure of your loan. But the impact of the rate hike is much more significant if you compare the tenure of your loan.

Consider this: Your 20-year loan of Rs 50 lakh at 7 per cent has now turned into a loan of 45 years and 9 months, a jump of 25 years and 9 months. The calculation is based on the assumption that the rate got revised to 9.25 per cent after 6 months of taking the loan.

In such a scenario when home loan rates have crossed the mark of 9 per cent, the concerning point is the tenure of the home loan that has already crossed the working age of 60 years for many borrowers. Given the steep rise in the tenure of loans, which is the default option for banks when the lending rates rise, it is important that you are aware of its implications in the long run.

What is better to increase tenure or EMI? If you are already living on a tight budget it is better to increase your tenure without hurting your spending and savings.

But if you have a surplus then you have three options: First to increase your EMI, second to pre-pay with the surplus amount and third to invest the surplus amount somewhere else where the return is higher considering a home loan is the cheapest loan and comes along with tax benefits. Having said that if you choose to increase the tenure make sure you invest the extra amount for generating higher returns.

For example, If you have Rs 5 lakh, and on average, based on your past investment experience, you can get a 12 per cent return on the amount invested. It makes more sense to invest Rs 5 lakh for that return, and continue the home loan with revised tenure.

“If a borrower chooses to increase the repayment tenure of the loan, they can save the extra amount and use it for repaying another loan or can invest the same for a higher return which will balance out the increased interest burden,” said V Swaminathan, Executive Chairman, Andromeda loans and Apnapaisa.

Also Read: SBI's home loan rates to go up from today. New customers can still avail concessions. Know how

India's next 'eyes in the sky': Adani-DRDO seal landmark AEW&C Mk-II deal for IAF

India's next 'eyes in the sky': Adani-DRDO seal landmark AEW&C Mk-II deal for IAF Indian govt orders GitHub to block access of Jack Dorsey's messaging app, Bitchat amid CJP protest

Indian govt orders GitHub to block access of Jack Dorsey's messaging app, Bitchat amid CJP protest 'My partner is half-Indian': Elon Musk rejects racism claims; why his son is named after Chandrasekhar

'My partner is half-Indian': Elon Musk rejects racism claims; why his son is named after Chandrasekhar 'Ad hocism has troubled us for years': Amid CJP protest, Supreme Court to monitor NEET paper leak reforms

'Ad hocism has troubled us for years': Amid CJP protest, Supreme Court to monitor NEET paper leak reforms 'Non-negotiable': CJP holds firm on Pradhan's resignation as government seeks time till Saturday

'Non-negotiable': CJP holds firm on Pradhan's resignation as government seeks time till Saturday PM Modi Announces Fast-Track Courts Amid NEET Row, CJP Continues Demand For Pradhan's Resignation

PM Modi Announces Fast-Track Courts Amid NEET Row, CJP Continues Demand For Pradhan's Resignation Sona Comstar Q1 Results | Profit Jumps 47%, EV Business Drives Record Revenue

Sona Comstar Q1 Results | Profit Jumps 47%, EV Business Drives Record Revenue IIT Madras Incubated Startup Unveils e200X: World's Most Compact Passenger eVTOL Air Taxi

IIT Madras Incubated Startup Unveils e200X: World's Most Compact Passenger eVTOL Air Taxi Fractal Q1 Results | CEO Srikanth Velamakanni On 92% Profit Jump, AI Demand & Growth Outlook

Fractal Q1 Results | CEO Srikanth Velamakanni On 92% Profit Jump, AI Demand & Growth Outlook Stop Predicting Markets! Focus On These Long-Term Investment Themes

Stop Predicting Markets! Focus On These Long-Term Investment Themes PVR Inox shares jump 6% after Q1; Nuvama cites continued debt reduction

PVR Inox shares jump 6% after Q1; Nuvama cites continued debt reduction Adani Energy wins Rs 8,500 crore Andhra Pradesh order; stock reacts

Adani Energy wins Rs 8,500 crore Andhra Pradesh order; stock reacts Hindustan Zinc: Q1 profit jumps 145% to Rs 5,469 crore; names ex-SAIL chief Amarendu Prakash as CEO

Hindustan Zinc: Q1 profit jumps 145% to Rs 5,469 crore; names ex-SAIL chief Amarendu Prakash as CEO NBCC share price target: Analyst says watch out for Rs 128 breakout level before fresh buying

NBCC share price target: Analyst says watch out for Rs 128 breakout level before fresh buying Ambuja Cements stock: Analyst gives buy call; suggests stop loss, price target

Ambuja Cements stock: Analyst gives buy call; suggests stop loss, price target  Vijay’s last film creates a storm: Fans turn theatres into celebration zonesPM Modi Announces Fast-Track Courts Amid NEET Row, CJP Continues Demand For Pradhan's Resignation

Vijay’s last film creates a storm: Fans turn theatres into celebration zonesPM Modi Announces Fast-Track Courts Amid NEET Row, CJP Continues Demand For Pradhan's Resignation Vijay Sethupathi, Simran join Regal Jewellers as brand ambassadors

Vijay Sethupathi, Simran join Regal Jewellers as brand ambassadors India’s medal challenge begins: Why Glasgow 2026 will be a different battle

India’s medal challenge begins: Why Glasgow 2026 will be a different battle Your Prime Video is about to change: Jeff Bezos wants AI to decide what you watch next

Your Prime Video is about to change: Jeff Bezos wants AI to decide what you watch next