Industry data shows scheduled bank FD rates currently range from 2.5% to 8% for regular depositors.Industry data shows scheduled bank FD rates currently range from 2.5% to 8% for regular depositors.

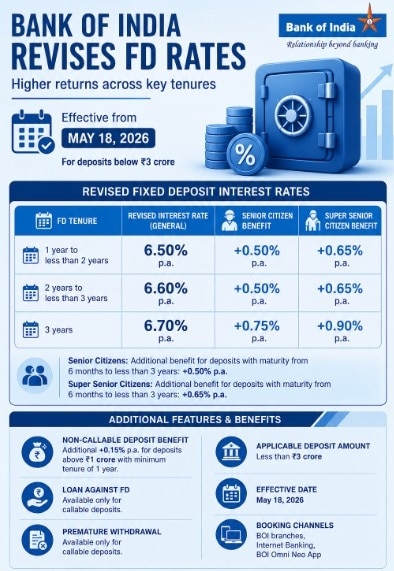

Industry data shows scheduled bank FD rates currently range from 2.5% to 8% for regular depositors.Industry data shows scheduled bank FD rates currently range from 2.5% to 8% for regular depositors.State-owned Bank of India (BOI) has revised fixed deposit (FD) interest rates on select medium- and long-term deposits, offering higher returns to customers seeking stable and guaranteed income options. The revised FD rates, applicable on retail fixed deposits below ₹3 crore, came into effect from May 18, 2026, and are expected to strengthen the bank’s competitiveness in an increasingly crowded deposit market.

The revision comes at a time when banks are actively adjusting deposit offerings to attract retail savings amid rising competition from private lenders, small finance banks, and non-banking financial companies (NBFCs), many of which continue to offer higher rates.

Bank of India: Revised FD rates

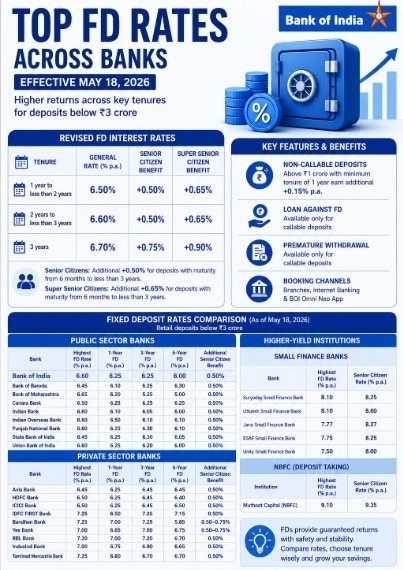

Under the revised structure, Bank of India has increased rates across key one- to three-year maturity buckets. Deposits with tenure between one year and less than two years will now earn 6.5% annually. Deposits maturing between two years and less than three years will fetch 6.6%, while three-year fixed deposits will now provide 6.7% per annum.

MUST READ: Special FDs vs regular fixed deposits: Which option makes more sense for investors?

The revised rates make BOI one of the stronger contenders among public sector banks in the medium-term FD category.

The lender has also retained additional benefits for senior citizens and super senior citizens. Senior citizens will continue receiving an additional 50 basis points on deposits with maturity from six months to less than three years, while super senior citizens will receive an additional 65 basis points.

For deposits with maturity of three years and above, senior citizens will get an additional 75 basis points and super senior citizens an additional 90 basis points over the applicable rate.

Additional benefits

BOI has also announced extra incentives for high-value depositors. Non-callable deposits above ₹1 crore with a minimum tenure of one year will earn an additional 15 basis points over the applicable rate. However, such deposits come with restrictions.

The bank clarified that facilities such as loans against fixed deposits and premature withdrawal options will be available only on callable deposits.

MUST READ: Foreign Bank FD rates in India: How do they stack up against public and private banks?

Customers can open these deposits through BOI branches, internet banking channels, and the BOI Omni Neo mobile application.

Why FD rates matter for investors

Fixed deposits continue to remain a preferred investment choice for conservative savers because they offer assured returns and insulation from market volatility. Unlike market-linked products, the interest rate agreed upon at the time of booking remains fixed for the duration of the deposit.

The final return on an FD, however, depends on several variables. Apart from the headline interest rate, returns are influenced by deposit tenure, payout option, compounding frequency, and customer category such as regular depositor or senior citizen.

For deposits shorter than six months, simple interest generally applies, while longer-duration deposits typically benefit from quarterly compounding.

MUST READ: What are India’s HNIs buying now -- equities, gold or alternative assets?

How BOI compares with other banks

While BOI's revised rates strengthen its standing among public sector lenders, competition across the broader FD market remains intense. Industry data shows scheduled bank FD rates currently range from 2.5% to 8% for regular depositors.

Among public sector peers, Punjab National Bank and Indian Bank offer rates up to 6.6%, while State Bank of India offers up to 6.45%.

Private and small finance banks continue to lead on returns. Bandhan Bank and IDFC FIRST Bank offer rates as high as 7.25%, while Suryoday Small Finance Bank and Utkarsh Small Finance Bank are offering up to 8.1%. NBFCs remain at the top end, with Muthoot Capital offering rates reaching 9.1%.

As banks continue competing for deposits, investors may increasingly compare not only returns but also liquidity, withdrawal flexibility, and institutional credibility before locking in their savings.

") NSE IPO vs Reliance Jio IPO: Issue size compared

NSE IPO vs Reliance Jio IPO: Issue size compared RBI extends Keki Mistry's tenure as HDFC Bank's interim chairman by three months

RBI extends Keki Mistry's tenure as HDFC Bank's interim chairman by three months Diesel price surge: Highway developers to get compensation from centre

Diesel price surge: Highway developers to get compensation from centre 'Shows how nations can defeat terror networks': Israeli envoy praises Dhurandhar

'Shows how nations can defeat terror networks': Israeli envoy praises Dhurandhar 'India AI Summit was extremely disorganised': Dario Amodei on viral stage moment with Sam Altman

'India AI Summit was extremely disorganised': Dario Amodei on viral stage moment with Sam Altman Which Sectors Worked Best For BOI Mutual Fund? Alok Singh Reveals The Top Performers

Which Sectors Worked Best For BOI Mutual Fund? Alok Singh Reveals The Top Performers Indian Stock Market News: Why Pharma, Hospitals And Diagnostics Remain Long-Term Compounders

Indian Stock Market News: Why Pharma, Hospitals And Diagnostics Remain Long-Term Compounders Why Expert Believes AI Could Trigger The Next Growth Wave For Indian IT Stock

Why Expert Believes AI Could Trigger The Next Growth Wave For Indian IT Stock Falling Oil Prices And A Stronger Rupee: Experts See A Big Opportunity For India

Falling Oil Prices And A Stronger Rupee: Experts See A Big Opportunity For India "India Will Write The Last Word On AI": Piyush Goyal's Bold Tech Vision From France

"India Will Write The Last Word On AI": Piyush Goyal's Bold Tech Vision From France Nifty rises 1,000 pts in six days, trend reversal or more gains ahead?

Nifty rises 1,000 pts in six days, trend reversal or more gains ahead? NSE IPO: Exchange likely to raise Rs 30,000 crore— Are unlisted shares trading at premium?NSE IPO vs Reliance Jio IPO: Issue size compared

NSE IPO: Exchange likely to raise Rs 30,000 crore— Are unlisted shares trading at premium?NSE IPO vs Reliance Jio IPO: Issue size compared Jaiprakash Associates shares delisted from BSE, NSE; key details

Jaiprakash Associates shares delisted from BSE, NSE; key details Up 18% in a month! Falling crude isn't the only tailwind for this multibagger stock

Up 18% in a month! Falling crude isn't the only tailwind for this multibagger stock