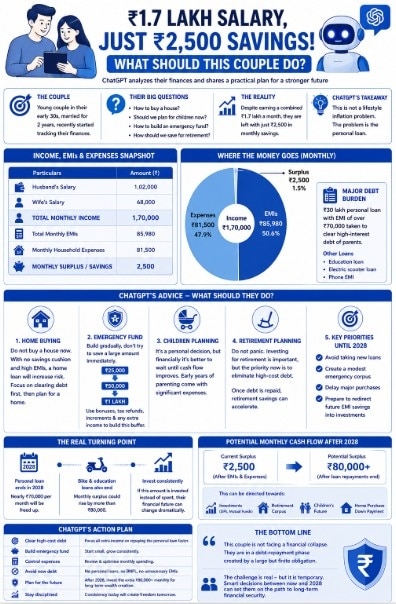

According to ChatGPT, the most important observation is that this is not a case of reckless spending, but it is the personal loan.

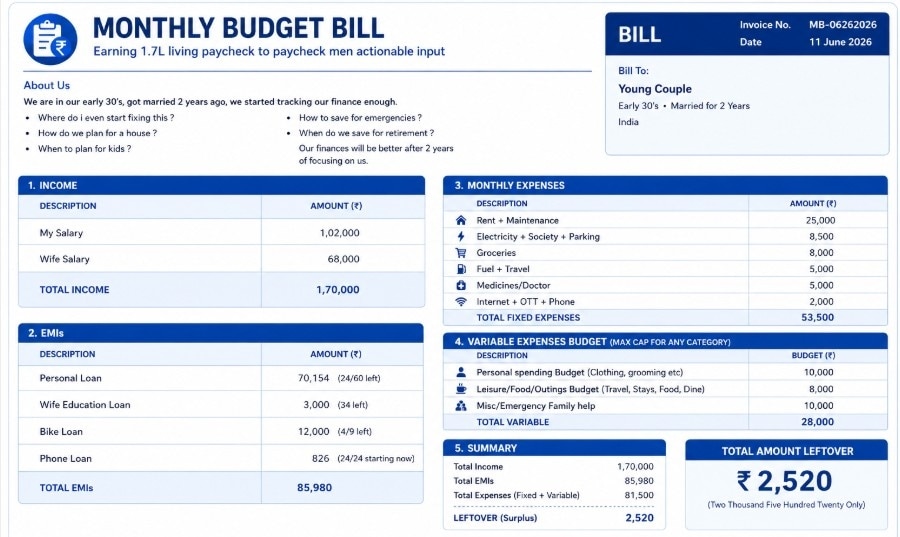

According to ChatGPT, the most important observation is that this is not a case of reckless spending, but it is the personal loan.A young married couple in their early 30s recently turned to ChatGPT with a concern that many urban Indian households may find familiar. Despite earning a combined monthly income of ₹1.7 lakh, they are left with just ₹2,500 in monthly surplus after accounting for loan repayments and household expenses.

The couple, married for two years, said they recently began tracking their finances and were shocked to discover how little they were saving. Their biggest questions revolved around buying a home, planning for children, building an emergency fund, and saving for retirement.

So, what would ChatGPT advise?

The problem

The couple's combined monthly income consists of ₹1.02 lakh from the husband and ₹68,000 from the wife. However, nearly half of that income is consumed by debt obligations.

Their total EMIs amount to ₹85,980 per month, including a personal loan, education loan, electric scooter loan, and phone EMI.

The biggest burden is a ₹30 lakh personal loan, which the husband took to consolidate high-interest debt accumulated by his parents through local lenders charging around 18% interest. The loan carries a monthly EMI of more than ₹70,000 and will continue until 2028.

In addition to EMIs, the couple spends around ₹81,500 per month on rent, utilities, groceries, commuting, healthcare, leisure, and family support.

After all expenses are paid, only about ₹2,500 remains.

Lifestyle inflation

According to ChatGPT, the most important observation is that this is not a case of reckless spending.

The couple's finances are constrained primarily because of one large debt obligation. While their cash flow appears stretched today, the situation is fundamentally different from households that consistently overspend on discretionary purchases.

"The problem isn't spending—it's the personal loan," ChatGPT noted.

Buying a house

One of the couple's key concerns was home ownership. ChatGPT's view was clear: purchasing a house now would likely worsen their financial situation.

With virtually no savings cushion and a significant EMI burden already in place, adding a home loan would increase financial risk. Instead, the couple should focus on stabilising their finances and repaying existing debt before considering a property purchase.

Emergency Fund

Financial experts often recommend building six to twelve months of expenses as an emergency corpus. However, ChatGPT suggested a more practical approach.

Rather than targeting a large emergency fund immediately, the couple should start with smaller milestones—₹25,000, then ₹50,000, and eventually ₹1 lakh. Bonuses, tax refunds, salary increments, or any unexpected inflows could be directed toward creating this buffer.

The objective is simple: avoid taking on new debt when unexpected expenses arise.

Children and retirement

The couple also asked whether they should delay having children.

ChatGPT noted that family planning is a personal decision, but from a purely financial perspective, waiting until cash flow improves would reduce stress. Child-related expenses can be significant, particularly in the early years.

On retirement, the recommendation was not to panic. While investing for retirement is important, the current priority should be eliminating high-cost debt. Once the major loans are repaid, retirement savings can accelerate significantly.

Turning Point

The most encouraging aspect of the couple's situation is that it is temporary.

When the personal loan ends in 2028, nearly ₹70,000 per month will be freed up. As the bike and education loans are also completed, the family's monthly surplus could rise by more than ₹80,000.

If that amount is invested consistently rather than spent, the couple's financial trajectory could change dramatically.

Financial collapse

ChatGPT's conclusion was straightforward: this couple is not facing a financial collapse. They are in a debt-repayment phase created by a large but finite obligation. For the next few years, the focus should be on avoiding new loans, building a modest emergency fund, delaying major purchases, and preparing to redirect future EMI savings into investments.

The challenge is real — but it is temporary. The financial decisions made between now and 2028 could determine whether the couple enters their 40s burdened by money worries or on a path toward long-term financial security.

Gautam Adani tops Hurun real estate rich list, overtaking DLF's Rajiv Singh

Gautam Adani tops Hurun real estate rich list, overtaking DLF's Rajiv Singh Amid US probe, India set to prohibit import of goods manufactured using forced labour

Amid US probe, India set to prohibit import of goods manufactured using forced labour Govt releases new monthly Services Production Index; Here's what the first data shows

Govt releases new monthly Services Production Index; Here's what the first data shows Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts

Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts Assam's debt surged 4.5-fold to ₹1.62 lakh crore in 10 years, government tells Assembly

Assam's debt surged 4.5-fold to ₹1.62 lakh crore in 10 years, government tells Assembly Is India Prepared For An Oil Shock? Expert Explains Supply Risks Amid West Asia Conflict

Is India Prepared For An Oil Shock? Expert Explains Supply Risks Amid West Asia Conflict Why Coforge Could Outperform The Market Over The Next 12–24 Months | Rakesh Vyas Explains

Why Coforge Could Outperform The Market Over The Next 12–24 Months | Rakesh Vyas Explains War In West Asia: What It Means For India's Oil Supply, Fuel Prices & Economy

War In West Asia: What It Means For India's Oil Supply, Fuel Prices & Economy “Pakistani Cricket Team Brought Drugs To India”: RVS Mani’s Explosive Claim Sparks Row

“Pakistani Cricket Team Brought Drugs To India”: RVS Mani’s Explosive Claim Sparks Row Indian I.T. Stocks Outlook: Why Midcap And Smallcap I.T. Could Lead The AI Comeback

Indian I.T. Stocks Outlook: Why Midcap And Smallcap I.T. Could Lead The AI Comeback Sensex falls 561 pts as crude oil price boils, rupee sinks; what's next for investors? Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts

Sensex falls 561 pts as crude oil price boils, rupee sinks; what's next for investors? Rupee falls 57 paise to 96.20 against dollar; further weakness likely, say analysts Is Swiggy the next Eternal? Quest PMS' Vyas reveals portfolio view after stock correction

Is Swiggy the next Eternal? Quest PMS' Vyas reveals portfolio view after stock correction Brent crude rally revives pressure on paint, tyre and aviation stocks; should investors be worried?

Brent crude rally revives pressure on paint, tyre and aviation stocks; should investors be worried? Suzlon, BHEL, Adani Power, Waaree, Adani Green, Tata Power: Check fresh ratings & targets

Suzlon, BHEL, Adani Power, Waaree, Adani Green, Tata Power: Check fresh ratings & targets