If investors choose the monthly payout option, the interest earned is credited every month instead of being compounded till maturity.If investors choose the monthly payout option, the interest earned is credited every month instead of being compounded till maturity.

If investors choose the monthly payout option, the interest earned is credited every month instead of being compounded till maturity.If investors choose the monthly payout option, the interest earned is credited every month instead of being compounded till maturity.Many investors continue to prefer fixed income instruments over market-linked products such as equities and mutual funds, especially during periods of volatility and economic uncertainty. Among these, fixed deposits (FDs) remain one of the most popular low-risk investment options for individuals seeking stable returns, capital protection, and predictable monthly income.

In 2026, interest in fixed deposits has increased again as banks and financial institutions offer FD rates ranging between 5.75% and 7.75%, while some small finance banks are providing rates of up to 8.10% for select tenures. Senior citizens continue to receive additional interest benefits ranging from 0.25% to 0.75%, making FDs particularly attractive for retirees and conservative investors.

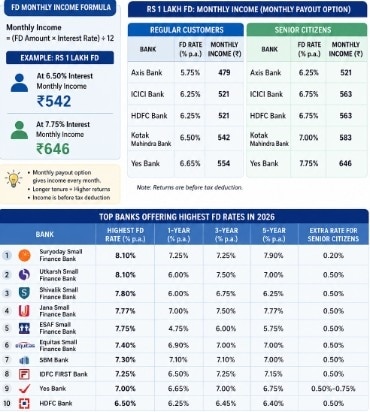

For investors planning to deposit Rs 1 lakh in a fixed deposit, monthly earnings depend mainly on three factors — the total deposit amount, the interest rate offered by the bank, and the payout option selected.

If investors choose the monthly payout option, the interest earned is credited every month instead of being compounded till maturity. This option is commonly preferred by retirees, salaried individuals seeking supplementary income, and risk-averse savers looking for predictable cash flow.

MUST READ: Bank FDs vs Post Office time deposits: Which offers better returns, safety, tax benefits in 2026?

Investing Rs 1 lakh in FD

The monthly income from an FD is calculated using the formula:

Monthly Income = (FD Amount × Interest Rate) ÷ 12

Based on current FD rates offered by major private sector banks, a Rs 1 lakh fixed deposit can generate monthly income ranging from around Rs 479 to Rs 646 before tax deductions.

For regular customers:

For senior citizens:

MUST READ: FD rates now: NBFC fixed deposits outpace banks in 2026 with returns up to 8.5%

Small finance banks offering the highest FD rates

Several small finance banks are currently offering some of the highest FD rates in the market. According to available FD data for 2026:

Among private banks, IDFC FIRST Bank, Yes Bank, Bandhan Bank, RBL Bank, Tamilnad Mercantile Bank, and IndusInd Bank are also offering relatively higher FD slab rates compared to larger peers. Public sector banks such as SBI, Bank of Baroda, Canara Bank, Punjab National Bank, and Union Bank of India continue to offer FD rates largely between 6% and 6.75%.

Financial planners say fixed deposits remain attractive because they provide assured returns, flexible tenure options ranging from 7 days to 10 years, and lower risk compared to market-linked investments. However, experts advise investors to compare FD rates, premature withdrawal rules, payout options, and post-tax returns before investing.

MUST READ: Fixed deposits (FD) vs Post Office schemes: Where to earn more in 1–5 years

TCS could soon have as many AI agents as employees, says N. Chandrasekaran

TCS could soon have as many AI agents as employees, says N. Chandrasekaran  and two weeks (7.22%).") Adani Power: After a blockbuster rally, Adani stock hits a pause; check price targets

Adani Power: After a blockbuster rally, Adani stock hits a pause; check price targets India has 15 FTAs covering 27 nations, but most exporters aren't using them effectively: GTRI report

India has 15 FTAs covering 27 nations, but most exporters aren't using them effectively: GTRI report Zojila tunnel breakthrough: The project that could change travel to Ladakh forever

Zojila tunnel breakthrough: The project that could change travel to Ladakh forever BT Explainer: How a special window to attract FCNR (B) deposits can help bring in more forex

BT Explainer: How a special window to attract FCNR (B) deposits can help bring in more forex What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV

What’s Hot: Stocks, Gold & Big Money Moves | Daily Market Show | Business Today TV Major Win For Indians As U.S. Court Blocks Trump's $100,000 H-1B Visa Fee Hike

Major Win For Indians As U.S. Court Blocks Trump's $100,000 H-1B Visa Fee Hike Zojila Tunnel Breakthrough: India Nears Completion Of World's Longest High-Altitude Road Tunnel

Zojila Tunnel Breakthrough: India Nears Completion Of World's Longest High-Altitude Road Tunnel TMC Crisis Deepens As MP Quits, Rebel Group Challenges Abhishek Banerjee

TMC Crisis Deepens As MP Quits, Rebel Group Challenges Abhishek Banerjee India Must Learn From China & Unleash Private Investment: Neelkanth Mishra

India Must Learn From China & Unleash Private Investment: Neelkanth Mishra Up to 76% upside! HAL, BHEL, Mazagon Dock, Coforge, BDL, Titagarh, HPCL among Antique's top picks

Up to 76% upside! HAL, BHEL, Mazagon Dock, Coforge, BDL, Titagarh, HPCL among Antique's top picks Rajesh Exports Chairman Rajesh Mehta on LIC: 'No contact; don't even know where LIC's office is … ' — Report

Rajesh Exports Chairman Rajesh Mehta on LIC: 'No contact; don't even know where LIC's office is … ' — Report FirstCry-promoted Swara Baby to file DRHP for IPO in June; eyes upto Rs 1,000 cr fundraise

FirstCry-promoted Swara Baby to file DRHP for IPO in June; eyes upto Rs 1,000 cr fundraise SpaceX IPO: Dividend policy of Musk’s space giant explained ahead of historic Nasdaq debut

SpaceX IPO: Dividend policy of Musk’s space giant explained ahead of historic Nasdaq debut Defence stocks: Choice initiates coverage on Mazagon Dock, GRSE, Cochin Shipyard — Targets

Defence stocks: Choice initiates coverage on Mazagon Dock, GRSE, Cochin Shipyard — Targets