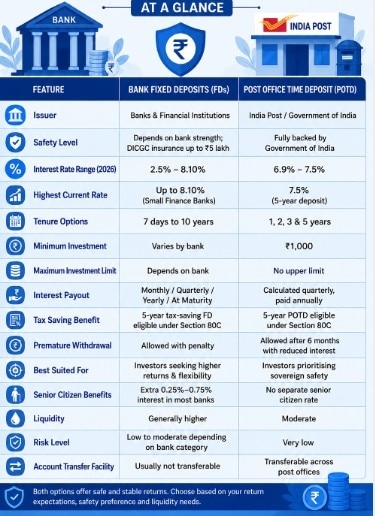

Bank FDs are offered by public sector banks, private banks and small finance banks, with tenures ranging from 7 days to 10 years. Post Office Time Deposits are government-backed savings schemes.Bank FDs are offered by public sector banks, private banks and small finance banks, with tenures ranging from 7 days to 10 years. Post Office Time Deposits are government-backed savings schemes.

Bank FDs are offered by public sector banks, private banks and small finance banks, with tenures ranging from 7 days to 10 years. Post Office Time Deposits are government-backed savings schemes.Bank FDs are offered by public sector banks, private banks and small finance banks, with tenures ranging from 7 days to 10 years. Post Office Time Deposits are government-backed savings schemes.Fixed deposits remain one of the most popular investment options for conservative savers looking for stable returns and capital protection. But for investors choosing between traditional bank fixed deposits (FDs) and Post Office Time Deposits (POTD), the decision now depends on more than just interest rates.

While banks currently offer FD rates as high as 8.10%, Post Office Time Deposits continue to attract investors seeking sovereign-backed safety and predictable returns.

Here’s how the two products compare in 2026.

Bank FDs vs Post Office time deposits

Both instruments allow investors to deposit a lump sum for a fixed period in return for guaranteed interest income.

Bank fixed deposits are offered by public sector banks, private banks and small finance banks, with tenures ranging from 7 days to 10 years.

Post Office Time Deposits, meanwhile, are government-backed savings schemes available for:

1 year

2 years

3 years

5 years

Unlike market-linked investments, both options provide fixed returns and are commonly used for short-term goals, retirement planning and emergency corpus parking.

Bank FD rates vs Time Deposit rates

Interest rates have become one of the biggest differentiators between the two products.

According to current 2026 data:

Small finance banks are offering FD rates up to 8.10%

Several private banks offer rates between 6.5% and 7.35%

PSU bank FD rates largely remain between 6% and 6.75%

Examples include:

Suryoday Small Finance Bank: 8.10%

Utkarsh Small Finance Bank: 8.10%

Jana Small Finance Bank: 7.77%

IDFC FIRST Bank: 7.25%

SBI: 6.45%

In comparison, Post Office Time Deposit rates for April–June 2026 are:

1-year: 6.9%

2-year: 7.0%

3-year: 7.1%

5-year: 7.5%

This means POTD rates are currently more competitive than many PSU and large private bank FDs, though some small finance banks still offer higher returns.

MUST READ: Want over 9% FD returns? These small finance banks offer up to 9.1% interest

Safety on investment

One major advantage of Post Office Time Deposits is safety.

POTDs are fully backed by the Government of India, making them among the safest fixed-income products available.

Bank FDs, while generally considered safe, carry varying levels of institutional risk depending on the bank category.

Although deposits up to ₹5 lakh are insured under DICGC cover, amounts beyond that remain exposed to bank-specific risks.

This makes POTDs particularly attractive for risk-averse investors and retirees prioritising capital protection.

MUST READ: FD rates now: NBFC fixed deposits outpace banks in 2026 with returns up to 8.5%

Tax benefits, liquidity

The 5-year Post Office Time Deposit qualifies for deduction under Section 80C of the Income-tax Act.

Similarly, tax-saving bank FDs with a 5-year lock-in also qualify for Section 80C benefits.

However, liquidity rules differ slightly.

Bank FDs generally offer easier premature withdrawal facilities, though penalties may apply.

POTDs allow premature withdrawal only after six months, with reduced interest rates in such cases.

MUST READ: Fixed deposits (FD) vs Post Office schemes: Where to earn more in 1–5 years

Who should choose what?

Financial planners say the choice depends on investor priorities.

Bank FDs may suit investors:

Seeking higher interest rates

Looking for flexible tenure options

Comfortable taking limited institutional risk

Post Office Time Deposits may suit investors:

Prioritising sovereign-backed safety

Seeking stable long-term income

Looking for tax-saving fixed-income options

With interest rates remaining elevated in 2026, both products continue to remain attractive for conservative savers, retirees and investors seeking predictable income amid market volatility.

MUST READ: Bank FD rates 2026: Top returns for 1, 3 and 5-year deposits compared

IT hiring falls to 28-month low, but demand for AI talent remains strong

IT hiring falls to 28-month low, but demand for AI talent remains strong Lilly’s experimental drug now shows benefits across obesity, diabetes, other conditions

Lilly’s experimental drug now shows benefits across obesity, diabetes, other conditions  Adani Power corrects, but bullish signals remain intact: What investors should know

Adani Power corrects, but bullish signals remain intact: What investors should know Wipro, MTAR Technologies, Netweb Technologies shares slip up to 8% today

Wipro, MTAR Technologies, Netweb Technologies shares slip up to 8% today  YES Bank shares rebound to near 52-week high despite GST notice; check target price & more

YES Bank shares rebound to near 52-week high despite GST notice; check target price & more Russians, Americans & Indians Are Betting Big On UAE Real Estate | Ankur Aggarwal, BNW Developments

Russians, Americans & Indians Are Betting Big On UAE Real Estate | Ankur Aggarwal, BNW Developments How PM Modi’s Ujjwala Yojana Transformed 10 Crore Families and Empowered Women Across India

How PM Modi’s Ujjwala Yojana Transformed 10 Crore Families and Empowered Women Across India TECH-IT-EASY | The Tech Gear Show EP 5 | Latest Technology News | Business Today

TECH-IT-EASY | The Tech Gear Show EP 5 | Latest Technology News | Business Today Latest Launches Of The Week With AI SANA | Tech Gear EP 5 | Business Today

Latest Launches Of The Week With AI SANA | Tech Gear EP 5 | Business Today "India Has World-Class Talent": Putin Unveils Russia's $25 Billion Commitment

"India Has World-Class Talent": Putin Unveils Russia's $25 Billion Commitment Rajesh Exports shares in free fall mode: Back-to-back lower circuits - What SEBI Chairman saidWipro, MTAR Technologies, Netweb Technologies shares slip up to 8% today YES Bank shares rebound to near 52-week high despite GST notice; check target price & moreAdani Power corrects, but bullish signals remain intact: What investors should know

Rajesh Exports shares in free fall mode: Back-to-back lower circuits - What SEBI Chairman saidWipro, MTAR Technologies, Netweb Technologies shares slip up to 8% today YES Bank shares rebound to near 52-week high despite GST notice; check target price & moreAdani Power corrects, but bullish signals remain intact: What investors should know Apollo Hospitals, Federal Bank, GAIL, NBCC: Top stocks to buy - targets, stop loss & more

Apollo Hospitals, Federal Bank, GAIL, NBCC: Top stocks to buy - targets, stop loss & more