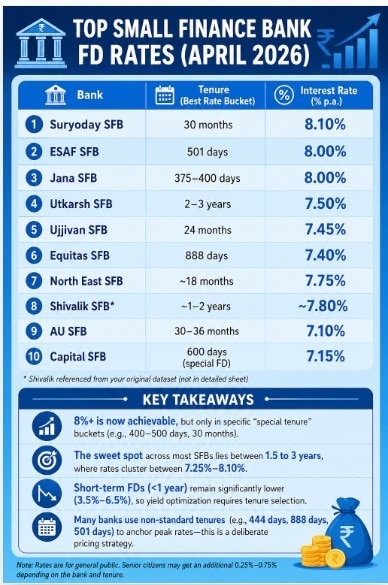

The optimal investment window lies between 1.5 to 3 years, where most SFBs offer 7.25% to 8.10%, balancing yield and duration risk.The optimal investment window lies between 1.5 to 3 years, where most SFBs offer 7.25% to 8.10%, balancing yield and duration risk.

The optimal investment window lies between 1.5 to 3 years, where most SFBs offer 7.25% to 8.10%, balancing yield and duration risk.The optimal investment window lies between 1.5 to 3 years, where most SFBs offer 7.25% to 8.10%, balancing yield and duration risk.Top FD rates: Small finance banks (SFBs) continue to dominate the fixed deposit (FD) rate landscape in April 2026, offering interest rates of up to 8.10% per annum—well above the levels seen at most public and private sector banks. The higher yields have strengthened their appeal among investors seeking stable, predictable returns in a relatively range-bound interest rate cycle.

Fixed deposits remain a cornerstone of retail investing in India, particularly for risk-averse savers. These instruments allow individuals to invest for tenures ranging from 7 days to 10 years, offering assured returns and capital protection. However, the divergence in FD rates across banking segments has widened, making rate comparison critical for optimising returns.

SFBs lead

Small finance banks (SFBs) are currently offering some of the most attractive fixed deposit (FD) rates in April 2026, with select tenures delivering returns of up to 8.10% per annum. Among small finance banks, Suryoday Small Finance Bank leads with a peak rate of 8.10% for 2–3 year deposits and around 7.90% for 3–5 year tenures. ESAF Small Finance Bank offers up to 8.00%, while Jana Small Finance Bank provides rates of up to 7.77%. Other players such as Ujjivan, Utkarsh, and Shivalik SFBs are offering returns in the 7.20%–7.80% range across key maturities.

Banks such as Suryoday SFB (8.10% at 30 months), ESAF SFB (8.00% at 501 days), and Jana SFB (8.00% at 375–400 days) are leading the rate cycle, significantly outperforming traditional banks.

A clear pattern emerges from the data: the highest rates are concentrated in non-standard or “special tenure” buckets, typically ranging between 400 days and 30 months. For instance, ESAF offers 8.00% at 501 days, while Equitas peaks at 7.40% at 888 days. This indicates a deliberate pricing strategy where banks incentivise specific maturities to manage asset-liability mismatches.

The optimal investment window lies between 1.5 to 3 years, where most SFBs offer 7.25% to 8.10%, balancing yield and duration risk. In contrast, shorter tenures below one year continue to offer significantly lower returns, typically in the 3.5%–6.5% range.

Overall, while SFBs offer a clear yield advantage, investors should combine rate comparison with tenure strategy and deposit safety considerations to optimise returns.

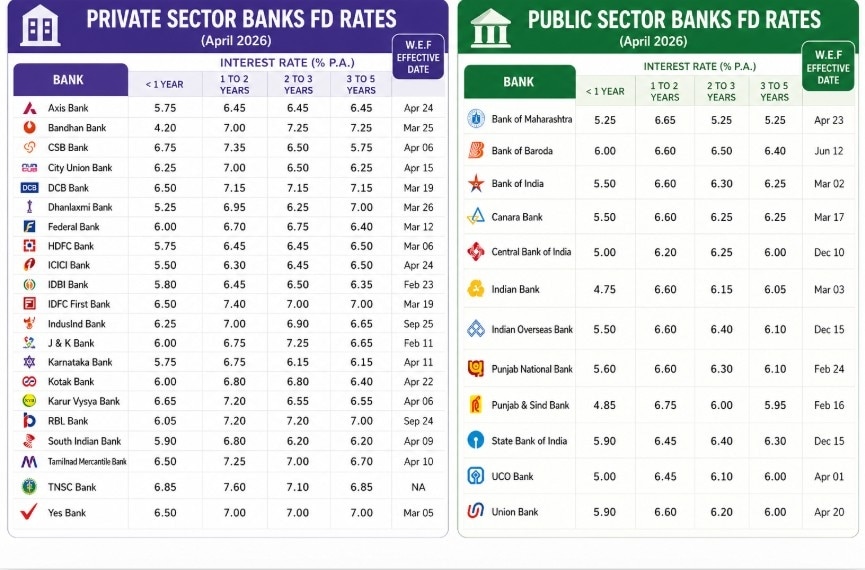

Private banks

Among private sector lenders, IDFC First Bank is offering up to 7.40% for 1–2 year deposits and around 7.00% for longer tenures, making it one of the more competitive large players. DCB Bank and RBL Bank offer rates in the 7.15%–7.20% range, while Bandhan Bank provides up to 7.25% for medium-term deposits.

However, large private banks such as HDFC Bank, ICICI Bank, and Axis Bank continue to offer relatively moderate rates, typically in the 6.30%–6.50% range across most tenures. These banks prioritise balance sheet stability and lower cost of funds, which reflects in comparatively lower FD yields.

Public sector banks

Public sector banks (PSBs), including State Bank of India (SBI), Punjab National Bank (PNB), and Bank of Baroda, are offering FD rates largely between 6.30% and 6.60% for common tenures. Punjab & Sind Bank stands slightly higher at around 6.75% for select maturities. While PSBs lag behind in terms of returns, they continue to attract a large depositor base due to strong trust, perceived sovereign backing, and extensive branch networks.

Senior citizen advantage

Across categories, most banks offer an additional 0.50 percentage points or more for senior citizens, enhancing effective returns. However, investors must balance yield with safety. Deposits up to ₹5 lakh are insured under the DICGC framework, making diversification across banks a prudent strategy for larger investments.

Strategic Points

With rates touching 8.10%, small finance banks offer a clear yield advantage in April 2026. However, private and public sector banks continue to play a role for investors prioritising stability and brand trust over incremental returns.

BPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets

BPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets Now, Trump is talking of Hormuz tolls if US-Iran deal collapses. What's his proposal?

Now, Trump is talking of Hormuz tolls if US-Iran deal collapses. What's his proposal? Transfers, promotions to go digital? Centre plans major HR overhaul at PSU banks

Transfers, promotions to go digital? Centre plans major HR overhaul at PSU banks") Jammers, 1.38 lakh CCTV cameras: How NTA is gearing up for big NEET re-test today

Jammers, 1.38 lakh CCTV cameras: How NTA is gearing up for big NEET re-test today Explained: Why Rajasthan is getting more rain than Maharashtra this June

Explained: Why Rajasthan is getting more rain than Maharashtra this June Why Do AI Data Centres Use So Much Water ? | Explained

Why Do AI Data Centres Use So Much Water ? | Explained Why Is India’s Cruise Market Just Getting Started?

Why Is India’s Cruise Market Just Getting Started? Versailles Peace Deal Explained: How U.S.-Iran War Moved From Missiles To MoU

Versailles Peace Deal Explained: How U.S.-Iran War Moved From Missiles To MoU Power Bags ₹5,000 Crore Karnataka Project, Unveils Big Mumbai Expansion Plan

Power Bags ₹5,000 Crore Karnataka Project, Unveils Big Mumbai Expansion Plan U.S.-Iran War Explained: From Operation Epic Fury To Strait Of Hormuz Crisis And Peace Deal

U.S.-Iran War Explained: From Operation Epic Fury To Strait Of Hormuz Crisis And Peace Deal Defence stocks to buy: Brokerage firms go bullish on this multibagger for strong gainsBPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets

Defence stocks to buy: Brokerage firms go bullish on this multibagger for strong gainsBPCL, HPCL and IOC: OMCs still not out of the woods? Share price targets BSE, Hyundai, Pine Labs, Ather & others: Top 12 fresh brokerage picks with upto 64% upside

BSE, Hyundai, Pine Labs, Ather & others: Top 12 fresh brokerage picks with upto 64% upside Are mid- and small-caps poised to lead the next leg of the market rally? Experts explain why

Are mid- and small-caps poised to lead the next leg of the market rally? Experts explain why India's average digital investor holds ₹10 lakh, adds ₹3 lakh a year: Report

India's average digital investor holds ₹10 lakh, adds ₹3 lakh a year: Report