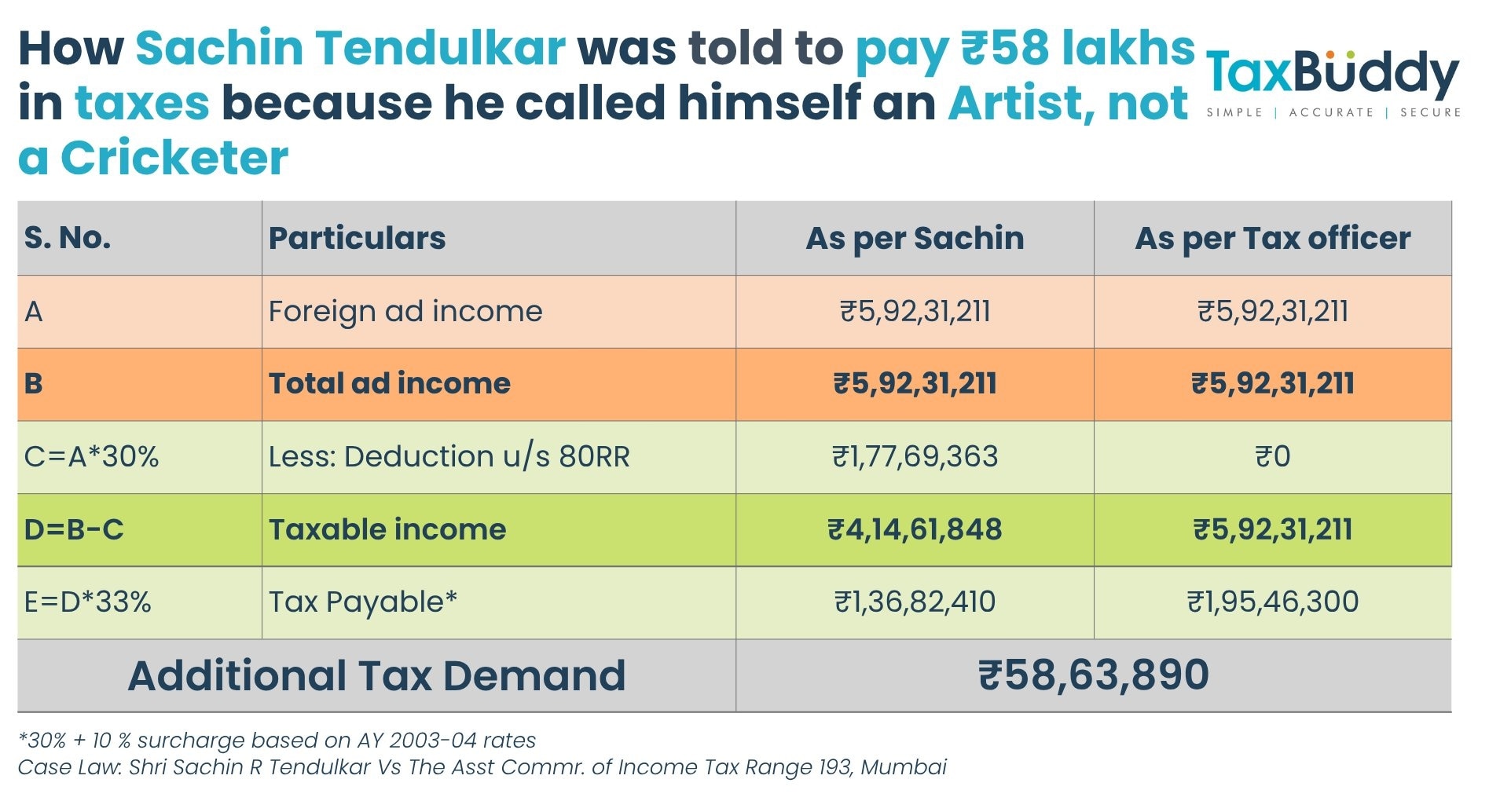

Under Section 80RR, Indian residents who are authors, artists, actors, musicians, or sportsmen can claim tax deductions on foreign income earned from their professional work

Under Section 80RR, Indian residents who are authors, artists, actors, musicians, or sportsmen can claim tax deductions on foreign income earned from their professional workCricket icon Sachin Tendulkar may be celebrated as the “Master Blaster” on the field, but off the field, he once made headlines for a completely different reason — proving that he was also an actor to save on taxes. Over a decade ago, Tendulkar found himself in a legal dispute with the Income Tax Department over how his foreign earnings from brand endorsements should be classified under the Income Tax Act.

Sujit Bangar, Founder of TaxBuddy.com, recently revisited this intriguing case on the social media platform X (formerly Twitter). “Sachin Tendulkar wasn’t a ‘cricketer.’ He claimed he was an actor — to save ₹58 lakh in taxes. The tax officer raised a demand on him. But here’s how the Master Blaster proved he was an actor, not a cricketer, and won the case,” Bangar wrote.

Where are the jobs: Youth unemployment remains high; fewer jobs for those with higher education in India

Where are the jobs: Youth unemployment remains high; fewer jobs for those with higher education in India What’s slowing the next phase of GCC growth?

What’s slowing the next phase of GCC growth? 576 individuals reported gross income exceeding ₹100 crore in AY 2025-26

576 individuals reported gross income exceeding ₹100 crore in AY 2025-26 NFO alert: SBI MF floats Nifty Midcap 150 Momentum 50 ETF FOF; why should you choose it

NFO alert: SBI MF floats Nifty Midcap 150 Momentum 50 ETF FOF; why should you choose it Nitin Gadkari moves Bombay High Court against viral E20 deepfakes, hits Meta with suit

Nitin Gadkari moves Bombay High Court against viral E20 deepfakes, hits Meta with suit  Infosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour Penalty

Infosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour Penalty I.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance?

I.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance? France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country

France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country Maruti Suzuki Eyes 25-30% SUV Growth, Says CNG Demand Has Overtaken Diesel

Maruti Suzuki Eyes 25-30% SUV Growth, Says CNG Demand Has Overtaken Diesel "Don't Divert Focus From Students' Future": Rijiju Urges Oppn To Debate Anti-Paper Leak Bill

"Don't Divert Focus From Students' Future": Rijiju Urges Oppn To Debate Anti-Paper Leak Bill Tata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore

Tata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore HDFC Bank concludes internal review into MSRDC deposit arrangements; CEO, CFO among 3 fined Rs 1 lakh

HDFC Bank concludes internal review into MSRDC deposit arrangements; CEO, CFO among 3 fined Rs 1 lakh How Narayana Murthy's era, Vishal Sikka's stint and Salil Parekh's tenure differed; big task awaits next Infosys CEO

How Narayana Murthy's era, Vishal Sikka's stint and Salil Parekh's tenure differed; big task awaits next Infosys CEO BEL Q1 results: Net profit rises 9%, revenue at Rs 5,533 crore

BEL Q1 results: Net profit rises 9%, revenue at Rs 5,533 crore  Sensex, Nifty snap five-session losing run; investors add Rs 5.1 lakh crore in wealthTata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore

Sensex, Nifty snap five-session losing run; investors add Rs 5.1 lakh crore in wealthTata Power Q1 profit rises 11% to Rs 1,176 crore; revenue up 6%, capex tops Rs 5,300 crore CCTV Captures Thrissur-Kozhikode Bus Crash In Malappuram, One Killed And Around 20 InjuredInfosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour PenaltyI.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance?France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country

CCTV Captures Thrissur-Kozhikode Bus Crash In Malappuram, One Killed And Around 20 InjuredInfosys Fined In France: 70-Hour Work-week Debate Returns After €175,000 Labour PenaltyI.T. Sector Outlook: Is the Worst Over for Indian I.T. Stocks After Long Underperformance?France And Spain Wildfires Threaten Cap Ferret Mansions And Bordeaux Wine Country