Few would disagree with the Economic Survey of 2018-19 when it makes a case for investment as the "key driver" of India's growth - in line with the Chinese experience, as it says - which would create capacity, increase labour productivity, introduce new technology, allow creative destruction and generate jobs. Except, this seem highly unlikely in the current situation.

Here is a look at the state of investment - by both the central government and private corporate sector.

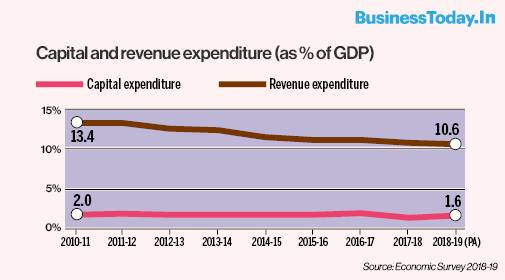

Shrinking government investment: Fiscal consolidation or investment?

The central government's total expenditure (both revenue and capital) has been declining sharply since 2010-11. From a high of 15.4% of the GDP in 2010-11, the total expenditure has hit a low of 12.2% of the GDP in 2018-19. The capital expenditure component has dropped from 2% of the GDP in 2010-11 to 1.6% in 2018-19 and that of the revenue expenditure from 13.4% in 2010-11 to 10.6% in 2018-19.

ALSO READ: No white elephants please! Where not to invest RBI surplus of Rs 1.76 lakh crore

This decline in expenditure is driven by the government's priority to contain fiscal deficit - which has indeed been brought down from 4.8% of the GDP in 2010-11 to 3.4% in 2018-19. The Economic Survey of 2018-19, as do several studies, explain that contrary to earlier years when tax buoyancy took care of fiscal consolidation, that is no more so.

In January this year, the Centre for Monitoring Indian Economy (CMIE), which tracks new projects, pointed out that fresh investment in the public sector had reached 14 years low with an announcement of fresh investments of Rs 50,604 crore in the December quarter of 2018-19 - the lowest since December 2004.

Now that the government has set its priority on reducing the fiscal deficit to 3.3% - a target it failed to achieve last fiscal - and its revenue on a persistent downward swing, there is little room for increasing investment in near future.

ALSO READ: BT Buzz: Are structural weaknesses, fundamental shifts slowing Indian economy?

Shrinking revenue: Little room for investment

The shrinking central government expenditure has everything to do with shrinking tax revenue. The total revenue receipt has fallen from 10.1% of the GDP in 2010-11 to 8.2% in 2018-19.

The tax revenue, which constitutes the larger share of total revenue, has declined from 7.3% of the GDP in 2010-11 to 6.9% in 2018-19. The non-tax revenue too has dropped from 2.8% in 2010-11 to 1.3% in 2018-19.

The tax revenue is set to dip further.

ALSO READ: Indian economy set for weakest quarter of growth in five years: report

That is because the government's target of achieving net tax of Rs 16.5 lakh crore in 2019-20 is based on the assumption of a 12% nominal growth (or about 8.8% of real GDP growth at 3.15% general CPI inflation in July 2019) - a level India has not reached in the recent memory. A SBI research shows that the real growth of GDP will slip from 5.8% in the last quarter of 2018-19 to 5.6% in the first quarter of 2019-20.

The monthly data of the Controller General of Accounts (CGA) shows net tax revenue collection for first quarter of 2019-20 (Apr-Jun) is Rs 2,51,411 crore - which is substantially less than the average quarterly collection of 2018-19 (Rs 329,250 crore), though higher than the corresponding period of 2018-19 (Rs 2,37170 crore).

Further, last week's announcement by the finance minister withdrawing angel tax, surcharges on foreign portfolio investors and those earning more than Rs 2 crore and an upfront capital infusion of Rs 70,000 crore into public sector banks would reduce the scope for investment.

Shrinking private investment

If the government investment is going down, so do the private investment.

The RBI, which tracks capital expenditure (capex) plans of private corporate sector (projects that are already 'funded' by financial institutions, including through their IPOs), finds that both the 'animal spirits' and the 'business sentiments' are missing since 2010-11.

Its May 2019 report says the year 2017-18 "marked the seventh successive annual contraction in the private corporate sector's capex plans". For the year 2017-18, the capex plans declined by 10.15% (annual growth rate) from Rs 165,000 crore in 2016-17.

While the RBI tracks envisaged investments of private sector, the Central Statistics Office (CSO) of the government maps 'realised investment' or gross fixed capital formation (GFCF).

ALSO READ: Sans tax cuts or sops, can FM Sitharaman's confidence-building measures remedy slowdown blues

As per the CSO data (National Accounts Statistics), available until 2016-17 at current prices, the private corporate sector component of GFCF (GFCF has three components - public, private and household sectors) has gone up from 11.2% in 2011-12 to 12.3% in 2016-17.

There is one difference between these two sets of data. There is often a time lag between the envisaged or declared investment (capex plans) and the investments that has already been realised (GFCF). The annual growth rates of the two show a parallel movement over a long horizon, as could be seen in the following graph.

The trend reflected by the CSO data (up to 2016-17), however, runs contrary to the RBI data on sectoral deployment of bank credits.

According to the RBI, growth in the bank credit to industry has witnessed a sharp fall from 24.4% of the GDP in 2010 to 6.9% in 2019, reflecting poor appetite of the industry to investment.

Besides, industrial production and capacity utilisation also run contrary to the CSO trend.

The RBI data shows that growth in the index of industrial production (IIP) for manufacturing (which accounts for 77.63% of the IIP) has been confined to a lower band of 2.8-4.8% (with an annual average of 4%) between 2011-12 and 2018-19, while the earlier years, between 2004-05 and 2010-11 (base year 2004-05) saw average growth of 10%.

Eminent economists C Rangarajan and DK Srivastava recently raised doubts about the CSO data on private investment by observing that it runs counter to what the industry leaders have been saying and what other data sources such as CMIE indicate, "casting some doubts on the veracity of the figures".

Government's investment plans for infrastructure sector

Last week, the Finance Minister Nirmala Sitharaman reiterated her budget promise of investing Rs 100 lakh crore in infrastructure over the next five years. This sounds good except that no fund has been allocated for it nor has she explained where the resources would come from.

Here is a sobering thought.

The 2019-20 Budget's total revenue target is just a fraction of it - Rs 19.63 lakh crore, out of which Rs 16.5 lakh crore would be tax revenue and Rs 3.13 lakh crore non-tax revenue, including anything that disinvestment would generate.

ALSO READ: Experts analyse government's efforts to revive economic growth

So where will the money come from?

Even if the RBI transfers Rs 1,76,051 crore to the central government, as was announced on Monday night, that would not be much, given that the 2019-20 Budget had already accounted for Rs 90,000 crore of it as a part of its non-tax revenue receipts -- a total of Rs 1.06 lakh crore of dividend/surplus from the RBI and other nationalised banks and financial institutions for 2019-20.

Sovereign overseas borrowing, as proposed in the 2019-20 Budget, no longer seems an option after the sudden transfer of finance secretary Subhash Chandra Garg - who supposed to have pushed for it and paid the price for it (he has applied for voluntary retirement since then) and a strong caution from leading bankers and economists.

That leaves the question abegging: Who or what will bring resources for fresh investment to revive the economy?

Xbox cuts 3,200 jobs: CEO Asha Sharma blames hardware slump, rising costs behind hard reset

Xbox cuts 3,200 jobs: CEO Asha Sharma blames hardware slump, rising costs behind hard reset India's cooling revolution: How rising incomes, better tech turned ACs from luxury to necessity

India's cooling revolution: How rising incomes, better tech turned ACs from luxury to necessity Your EPF balance is about to rise: EPFO orders 8.25% interest credit

Your EPF balance is about to rise: EPFO orders 8.25% interest credit CCI may consider market study on digital economy

CCI may consider market study on digital economy E20 petrol in pre-2022 cars: Engineer’s blog post against panic goes viral

E20 petrol in pre-2022 cars: Engineer’s blog post against panic goes viral The Next Big Winners In The Stock Market | Aparna Shanker's Investment Playbook

The Next Big Winners In The Stock Market | Aparna Shanker's Investment Playbook PM Modi In Jakarta: BrahMos Deal In Focus As India Indonesia Defence Ties Enter Big Phase

PM Modi In Jakarta: BrahMos Deal In Focus As India Indonesia Defence Ties Enter Big Phase India Vs Global Markets: Devina Mehra Explains Rupee Risk, PMS Strategy And Diversification

India Vs Global Markets: Devina Mehra Explains Rupee Risk, PMS Strategy And Diversification Indian Stock Market Bottom? Devina Mehra Reveals Why Downside May Be Limited

Indian Stock Market Bottom? Devina Mehra Reveals Why Downside May Be Limited India Stock Market Outlook: Top Sectors For The Next 18-24 Months

India Stock Market Outlook: Top Sectors For The Next 18-24 Months Realty stock climbs after record quarterly pre-sales; check target price, outlook

Realty stock climbs after record quarterly pre-sales; check target price, outlook Sensex, Nifty take winning run to fourth session; investor wealth swells by over Rs 8.2 lakh crore

Sensex, Nifty take winning run to fourth session; investor wealth swells by over Rs 8.2 lakh crore TCS Q1 results, dividend announcement: Key dates, earnings preview, 5 things to watch

TCS Q1 results, dividend announcement: Key dates, earnings preview, 5 things to watch IT stocks to buy: TCS, Infy, TechM, HCL Tech, Persistent, Netweb, KPIT; Check target price

IT stocks to buy: TCS, Infy, TechM, HCL Tech, Persistent, Netweb, KPIT; Check target price Ola Electric shares extend fall, tumble over 6%; here's what's weighing on the stock

Ola Electric shares extend fall, tumble over 6%; here's what's weighing on the stock