Nuvama favoured Max Financial Services Ltd, JK Cement Ltd and Crompton Greaves Consumer Electricals Ltd. (Pic: AI generated for representational purposes only)

Nuvama favoured Max Financial Services Ltd, JK Cement Ltd and Crompton Greaves Consumer Electricals Ltd. (Pic: AI generated for representational purposes only) Nuvama favoured Max Financial Services Ltd, JK Cement Ltd and Crompton Greaves Consumer Electricals Ltd. (Pic: AI generated for representational purposes only)

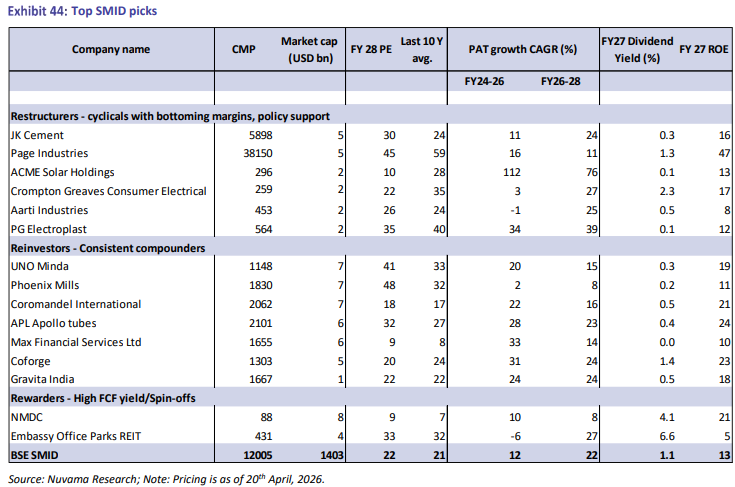

Nuvama favoured Max Financial Services Ltd, JK Cement Ltd and Crompton Greaves Consumer Electricals Ltd. (Pic: AI generated for representational purposes only)Smallcap and midcap (SMID) stocks, represented by the BSE Small and Midcap 400 Index, have rebounded sharply in April to the pre-war level of 12,000 despite lingering uncertainties around supply shocks. While Nuvama Alternative & Quantitative Research viewed SMID valuations as expensive, despite the index being stuck between 11,000 to 13,000 levels for the last two years, it identified value-buying opportunities in consumer durables, chemicals, IT and select auto ancillaries. The brokerage preferred stocks such as ACME Solar Holdings Ltd, Coforge Ltd, Page Industries Ltd, UNO Minda, NMDC Ltd, Gravita India Ltd, PG Electroplast Ltd and Aarti Industries Ltd. It also favoured Max Financial Services Ltd, JK Cement Ltd and Crompton Greaves Consumer Electricals Ltd among its top picks.

Nuvama classified these stocks into three groups. The first, termed ‘Restructurers’, included cyclicals with bottoming margins and policy support. The second category, ‘Reinvestors’, comprised consistent compounders, while the third, ‘Rewarders’, included companies with high free cash flow yields. Embassy Office Parks REIT and NMDC Ltd were grouped under ‘Rewarders’. UNO Minda, Coromandel International Ltd and Coforge Ltd were categorised as ‘Reinvestors’, while Page Industries Ltd and PG Electroplast Ltd were identified as ‘Restructurers’.

With regards to valuations, consumption stocks are now much cheaper than most cyclicals, not just relative to their own history, but also with regards to levels, Nuvama said.

"Durables, FMCG, even retail are all trading at the lower end of their valuations. While some of the cyclicals in SMIDs—industrials, defence, metals are trading at the higher end of the spectrum. Real estate is perhaps a space amongst cyclicals where valuations have moved somewhat lower," Nuvama added.

The brokerage sees near-term earnings pressure. But while demand recovery post the 2022 disruption was led by capex, it sees consumption outpacing capex this time, given the higher policy support.

"SMIDs are trading at 20–30 per cent premium to large caps—nearly all-time high, despite their one-year forward EPS growth differential vanishing as compared to 40 per cent discount seen during the previous bottoms. The valuation premiums look particularly high in the context of weak earnings differential," Nuvama said.

That said, it said earnings growth of Indian SMIDs is now in line or rather underperforming their global peers, back to its pre-Covid-19 trend. This is in sharp contrast to the 2023–24 phase where higher earnings growth justified a larger premium. Thus, large premium to global peers may perhaps not be warranted, Nuvama said.

NEET retest 2026: Govt bans Telegram app until June 22. Here's why

NEET retest 2026: Govt bans Telegram app until June 22. Here's why  TCS to take $70 million Q1 hit after US Supreme Court rejects appeal in DXC trade secrets case

TCS to take $70 million Q1 hit after US Supreme Court rejects appeal in DXC trade secrets case Govt must revive privatisation of PSUs, PSBs: Arvind Panagariya

Govt must revive privatisation of PSUs, PSBs: Arvind Panagariya Suzlon shares rally 55% in 3 months: Why brokerages see more upside ahead — Targets

Suzlon shares rally 55% in 3 months: Why brokerages see more upside ahead — Targets Anthropic had 90 minutes to restrict Claude Fable 5 as White House feared Chinese access

Anthropic had 90 minutes to restrict Claude Fable 5 as White House feared Chinese access Netanyahu’s Nightmare: Israeli Minister Rejects Trump’s Peace Deal, Threatens Coalition Collapse

Netanyahu’s Nightmare: Israeli Minister Rejects Trump’s Peace Deal, Threatens Coalition Collapse Shiv Sena UBT Crisis: Uddhav Issues 48-Hour Ultimatum After 5 MPs Skip Meet

Shiv Sena UBT Crisis: Uddhav Issues 48-Hour Ultimatum After 5 MPs Skip Meet Ram Mandir Donation Controversy: Yogi Govt Orders SIT Probe Into Allegations

Ram Mandir Donation Controversy: Yogi Govt Orders SIT Probe Into Allegations UNSC Reforms: Ambassador Parvathaneni Exposes Flaws In Latest UN Elements Paper

UNSC Reforms: Ambassador Parvathaneni Exposes Flaws In Latest UN Elements Paper Stanford Walkout: Graduates Boo Sundar Pichai Over Google's $1.2B Israel Project Nimbus Deal

Stanford Walkout: Graduates Boo Sundar Pichai Over Google's $1.2B Israel Project Nimbus Deal YES Bank shares hit 52-week high, analysts share price targets

YES Bank shares hit 52-week high, analysts share price targets  Nikkei crosses 70,000 for first time: What's driving the rally?

Nikkei crosses 70,000 for first time: What's driving the rally? Global rally bypasses India as IPO momentum fades and foreign investors turn cautious. What lies ahead for markets?

Global rally bypasses India as IPO momentum fades and foreign investors turn cautious. What lies ahead for markets? Dixon, Kaynes, Amber, Avalon, Syrma SGS, Cyient DLM, Data Patterns: Share price targets

Dixon, Kaynes, Amber, Avalon, Syrma SGS, Cyient DLM, Data Patterns: Share price targets Jaiprakash Associates: Stock to delist on June 18, here's what happens to 6.5 lakh shareholders

Jaiprakash Associates: Stock to delist on June 18, here's what happens to 6.5 lakh shareholders