Sebi's shift brings greater predictability and reduces the discretion previously exercised by fund managers, which could sometimes work against investors, say experts.

Sebi's shift brings greater predictability and reduces the discretion previously exercised by fund managers, which could sometimes work against investors, say experts.  Sebi's shift brings greater predictability and reduces the discretion previously exercised by fund managers, which could sometimes work against investors, say experts.

Sebi's shift brings greater predictability and reduces the discretion previously exercised by fund managers, which could sometimes work against investors, say experts. In a major regulatory overhaul, the Securities and Exchange Board of India (SEBI) has discontinued solution-oriented mutual funds from February 2026, marking a decisive shift in how goal-based investing is structured and delivered. The move signals a transition from marketing-driven product positioning to a more disciplined, process-oriented investment framework.

Solution-oriented funds

Solution-oriented funds, typically marketed as retirement or children’s plans, were designed to appeal to investors through emotional goals. However, experts argue that these products often failed to deliver on their core promise.

"For years, solution-oriented funds such as retirement and children's plans were marketed as goal-based investments. The pitch was simple and powerful. Invest for your child's future or your retirement. This emotional positioning made them easy to sell, but often masked the reality underneath. Many of these funds were not structurally different from existing categories. In practice, they behaved like flexi cap or hybrid funds, with little alignment to the actual life goal they claimed to serve," said Hariprasad K, SEBI-registered Research Analyst and Founder – Livelong Wealth.

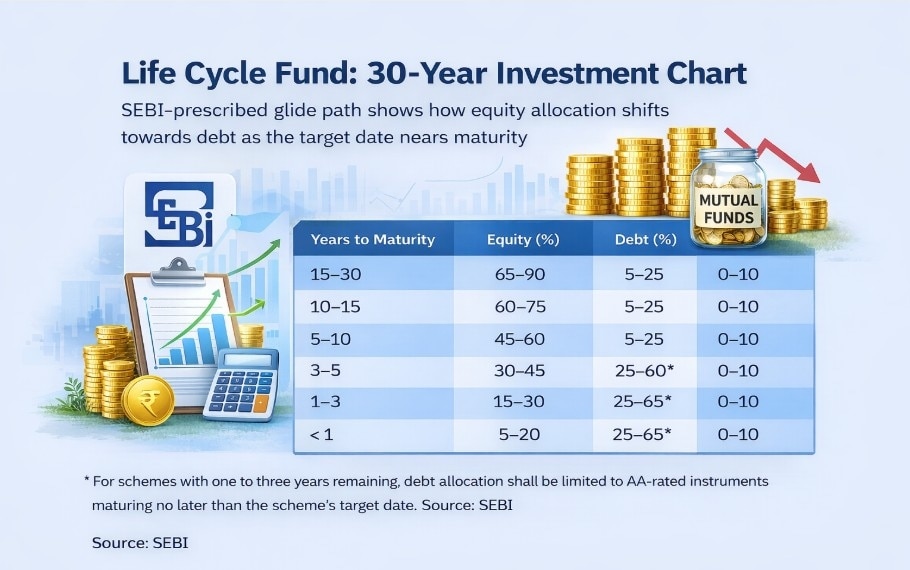

One of the most critical gaps identified in these funds was the absence of a defined “glide path”—a mechanism that adjusts asset allocation as investors approach their financial goals.

Hariprasad explained, "A retirement fund, for instance, could maintain high equity exposure even when the investor was close to retirement. In the event of a market correction, this could lead to significant capital erosion at the worst possible time. Investors were effectively paying for a 'solution' that lacked the most critical feature required to solve the problem."

ALSO READ: Gift cards for mutual funds? Sebi plans new route to invest using prepaid instruments

Life cycle funds

To address these shortcomings, SEBI has introduced Life Cycle Funds, a more structured alternative. These funds are designed around a target maturity timeline and follow a predefined asset allocation strategy that gradually reduces equity exposure while increasing allocation to safer assets like debt as the goal nears.

Hariprasad said this shift brings greater predictability and reduces the discretion previously exercised by fund managers, which could sometimes work against investors. It also enhances accountability, ensuring that portfolio construction aligns more closely with the investor’s time horizon rather than short-term return chasing.

What it means for investors

"For existing investors, the impact is more operational than financial. Systematic investment plans in older schemes have been discontinued, and many of these funds are being merged into broader categories such as diversified equity or multi-asset funds. Importantly, these transitions are largely tax neutral, meaning investors are not immediately impacted from a capital gains perspective. However, it does require awareness. Investors need to review where their money is being reallocated and whether it still aligns with their financial goals," Hariprasad added.

ALSO READ: April 1 tax shake-up: HRA, ITR forms, deadlines, meal cards, Form 130 explained

The broader implication of SEBI’s move is the emergence of a “true-to-label” regime in the mutual fund industry. By tightening category definitions and reducing overlap between schemes, the regulator aims to ensure that fund offerings accurately reflect their stated objectives. There is also a growing push toward better diversification, including exposure to alternative assets such as gold and silver.

For long-term investors, the message is clear: product labels alone are no longer sufficient. Understanding the underlying investment structure, particularly how risk is managed over time, is critical.

Ultimately, this reform aligns mutual fund investing more closely with sound financial planning principles—prioritising discipline, transparency, and outcome-oriented design over marketing narratives.

Major relief! Price of 19 kg LPG cylinder cut by ₹183.50; check new rates

Major relief! Price of 19 kg LPG cylinder cut by ₹183.50; check new rates Anthropic’s Claude Fable 5, Mythos 5 global access cleared by US govt; Global rollout starts July 1

Anthropic’s Claude Fable 5, Mythos 5 global access cleared by US govt; Global rollout starts July 1 KPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low

KPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer

Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer Agnikul, ICEYE tie up to explore sovereign satellite and launch system in India

Agnikul, ICEYE tie up to explore sovereign satellite and launch system in India Road Deaths In India: Nitin Gadkari Exposes The Deadly Impact Of Irresponsible Driving!

Road Deaths In India: Nitin Gadkari Exposes The Deadly Impact Of Irresponsible Driving! "Designed,Developed, & Manufactured In India": Rajnath Singh Calls For New Era Of Defence Excellence

"Designed,Developed, & Manufactured In India": Rajnath Singh Calls For New Era Of Defence Excellence Adani Ports Gets $1.4 Billion Boost As MSC Buys 49% Stake In Vizhinjam Port

Adani Ports Gets $1.4 Billion Boost As MSC Buys 49% Stake In Vizhinjam Port Oyo's Parent Company Files Updated DRHP To SEBI, Check Full Details Here

Oyo's Parent Company Files Updated DRHP To SEBI, Check Full Details Here Nifty Ends H1; Looks Ahead To Gains

Nifty Ends H1; Looks Ahead To Gains Vedanta Iron shares rally over 62% in two weeks; company issues clarification on price movement

Vedanta Iron shares rally over 62% in two weeks; company issues clarification on price movement Knack Packaging IPO opens today: Should you subscribe? Check price band, latest GMP & moreKPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low

Knack Packaging IPO opens today: Should you subscribe? Check price band, latest GMP & moreKPIT Technologies clarifies on H1 FY27 revenue outlook as stock slumps to 52-week low Madhusudan Kela buys stake in Genus Power via block deal, more details Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer

Madhusudan Kela buys stake in Genus Power via block deal, more details Advit Jewels delivers 37% listing gains; Cordelia Cruise turns into a wealth destroyer