Life Cycle Funds automatically shift from aggressive to conservative asset allocation over time, covering equity, debt, gold/silver ETFs, InvITs, and commodity derivatives.

Life Cycle Funds automatically shift from aggressive to conservative asset allocation over time, covering equity, debt, gold/silver ETFs, InvITs, and commodity derivatives. Life Cycle Funds automatically shift from aggressive to conservative asset allocation over time, covering equity, debt, gold/silver ETFs, InvITs, and commodity derivatives.

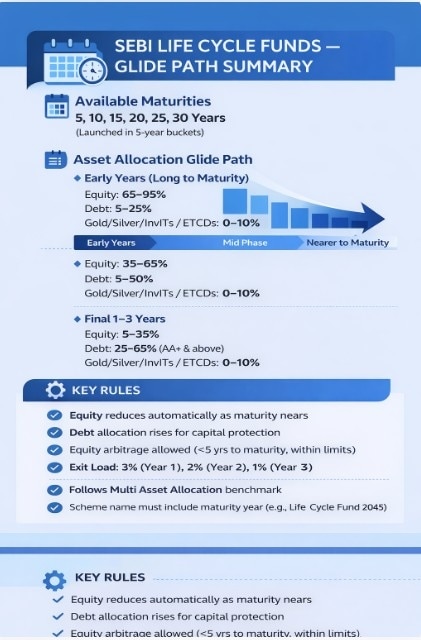

Life Cycle Funds automatically shift from aggressive to conservative asset allocation over time, covering equity, debt, gold/silver ETFs, InvITs, and commodity derivatives.The Securities and Exchange Board of India (SEBI) has unveiled a new mutual fund category — Life Cycle Funds — marking what many industry leaders describe as a significant step toward structured, goal-based investing. These open-ended target-date funds will have maturities ranging from five to 30 years, launched in five-year buckets such as Life Cycle Fund 2045 or Life Cycle Fund 2050, making the investment horizon immediately visible to investors.

Life Cycle Funds are designed around a glide path strategy, automatically shifting asset allocation from aggressive to conservative as the maturity date approaches. The structure spans multiple asset classes, including equity, debt, gold and silver ETFs, Infrastructure Investment Trusts (InvITs), and exchange-traded commodity derivatives (ETCDs). However, the allocation mix evolves over time to match the investor’s time horizon.

Radhika Gupta, CEO of Edelweiss Mutual Fund, welcomed the move, stating, “Over the last few years, SEBI has meaningfully expanded what asset managers can do. Debt passive regulations, Specialised Investment Funds, and now Life Cycle Funds are good examples. These aren’t cosmetic changes, rather they widen the solution set. It’s genuinely one of the most exciting times to be building in this business.”

She added that Life Cycle Funds are a “big step for goal-based investing” because asset allocation automatically aligns with an investor’s time horizon. “That reduces the need for constant decision-making, keeps investors disciplined, and does so within a tax-efficient structure. Simple in concept. Powerful in outcome. And very practical for long-term financial planning,” Gupta noted.

For example, a 30-year maturity Life Cycle Fund may begin with 65–95% exposure to equity in its early years. As the fund approaches maturity, equity exposure gradually declines to 5–20%, while debt allocation rises to as much as 25–65% in the final one to three years. Debt investments are restricted to AA+ and above-rated instruments to enhance safety. Exposure to gold, silver ETFs, InvITs, and ETCDs remains limited at 0–10%, primarily in the earlier years. For funds with less than five years to maturity, equity arbitrage exposure of up to 50% is permitted, while ensuring overall equity allocation remains within prescribed limits.

Life Cycle Funds

The new category effectively replaces the earlier Solution-Oriented Funds, such as retirement and children’s funds. Industry experts believe this resolves the problem of static allocation in older retirement products and removes taxation friction when investors switch funds to adjust asset allocation.

To promote long-term discipline, SEBI has prescribed a graded exit load structure: 3% if redeemed within the first year, 2% within the first two years, and 1% within the first three years. This is aimed at discouraging premature withdrawals and reinforcing long-term commitment.

Each Asset Management Company (AMC) can operate a maximum of six Life Cycle Funds at any given time. If a scheme has less than one year remaining to maturity, it may be merged with the nearest maturity Life Cycle Fund, subject to unitholder approval. Additionally, these funds will follow the benchmark framework prescribed for Multi Asset Allocation Funds, enhancing comparability and transparency.

The larger question remains: can Life Cycle Funds become a preferred vehicle for retirement and long-term goals? By embedding automatic asset allocation shifts and time-bound discipline into a single product, SEBI appears to be nudging investors toward simpler, behaviourally aligned investing. For individuals seeking structured retirement planning without constant portfolio rebalancing, Life Cycle Funds may indeed prove to be a practical and powerful solution.

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls

India's monsoon runs on a double engine: The hidden weather tag team deciding where the rain falls Same 43°C temperature, different reality: Why Europe's heatwave is more brutal than India's

Same 43°C temperature, different reality: Why Europe's heatwave is more brutal than India's 'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means

'Think of yourselves like stocks': WhatsApp chief Kunal Shah's advice for youth - what he means Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Dixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore

From engineers to product managers: Here's how much Anthropic pays, with salaries up to ₹13.02 crore HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match

HP EliteBook X G2a Review: An AI PC in 2026 With 64 GB RAM And A Price To Match China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System

China’s Modern Inequality System | Akshita Nandgopal Unpacks The Brutal Reality Of The Hukou System India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action

India Food Label Scam Explained By Sneha Mordani | FSSAI Issues Strict Action Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis UpdateDixon Technologies shares: Four factors why JM Financial upgraded the EMS stock  Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery

Coforge, KPIT Tech, Cyient among top IT stocks to buy for upto 44% upside amid AI recovery Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore

Infosys, Hindalco, Redington: How FPI-heavy stocks fared in June as outflows hit ₹53K crore Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates

Last chance next week to buy four Bajaj Group stocks for dividend; check payout, record dates Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure