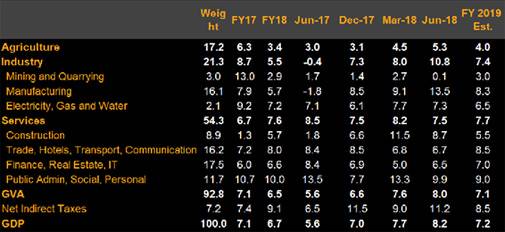

A quicker-than-expected acceleration in India's GDP growth last quarter was supported by a favourable, low base in the year-earlier period. Green shoots were also visible in certain sectors. The key takeaway - the pickup in growth, without demand-pull inflationary pressure in the economy, supports our thesis that reforms have lifted India's potential growth, and activity ahead is likely to remain non-inflationary.

Base Effects Plus Green Shoots of Recovery Driving Growth

In our view, India's potential growth is around 8-8.5%, above the consensus and Reserve Bank of India view of around 7-7.5%. Going ahead, we expect the output gap to remain negative and continue to pressure down core inflation. With inflation already starting to surprise on the downside, we expect the RBI to return to a long pause on rates.

History Suggests India's Potential Growth Likely Underestimated

Decomposition of Changes in RBI's Foreign Currency Assets

Looking ahead, quarterly GDP growth is expected to trend down as base effects turn adverse. Nevertheless, green shoots suggest that, adjusted for base effects, the recovery is likely to get stronger. This poses upside risks to our full year projection for GDP growth to recover to 7.2% in fiscal 2019 from 6.7% in fiscal 2018 -- 0.2 ppt below the central bank and consensus projection of 7.4%.

Our monthly tracker for the rural economy shows a strong recovery. We were expecting that the headwinds from higher oil prices, rising interest rates and a still-weak banking sector would pose risks to growth in the industrial sector and the urban areas. That might still be the case, but the latest growth numbers suggest that the structural reforms of the past few years are starting to support a broad-based growth recovery and are likely countering the headwinds.

Components of GDP Growth

Further Details:

India Forecast Table

Abhishek Gupta covers India for Bloomberg Economics in Mumbai. He previously worked as an economist at DSP Merrill Lynch and as a research analyst at the National Institute of Public Finance and Policy, India's premier macro/finance think tank.

Govt eases kerosene rules, allows sale via petrol pumps for 60 days

Govt eases kerosene rules, allows sale via petrol pumps for 60 days West Asia conflict: Iran warns US troops would become 'food for sharks' if ground operation begins

West Asia conflict: Iran warns US troops would become 'food for sharks' if ground operation begins  ‘Resort cities, not war zones’: Jeffrey Sachs cautions UAE against deeper role in Iran crisis

‘Resort cities, not war zones’: Jeffrey Sachs cautions UAE against deeper role in Iran crisis LPG or PNG connection? Your complete guide to gas connection problem

LPG or PNG connection? Your complete guide to gas connection problem  March 31 is a hard deadline, not a date: Miss the date and you will be voluntarily paying more

March 31 is a hard deadline, not a date: Miss the date and you will be voluntarily paying more BTS: Inside Business Today’s CEO Edition—Growth King Subbiah & Arundhati’s Digital Leadership Story

BTS: Inside Business Today’s CEO Edition—Growth King Subbiah & Arundhati’s Digital Leadership Story BT MindRush 2026: Lessons On Mindfulness And Resilience In A Turbulent World

BT MindRush 2026: Lessons On Mindfulness And Resilience In A Turbulent World The Murugappa Value-Creation Story: Legacy, Strategy & Growth In A New Era

The Murugappa Value-Creation Story: Legacy, Strategy & Growth In A New Era Making A Future-Ready Conglomerate | Anish Shah On Mahindra’s Strategy Shift

Making A Future-Ready Conglomerate | Anish Shah On Mahindra’s Strategy Shift A Leader’s Journey | Arundhati Bhattacharya On SBI Transformation & Digital India

A Leader’s Journey | Arundhati Bhattacharya On SBI Transformation & Digital India Why Goldman Sachs cut its Nifty target - Check new target

Why Goldman Sachs cut its Nifty target - Check new target JSW Steel, Coal India, Paytm, Sammaan Capital, Thermax among stocks in focus next week; here’s why

JSW Steel, Coal India, Paytm, Sammaan Capital, Thermax among stocks in focus next week; here’s why ‘Excess equity returns globally to correct’: Shankar Sharma bets on hard assets

‘Excess equity returns globally to correct’: Shankar Sharma bets on hard assets Exceptional market returns are made when you invest in times like this: Madhusudan Kela

Exceptional market returns are made when you invest in times like this: Madhusudan Kela Sensex, Nifty outlook for Monday, March 30: What to expect from stock market? Key levels, trading strategy & more

Sensex, Nifty outlook for Monday, March 30: What to expect from stock market? Key levels, trading strategy & more