One of primary reasons behind the downgrade was a prolonged energy shock stemming from geopolitical tensions, which severely impacted the economic outlook.One of primary reasons behind the downgrade was a prolonged energy shock stemming from geopolitical tensions, which severely impacted the economic outlook.

One of primary reasons behind the downgrade was a prolonged energy shock stemming from geopolitical tensions, which severely impacted the economic outlook.One of primary reasons behind the downgrade was a prolonged energy shock stemming from geopolitical tensions, which severely impacted the economic outlook.Goldman Sachs, earlier in a report dated March 26, downgraded Indian equities, slashing its 12-month Nifty target to 25,900 from 29,300.

This revision came as Goldman Sachs shifted its regional allocation for India to ‘marketweight’ from ‘overweight,’ citing a less attractive risk-reward scenario compared to North Asian markets.

One of the primary reasons behind the downgrade was a prolonged energy shock stemming from geopolitical tensions, which severely impacted the economic outlook.

“Our commodity analysts have raised their oil and gas price forecasts due to a longer impairment of Strait of Hormuz flows. Reflecting India’s greater vulnerability to the energy shock,” Goldman Sachs said.

According to Goldman Sachs, India's reliance on energy imports makes it vulnerable among Asian economies, as it has a low per capita income and high energy imports.

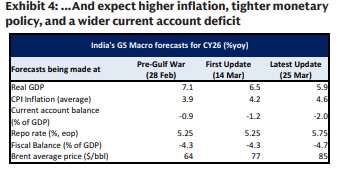

In response to crude oil surge, Goldman Sachs economists painted a different picture of the domestic economy. They slashed India's 2026 GDP growth forecast by 1.1 percentage points down to 5.9 per cent. The revised projections also baked in higher consumer inflation, a widened current account deficit of 2 per cent of GDP, a weaker rupee, and the likelihood of the central bank raising interest rates by 50 basis points in 2026.

Goldman Sachs also lowered its earnings growth forecast for India by a cumulative 9 percentage points over the next two years. It projected earnings growth of just 8 per cent for calendar year 2026 and 13 per cent for 2027, a drop from the pre-conflict estimates of 16 per cent and 14 per cent.

“Forthcoming earnings cuts, on top of the ongoing investor concerns over the potential adverse impact of AI, will likely impede foreign re-buying after persistent net selling (record $42bn since Sep’24 peak),” Goldman Sachs noted.

Goldman Sachs maintained an ‘overweight’ position on banks, consumer staples, telecommunications, and defence sectors. It upgraded upstream energy companies to ‘overweight’ on the back of tight refining capacity, while simultaneously downgrading downstream oil marketing companies to ‘underweight’ “due to limited pass through of higher crude prices at the gas stations.”

From 175-tonne thrust to future Moon missions: Why ISRO's latest engine test is a game changer

From 175-tonne thrust to future Moon missions: Why ISRO's latest engine test is a game changer  100% tariffs: Trump warns Europe over looming digital services taxes, EU vows swift response

100% tariffs: Trump warns Europe over looming digital services taxes, EU vows swift response June 30 to July 31: ITR scrutiny notice deadline ends June 30; key tax dates to track in July

June 30 to July 31: ITR scrutiny notice deadline ends June 30; key tax dates to track in July Ceasefire at risk? US airstrikes hit Iran after drone attack on cargo ship, Iran retaliates

Ceasefire at risk? US airstrikes hit Iran after drone attack on cargo ship, Iran retaliates  SGB redemption calendar: SGB investors can redeem these Sovereign Gold Bond tranches between July and September

SGB redemption calendar: SGB investors can redeem these Sovereign Gold Bond tranches between July and September Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain

Should You Get Your Heart Check Before Gym? Sneha Mordani & Dr Devi Shetty Explain Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update

Biggest Water Dispute In Asia | India-Pakistan Indus Crisis Update Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock Watch

Casio G-Shock GA-2100CC-3A Review | Coca-Cola x G-Shock Watch The Man Behind Chandigarh's Cleanliness Mission: Meet Padma Shri Awardee Inderjit Singh Sidhu

The Man Behind Chandigarh's Cleanliness Mission: Meet Padma Shri Awardee Inderjit Singh Sidhu TECH TODAY | Apple Products Suddenly Cost More: What's Behind The ₹1 Lakh Price Jump? FAQ

TECH TODAY | Apple Products Suddenly Cost More: What's Behind The ₹1 Lakh Price Jump? FAQ Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure

Coforge, Mphasis, Persistent, LTIMindtree: Share price targets as IT stocks under pressure  JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential

JSW Energy, Ethos, UPL, Ashok Leyland: Top brokerage picks with upto 48% upside potential Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet

Why Rakesh Jhunjhunwala backed Titan when few did; Raamdeo Agrawal explains the winning bet HDFC Bank, ICICI Bank shares top picks; Axis Bank needs better showing to justify premium, says Kotak

HDFC Bank, ICICI Bank shares top picks; Axis Bank needs better showing to justify premium, says Kotak Rs 33 per share dividend announced; check record date, other details

Rs 33 per share dividend announced; check record date, other details