A noticeable mismatch between ITR disclosures and bank statements can trigger additional verification, slow down approvals or, in some cases, result in rejection.

A noticeable mismatch between ITR disclosures and bank statements can trigger additional verification, slow down approvals or, in some cases, result in rejection.A personal loan application can look perfectly in order at first glance. Regular salary credits, healthy account balances and timely Income Tax Return (ITR) filings may suggest a smooth approval process ahead. Yet for many borrowers, problems emerge when lenders notice that the income shown in tax records does not align with actual bank transactions.

Such differences may not always indicate wrongdoing, but they can raise questions during the verification process. Today, banks and digital lending platforms increasingly rely on cross-checking multiple financial records rather than evaluating a single document in isolation. When declared income and banking activity tell different stories, lenders may seek further clarification before moving ahead.

The approach reflects how credit assessment is changing. Instead of relying solely on annual income declarations, lenders are now examining broader financial behaviour to understand earning patterns and assess repayment potential.

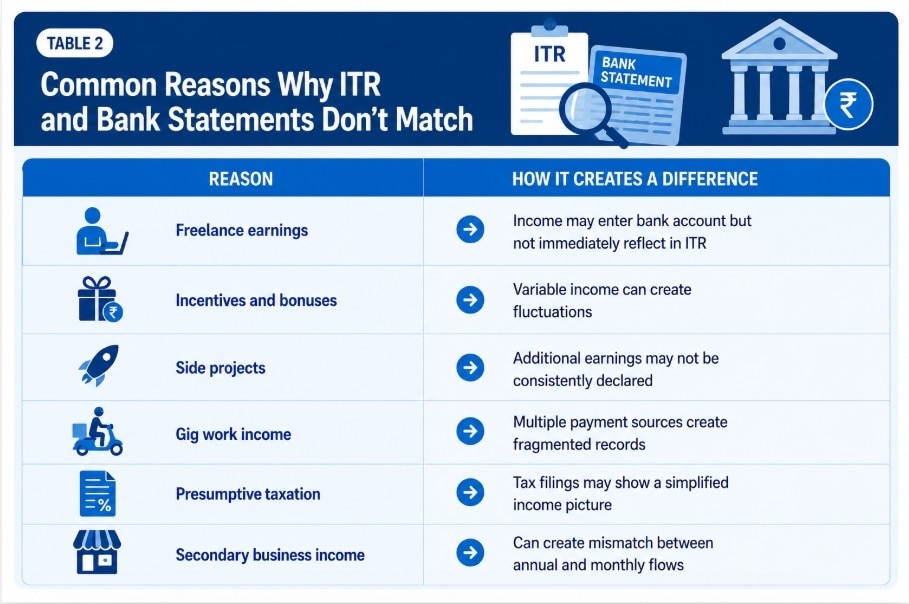

For salaried borrowers, income records often follow predictable patterns. However, freelancers, consultants, self-employed professionals, gig workers and people with multiple sources of income frequently have more varied cash flows.

Income from incentives, side projects, freelance assignments or additional work streams may enter bank accounts regularly but may not immediately appear in tax filings, resulting in gaps between reported income and actual inflows.

MUST READ: 30% Indians face loan rejection without knowing why. Can AI solve this credit awareness gap?

Single-document verification

According to Soumyajit Ghosh, COO, Truebalance, income assessment today has become far more comprehensive than simply reviewing one financial record.

“Evaluating income consistency has evolved toward a much more holistic process rather than relying on a single financial document in isolation. If there is a significant mismatch between ITR filings and bank statement cash flows, it can raise concerns around income stability, repayment capacity, or disclosure accuracy during the underwriting process,” Ghosh said.

He noted that irregular cash flows are not unusual, particularly among self-employed individuals and emerging credit customers.

“In many cases, especially among self-employed or emerging credit customers, irregular cash flows are not uncommon, but transparency becomes extremely important,” he added.

According to Ghosh, lenders increasingly rely on broader data points, including repayment behaviour, bureau information and AI-led cash-flow analysis to understand borrower risk.

MUST READ: Do Indians understand credit scores? Report highlights costly knowledge gaps

“Ultimately, borrowers who maintain clear financial records and consistent disclosures are more likely to see better credit outcomes over time,” he said.

Fragmented income

Industry executives suggest that income mismatches are becoming increasingly frequent due to changing work patterns and the rise of non-traditional income sources.

Shakti Shekhawat, Business Head at BharatLoan, said income fragmentation rather than misreporting often explains the differences.

“Nearly 3 in 10 loan applications today show some level of mismatch between ITR filings and bank statement inflows, and in most cases, it’s not fraud, it's fragmentation of income,” Shekhawat said.

He explained that freelance income, incentives and secondary earnings may not always immediately appear in formal tax records.

“What we’ve seen is that cash flow consistency over 6-12 months is emerging as a far stronger predictor of repayment behaviour than declared annual income alone,” he added.

As a result, underwriting is increasingly shifting toward bank-led assessments and bureau-backed insights rather than relying entirely on static income declarations.

MUST READ: Buying a house with your spouse? Here’s how it can reduce your tax bill

Why documentation still matters

According to Kuldeep Yudhuvanshi, Business Head at Rupee112, larger gaps between stated income and actual bank credits often trigger additional verification.

“In our experience, applications with a significant gap typically 20-30% or more between stated income and bank credits see a materially higher drop-off during underwriting or require additional verification layers,” he said.

He added that despite more adaptive underwriting models, applicants with aligned financial records still receive faster approvals.

“Applicants with aligned financial documentation still see up to 40% faster approvals, underlining the importance of consistency,” Yudhuvanshi said.

As lenders increasingly adopt data-driven underwriting models, borrowers may find that maintaining consistent financial records matters as much as income itself.

MUST READ: Should you take a home loan in a high-interest economy?

India's largest airline IndiGo says Adani airline will be a huge conflict of interest

India's largest airline IndiGo says Adani airline will be a huge conflict of interest 'Giant leap in air defence': India successfully tests Kusha long-range missile for first time

'Giant leap in air defence': India successfully tests Kusha long-range missile for first time Who is Ashiss Kumar Dash, the new CEO-designate at IT major Infosys?

Who is Ashiss Kumar Dash, the new CEO-designate at IT major Infosys? From Haldiram’s to Lakshmi Mittal: Who made millions from Skyroot, India’s first private space unicorn

From Haldiram’s to Lakshmi Mittal: Who made millions from Skyroot, India’s first private space unicorn Switching from iPhone to Android? Google’s Android 17 just made it much easier; Here’s how

Switching from iPhone to Android? Google’s Android 17 just made it much easier; Here’s how Samsung India's Akshay Gupta Reveals Idea Behind New Foldable Form Factor

Samsung India's Akshay Gupta Reveals Idea Behind New Foldable Form Factor Why HFCL Raised Its FY27 Growth Target To 40% | Mahendra Nahata Exclusive

Why HFCL Raised Its FY27 Growth Target To 40% | Mahendra Nahata Exclusive Gold Vs Silver: Which Metal Should You Buy Now? Kunal Shah Decodes The Biggest Opportunities

Gold Vs Silver: Which Metal Should You Buy Now? Kunal Shah Decodes The Biggest Opportunities Nifty, Bank Nifty & Top Trading Picks | Market Masters With Prashant Shah

Nifty, Bank Nifty & Top Trading Picks | Market Masters With Prashant Shah Top 5 Safe Investment Options For You | Personal Finance

Top 5 Safe Investment Options For You | Personal Finance Sensex, Nifty extend losing streak to 4th day as Brent crude nears $100; more downside ahead?

Sensex, Nifty extend losing streak to 4th day as Brent crude nears $100; more downside ahead? Infosys Q1 earnings: IT major cuts FY27 revenue forecast amid muted demand expectations

Infosys Q1 earnings: IT major cuts FY27 revenue forecast amid muted demand expectations  Infosys Q1 FY27 profit rises 12%; board names Ashiss Kumar Dash as Salil Parekh's successor

Infosys Q1 FY27 profit rises 12%; board names Ashiss Kumar Dash as Salil Parekh's successor Twenty Microns shares in sideways trend, analyst suggests Rs 185 stop loss

Twenty Microns shares in sideways trend, analyst suggests Rs 185 stop loss Stovekraft shares trading in a range, ICICI Securities' analyst shares strategy

Stovekraft shares trading in a range, ICICI Securities' analyst shares strategy  Brent hits $100 as tanker attacks, Hormuz risks put crude traders on edge amid US-Iran tensions

Brent hits $100 as tanker attacks, Hormuz risks put crude traders on edge amid US-Iran tensions motorcycles a month in Delhi.") Bajaj Auto to launch Pulsar electric motorcycle in FY28

Bajaj Auto to launch Pulsar electric motorcycle in FY28 'Goal of a SIP isn't to beat the market...': Radhika Gupta on building long-term wealth through market ups and downs

'Goal of a SIP isn't to beat the market...': Radhika Gupta on building long-term wealth through market ups and downs NEET protest: Connaught Place forced to shut by evening, internet snapped at Jantar Mantar

NEET protest: Connaught Place forced to shut by evening, internet snapped at Jantar Mantar Govt permits FDI in inventory based ecommerce model for exports

Govt permits FDI in inventory based ecommerce model for exports